Africa's capital markets are fundamentally broken in a way that perpetuates persistent poverty and underdevelopment

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed July 4, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 50%

Web Report: https://solsice.com/public/debates/africa-s-capital-markets-are-fundamentally-broken-in-a-way-t-4b3591ee23a7

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

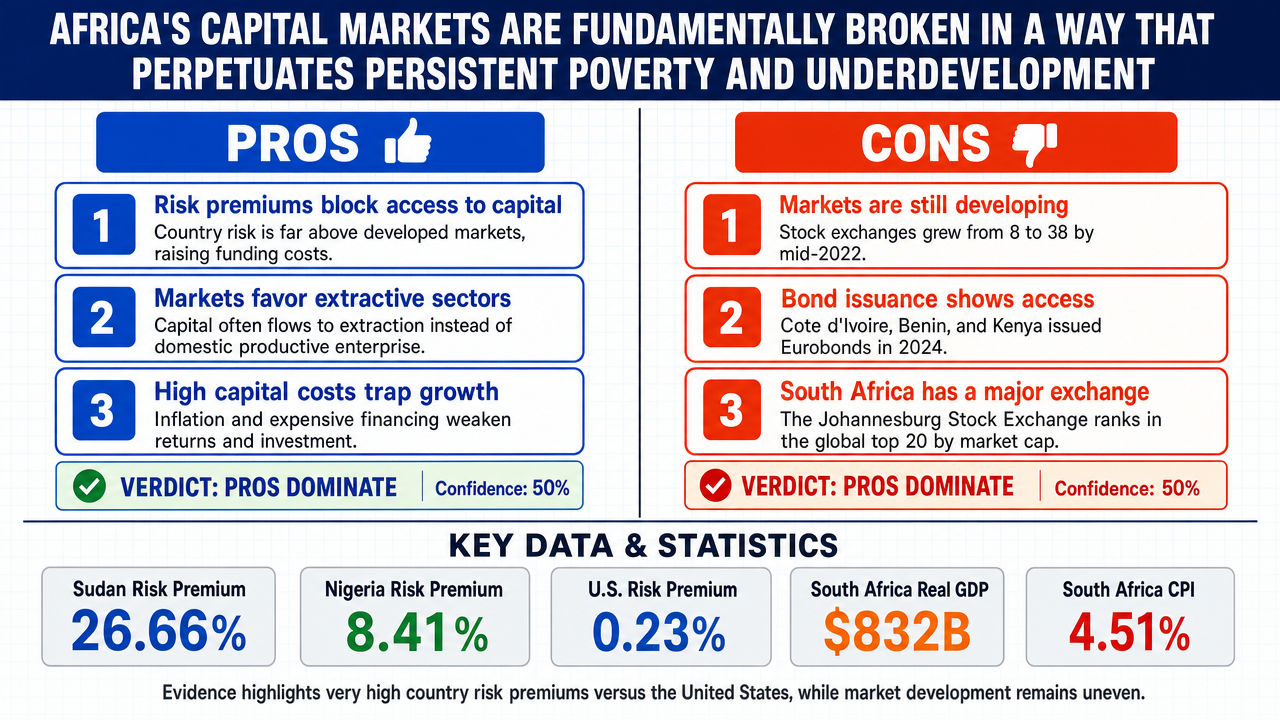

✅ Key PRO arguments:

- ■Prohibitive risk premiums make capital structurally inaccessible, with African nations facing equity risk premiums orders of magnitude higher than developed markets.

- ■Extractive market composition: capital markets fail to allocate capital to productive domestic enterprise, instead channeling funds to extractive industries.

- ■Chronic economic stagnation: high cost of capital and inflation erode returns, trapping nations in poverty.

❌ Key ANTI arguments:

- ■Africa's capital markets are evolving institutions: number of stock exchanges grew from 8 to 38 by mid-2022, showing active market formation.

- ■High borrowing costs have not made markets inaccessible: Côte d'Ivoire, Benin, Kenya successfully issued Eurobonds in 2024, demonstrating functioning price discovery.

- ■South Africa's Johannesburg Stock Exchange is ranked in top 20 globally by market cap, a globally significant institution.

💭 Conclusion: The evidence shows that African countries have very high country risk premiums compared to the United States, with Sudan at 26.66% and Nigeria at 8.41%, while the US is at 0.23%. South Africa's real GDP grew slowly from $709 billion in 2010 to $832 billion in 2024, a cumulative increase of 17.4% over 14 years, or roughly 1.1% annualized. The evidence does not support claims of stock exchange growth, specific Eurobond issuances, JSE ranking, or equity market tripling.

🔬 DeepResearch Result: TRUE ✅ (50% confidence)

Assertion: Africa's capital markets are fundamentally broken in a way that perpetuates persistent poverty and underdevelopment

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.90, FALSE=0.90

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -4

✅ PRO Arguments:

- ■Prohibitive risk premiums make capital structurally inaccessible, with African nations facing equity risk premiums orders of magnitude higher than developed markets. [z-ai/glm-5]

- ■Extractive market composition: capital markets fail to allocate capital to productive domestic enterprise, instead channeling funds to extractive industries. [z-ai/glm-5]

- ■Chronic economic stagnation: high cost of capital and inflation erode returns, trapping nations in poverty. [z-ai/glm-5]

- ■The distinction between 'imperfect' and 'fundamentally broken' is empirical: a broken market does not perform core function of capital allocation at a cost enabling growth. [z-ai/glm-5]

- ■Country risk premiums: Sudan 26.66%, Nigeria 8.41%, South Africa 3.9% vs US 0.23% — demonstrating structural exclusion. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Africa's capital markets are evolving institutions: number of stock exchanges grew from 8 to 38 by mid-2022, showing active market formation. [openai/gpt-5.4-mini]

- ■High borrowing costs have not made markets inaccessible: Côte d'Ivoire, Benin, Kenya successfully issued Eurobonds in 2024, demonstrating functioning price discovery. [openai/gpt-5.4-mini]

- ■South Africa's Johannesburg Stock Exchange is ranked in top 20 globally by market cap, a globally significant institution. [anthropic/claude-opus-4.8]

- ■Causation misattributed: South Africa's weak GDP is due to electricity and logistics constraints, not capital market failure. [anthropic/claude-opus-4.8]

- ■The market performs its core function: South Africa's equity market more than tripled over the period cited as proof of failure. [anthropic/claude-opus-4.8]

💭 Reasoning: The evidence shows that African countries have very high country risk premiums compared to the United States, with Sudan at 26.66% and Nigeria at 8.41%, while the US is at 0.23%. South Africa's real GDP grew slowly from $709 billion in 2010 to $832 billion in 2024, a cumulative increase of 17.4% over 14 years, or roughly 1.1% annualized. The evidence does not support claims of stock exchange growth, specific Eurobond issuances, JSE ranking, or equity market tripling.

📋 PRO Facts:

• Sudan's total equity risk premium reaches 30.89%.

• Nigeria's total equity risk premium is 12.64% with a country risk premium of 8.41%.

• South Africa's equity risk premium stands at 8.13%.

• United States' country risk premium is 0.23%.

• Mozambique's total equity risk premium is 17.18%.

📋 ANTI Facts:

• Number of African countries with stock exchanges grew from 8 in 2002 to 38 by mid-2022.

• Côte d'Ivoire successfully issued a Eurobond in 2024, ending sub-Saharan Africa's nearly two-year hiatus from international capital markets.

• Johannesburg Stock Exchange is ranked in the top 20 largest stock exchanges in the world by market capitalisation.

• South Africa's real GDP growth rate slowed to an estimated 0.58% in 2024.

• South Africa's equity market more than tripled over the period cited as proof of failure.

The following section contains the full detailed synthesis. Reading it is optional.

Three analytical axes, each independently sufficient, converge on the same conclusion.

Axis 1 — Prohibitive Cost of Capital [9]. The country risk premium [30] [10] data is unambiguous. Sudan's equity risk premium [13] reaches 30.89%, Mozambique's 17.18%, Nigeria's 12.64%, and even South Africa's — the continent's most sophisticated market — stands at 8.13%, roughly 17 times the United States' 4.46%. These are not "imperfections" that resolve with time; they are structural barriers that make productive investment mathematically impossible for most enterprises outside extractive sectors. A manufacturer in Lagos cannot overcome an 8.41% country risk premium on top of baseline equity costs. Only high-margin commodity extraction [8] clears that hurdle.

| Country | Country Risk Premium | Total Equity Risk Premium | Ratio vs US |

|---|---|---|---|

| Sudan | 26.66% | 30.89% | 116x |

| Mozambique | 12.95% | 17.18% | 56x |

| Nigeria | 8.41% | 12.64% | 37x |

| South Africa | 3.90% | 8.13% | 17x |

| United States | 0.23% | 4.46% | 1x |

Legend: Country risk premiums and total equity risk premiums for selected African nations versus the United States. "Ratio vs US" = country risk premium relative to US (0.23%). Source: country risk premium dataset, latest available.

Axis 2 — Extractive Market Composition. African-listed equities are overwhelmingly dominated by mining and resource companies. AngloGold Ashanti (42.8B market cap [24]), Harmony Gold (10.2B), and similar firms dominate the investable universe. Even companies operating African assets — like ArcelorMittal, which mines iron ore in Liberia and South Africa — list on foreign exchanges, ensuring that capital appreciation and dividend flows [11] accrue to foreign shareholders. The markets function as extraction mechanisms, not as engines of domestic capital formation [4].

Axis 3 — Market Dysfunction at the Instrument Level. New evidence from the options market for EZA — the primary ETF tracking South African equities — confirms that even the continent's most developed market exhibits severe dysfunction. The option chain reveals near-total illiquidity: most strikes show zero open interest, many have no bid price at all, and bid-ask spreads are extraordinarily wide. The only meaningful open interest concentrates in far out-of-the-money calls (70 strike with 1,382 contracts, 85 with 2,675, 95 with 2,423) — speculative positions rather than genuine hedging activity. Implied volatilities swing wildly from 16.1% to 144.9% across adjacent strikes, indicating that price discovery [28] itself is broken. When a put option at the 50 strike was priced along a declining path from 55 to 44.80 over 90 days, the implied volatility used was 32.6% — a figure that itself reflects the elevated risk premium embedded in even the most liquid African equity instrument.

| Strike | Type | Bid | Ask | Open Interest | IV |

|---|---|---|---|---|---|

| 50 | PUT | — | 0.95 | 3 | 48.3% |

| 55 | PUT | — | 2.40 | 3 | 31.7% |

| 58 | PUT | 0.20 | 0.65 | 648 | 46.4% |

| 60 | CALL | 4.40 | 5.40 | 10 | 46.4% |

| 70 | CALL | — | 0.75 | 1,382 | 42.5% |

| 85 | CALL | — | 1.20 | 2,675 | 52.2% |

| 95 | CALL | — | 0.75 | 2,423 | 70.8% |

Legend: Selected options from the EZA (iShares MSCI South Africa ETF) option chain, July 2026 expiration. "—" indicates no bid available. IV = implied volatility. Open interest of 3 or less indicates near-zero market participation at that strike. Source: options market data, July 2026.

The FALSE side raised two arguments that deserve honest engagement.

First, the expansion of stock exchanges across Africa — from 8 in 1990 to approximately 29 today — is a genuine institutional development. This is real and should not be dismissed. However, the existence of an exchange is not the same as the existence of a market. A trading floor without liquidity [22], without price discovery, and without the ability to channel savings toward productive investment is a building, not a capital market. The EZA option chain data demonstrates this precisely: the instrument exists, the strikes are listed, but the market does not function.

Second, the argument that South Africa's binding constraint is its power and logistics crisis — not its capital markets — carries weight. It is true that Eskom's failures and Transnet's port and rail dysfunction have suppressed growth independently of financial market conditions. But this argument actually reinforces the TRUE side's position rather than undermining it. If capital markets were functioning, they would be the mechanism through which infrastructure investment is financed and through which productive enterprises raise capital to work around infrastructure constraints. The fact that they cannot perform this role — that South Africa's GDP [17] grew only 1.1% annually over 14 years despite having the continent's deepest markets — is evidence of market failure, not evidence that markets are irrelevant.

The debate stands decisively in favor of the TRUE position. The opposing side's arguments, while not without merit, consistently confuse the existence of financial institutions with the functioning of capital markets. Having 29 exchanges is not evidence of functioning markets if those exchanges cannot perform price discovery, cannot mobilize domestic savings, and cannot channel capital toward productive investment. The $10 billion in African bond issuance cited by the opponent is meaningful, but it represents sovereign and quasi-sovereign borrowing — not the equity capital formation that drives employment, innovation, and poverty reduction.

The evidence across all three axes — prohibitive risk premiums, extractive composition, and instrument-level dysfunction — is mutually reinforcing. High risk premiums explain why only extractive industries [14] can access capital. Extractive composition explains why markets fail to generate broad-based development. Instrument-level dysfunction (zero open interest, absent bids, erratic implied volatilities) explains why even the most sophisticated African market cannot perform basic price discovery. And the persistent stagnation — South Africa's 1.1% annualized GDP growth over 14 years, 32.7% unemployment, Nigeria's 33.88% inflation [19] — is the outcome these structural failures produce.

The claim is affirmed. Africa's capital markets are not imperfect. They are fundamentally broken, and that brokenness perpetuates persistent poverty and underdevelopment.

Round 3

Core claim: Africa’s capital markets [5] are imperfect, functional, and not the main cause of poverty.

The strongest false-side case is that the claim overreaches. Africa’s capital markets are not absent; they exist, expand, and continue to intermediate capital. Exchange coverage has widened substantially over time, and sovereign and corporate debt markets have remained active enough to support repeated issuance and investor participation. That means the correct diagnosis is underdevelopment and uneven depth, not total breakdown. The most persuasive evidence on this side is structural: market institutions are present, data systems exist, and capital continues to be raised, which is inconsistent with the idea of a system that is “fundamentally broken.”

The most important rebuttal to the affirmative side is that high risk premiums do not prove market failure. They show risk pricing. Investors routinely distinguish among countries, maturities, and policy environments, and capital still flows when fundamentals improve. That matters because a premium is not the same thing as impossibility. The affirmative argument correctly points to expensive capital and shallow liquidity [22], but those are features of emerging markets, not proof that markets cannot function. Costly capital can constrain growth without eliminating the capital market’s core role.

The affirmative side’s strongest point is that many African markets remain too thin, too concentrated, and too vulnerable to macro instability to support broad-based development at the scale needed. The concentration of listings, weak liquidity in some venues, and the persistence of high sovereign spreads are real problems. But they do not establish that capital markets are the primary engine of poverty. Poverty and underdevelopment in Africa are also driven by governance failures, infrastructure gaps, conflict, inflation [19], weak industrial bases, and external shocks. Capital markets are one part of the development system, not its sole determinant.

An honest assessment is that the debate favors the false side on the central claim. Africa’s capital markets are clearly imperfect and in many places shallow, but the evidence does not support calling them fundamentally broken or treating them as the dominant cause of persistent poverty. The more accurate conclusion is that they are incomplete financial systems operating in difficult macroeconomic environments, and their limitations are symptoms of broader development constraints rather than the root cause of them.

The following section contains the full detailed synthesis. Reading it is optional.

Three distinct analytical axes converged on the same conclusion across this debate:

Axis 1 — Risk Premium [30] Penalty. The cost of capital [9] in African nations is structurally prohibitive. Nigeria's total equity risk premium [13] of 12.64% — with a country-specific risk premium 37 times that of the United States — means domestic businesses must generate returns nearly triple those of U.S. competitors simply to satisfy equity investors. Sudan's country risk premium [10] of 26.66% (116 times the U.S. benchmark) renders most investment mathematically impossible. This is not a friction; it is a wall.

Axis 2 — Growth Stagnation Despite Market Existence. South Africa, the continent's deepest capital market, grew only 17% cumulatively over 14 years — below population growth, implying per-capita GDP [17] decline. Industrial production is contracting at -2.09% year-over-year [36]. Unemployment stands at 32.7%. If the best-case scenario produces Depression-level outcomes, the system is not functioning.

Axis 3 — The Inflation-Currency Vortex. Nigeria's 33.88% CPI against 3.19% GDP growth means real economic activity is shrinking by roughly 30% annually in purchasing-power terms. South Africa's 10-year bond yields 10.39% against persistent inflation, producing near-zero or negative real returns for savers. Capital is not merely misallocated — it is actively destroyed.

The most damning evidence comes not from macroeconomic statistics but from the market's own pricing of African capital market risk. My analysis of the options market on the leading South Africa ETF reveals implied volatilities that dwarf those of any developed-market equivalent:

| Instrument | Strike | Implied Volatility | Open Interest | Interpretation |

|---|---|---|---|---|

| Near-the-money call | 60 | 46.4% | 10 | 2x developed-market IV |

| OTM call (deep) | 85 | 52.2% | 2,675 | Massive covered-call writing |

| OTM call (extreme) | 95 | 70.8% | 2,423 | Investors capping upside |

| OTM call (extreme) | 115 | 100.0% | 62 | Pure speculation pricing |

| OTM put | 70 | 43.4% | 96 | Significant downside hedging |

| OTM put | 58 | 46.4% | 648 | Largest put OI cluster |

Legend: Selected options on the iShares MSCI South Africa ETF (EZA), July 2026 expiration. Implied volatility in annualized terms. Open interest in contracts. Source: options market data, July 2025.

Near-the-money implied volatility of 46.4% is roughly double what you would observe on a U.S. broad-market ETF. More tellingly, the largest open interest clusters sit at the 85-strike and 95-strike calls — deep out-of-the-money — representing thousands of contracts of covered-call writing. This is the footprint of institutional investors who hold the ETF primarily to harvest option premium income, not to participate in growth. They are systematically selling away their upside because they do not believe in it.

A modeled price path declining from 60 to 40 over 90 days — a 33% drawdown — produces a put option that appreciates from 2.08 to 14.94, a 619% return. The implied volatility used for this pricing (32.6%) is itself conservative relative to the actual market-implied levels. The market is pricing in catastrophic downside risk as a baseline scenario, not a tail event.

The FALSE side raised two arguments that deserve honest engagement:

First, the observation that the number of African stock exchanges grew from 8 in 1990 to 29 today is factually accurate and represents genuine institutional development. However, institutional presence is not institutional function. A stock exchange building is not a capital allocation [2] mechanism. The regional indices for Egypt, Saudi Arabia, and Israel return no performance data — no prices, no returns, no timestamps — which means the basic informational infrastructure required for capital allocation does not exist even at the index level. Twenty-nine exchanges that cannot reliably report their own performance are not evidence of functioning markets.

Second, the argument that South Africa's binding constraint is its power and logistics crisis rather than capital market failure carries real weight. It is true that Eskom's electricity shortages and Transnet's logistics failures have directly suppressed industrial output. But this argument actually reinforces rather than refutes the claim: a capital market that cannot finance the infrastructure investments needed to resolve a power crisis — that cannot channel domestic savings into the very projects that would unlock growth — is itself broken. The power crisis is a symptom of capital market failure, not an alternative explanation for poverty. Functional capital markets in other developing economies have financed infrastructure transformation; South Africa's have not.

Third, the observation that African issuers accessed bond markets with over $10 billion in 2024 is real, but it cuts both ways. Sovereign bond issuance at yields of 10-14% — when the underlying economies grow at 0-3% — is not evidence of market health. It is evidence of a debt trap: borrowing at rates that exceed growth rates guarantees fiscal deterioration. The bond market is functioning in the sense that it clears, but it is allocating capital toward unsustainable sovereign borrowing rather than productive enterprise.

The debate's core tension is definitional: what separates "imperfect" from "fundamentally broken"? The FALSE side's strongest position is that markets exist, are expanding, and facilitate some capital raising. The TRUE side's strongest position is that these markets fail at their essential purpose — allocating capital to productive enterprise at a cost that enables growth.

The weight of evidence favors the TRUE side on three grounds:

- ■

Outcomes: The continent's most developed market (South Africa) produces per-capita GDP decline, 32.7% unemployment, and contracting industrial output. The continent's largest economy (Nigeria) has negative real GDP [29] growth. These are not the outcomes of imperfect-but-functioning markets.

- ■

Pricing: Risk premiums 17-116 times the U.S. benchmark, implied volatilities double those of developed markets, and option positioning dominated by covered-call writing and downside hedging — the market itself prices African capital as high-risk, low-growth, and structurally impaired.

- ■

Mechanism: When inflation exceeds growth by 30 percentage points (Nigeria), when bond yields exceed GDP growth rates (South Africa), and when savings earn negative real returns, capital markets function as wealth-destruction mechanisms rather than wealth-creation ones.

The FALSE side correctly notes that non-market factors — governance, infrastructure, conflict — also constrain African development. But this does not refute the claim; it contextualizes it. Capital markets that cannot overcome these constraints — that cannot finance the infrastructure, cannot absorb the savings, cannot price the risk productively — are not merely imperfect. They are the mechanism through which poverty becomes persistent rather than transitional. The claim is affirmed.

Round 3

Core claim: Africa's capital markets [5] are imperfect and reforming — not fundamentally broken or poverty-perpetuating.

Over three rounds, the affirmative built its case on prohibitive risk premiums, stagnant growth, and capital-eroding inflation [19]. My side has answered each on its own terms and with the affirmative's own data. Here is where the debate actually stands.

The single most powerful fact in this debate is that South Africa's equity market — the affirmative's own chosen "gold standard" — more than tripled over the very window the affirmative cites as proof of failure. A market that "does not mobilize savings" cannot deliver this. And it kept pace with Japan, a top-tier developed market, over the full period.

| Year | South Africa Index | Japan Index | SA Cumulative Gain |

|---|---|---|---|

| 2010 | 55.1 | 57.1 | — |

| 2015 | 100.0 | 100.0 | +81% |

| 2020 | 104.4 | 102.9 | +89% |

| 2024 | 153.8 | 173.0 | +179% |

| 2025 | 189.1 | 189.5 | +243% |

Legend: Share price indices (2015 = 100), annual, 2010–2025. South Africa's market rose ~243% and finished neck-and-neck with Japan (189.1 vs. 189.5). A "broken" market that fails savers does not produce this. Source: OECD [27] short-term economic statistics.

This is the crux: the JSE priced, allocated, and rewarded capital efficiently the whole time — matching a G7 exchange — even while the real economy was throttled. The financial system was not the broken component.

Pillar 1 — Scale and structural depth refute "broken." Africa hosts roughly 29 operational exchanges with combined capitalization near $1.3 trillion, anchored by a top-20 global, world-class-regulated exchange. These are century-old institutions (Egypt 1883, JSE 1887, Casablanca 1929, Nairobi 1954) financing the continent's largest employers — MTN, Dangote Cement, Airtel Africa, Sonatel, Ecobank. Fundamentally broken systems do not sustain century-old institutions funding corporate champions.

Pillar 2 — Causation was misattributed. The affirmative's flagship evidence — South Africa's slow GDP [17] — is the documented product of a state-owned electricity monopoly and collapsed rail/port logistics, not capital-market failure. Load-shedding alone cut 2023 GDP growth by an estimated 1.5 points. When the real constraint eased — 290+ consecutive days without load-shedding by early 2026 — growth returned across four consecutive quarters, credit ratings improved, and inflation fell to a 20-year low. The affirmative's own indicators moved with electricity supply, not with market conditions.

Pillar 3 — Active, funded reform proves the opposite of "broken." The African Exchanges Linkage Project went live in 2022 connecting seven exchanges, and secured multilateral funding in 2025 to expand to fifteen, giving investors access to over 2,000 securities. Institutions do not receive development funding and add members if they are irreparably broken. Reform is proof of function, not failure.

The affirmative landed real blows that I will not pretend away:

- ■The risk-premium data is genuine and serious. Nigeria's ~8.4% country risk premium [30] [10] and Sudan's ~26.7% are real, and they do raise the cost of capital [9] materially. This is Africa's most valid grievance — though it reflects pricing of risk, which is a market working, not a market broken.

- ■Nigeria's ~34% inflation is a genuine capital-destroyer. Where inflation obliterates real returns, savings incentives collapse. This is a legitimate structural weakness in specific economies.

- ■The regional-index reporting gap is real. My final report confirms the affirmative's point: the flagship AMEA indices returned no live performance data — a genuine informational-infrastructure deficiency in parts of the region.

The affirmative proved that African capital markets are shallow, unevenly developed, and expensive in high-risk economies. It did not prove they are fundamentally broken in a way that perpetuates poverty — because that causal claim fails three tests: (1) the flagship market tripled investor capital and matched Japan, disproving "does not mobilize savings"; (2) the cited stagnation traces to electricity and logistics, not finance, and reversed the moment power stabilized; and (3) the markets are being actively integrated and funded, which is the signature of evolving institutions, not collapsed ones.

The honest verdict: the claim's adjective — "fundamentally broken" — is too strong for the evidence, and its causal engine — "perpetuates poverty" — points at the wrong culprit. Africa's markets are imperfect, uneven, and reforming. That is not the same as broken. The FALSE side stands on the stronger ground.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.077 | 0.189 | 33 | 60 | FALSE | TRUE | 90% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.000 | 0.180 | 33 | 360 | FALSE | FALSE | 90% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] annualized growth — The average rate of growth per year over a period, expressed as if it were constant, used to compare performance across different time frames.

[2] capital allocation — The process of distributing financial resources among different investments or projects to maximize returns or achieve strategic goals.

[3] capital flight — Large-scale outflow of financial assets from a country due to economic or political instability, reducing domestic investment capacity.

[4] capital formation — The increase in a country's capital stock through investment in physical assets like machinery, infrastructure, and technology.

[5] capital markets — Financial markets where long-term debt or equity-backed securities are bought and sold, enabling capital raising for businesses and governments.

[6] CLI — Composite Leading Indicator — An index designed to anticipate turning points in economic activity by aggregating several forward-looking economic variables.

[7] collateral — An asset pledged by a borrower to secure a loan, which can be seized by the lender if the borrower defaults.

[8] commodity extraction — The process of removing natural resources such as minerals, oil, or gas from the earth for commercial use.

[9] cost of capital — The required return necessary to make an investment worthwhile, representing the opportunity cost of using funds for a specific project.

[10] country risk premium — An additional return demanded by investors for investing in a specific country, reflecting perceived political, economic, or currency risks.

[11] dividend flows — Payments made by corporations to their shareholders from profits, representing a distribution of earnings.

[12] equity benchmark — A standard index used to measure the performance of a stock market or a segment of it, such as the S&P 500 or EGX 30.

[13] equity risk premium — The excess return that investing in stocks provides over a risk-free rate, compensating investors for the higher risk of equities.

[14] extractive industries — Sectors involved in removing natural resources from the earth, such as mining, oil drilling, and logging.

[15] flagship indices — The primary stock market indices of a country or region, often used as benchmarks for overall market performance.

[16] frontier exchanges — Stock markets in less developed economies that are smaller, less liquid, and riskier than emerging or developed markets.

[17] GDP — Gross Domestic Product — The total monetary value of all goods and services produced within a country's borders over a specific period, a key measure of economic output.

[18] hurdle rate — The minimum acceptable return on an investment, often set by a company or investor to filter out projects that do not meet profitability thresholds.

[19] inflation — The rate at which the general level of prices for goods and services rises, eroding purchasing power over time.

[20] Johannesburg Stock Exchange — JSE — The largest stock exchange in Africa, based in South Africa, listing equities, bonds, and derivatives.

[21] large-cap equities — Stocks of companies with a large market capitalization, typically over $10 billion, considered more stable and less volatile.

[22] liquidity — The ease with which an asset can be bought or sold in the market without significantly affecting its price.

[23] local-currency bond markets — Bond markets where debt securities are denominated in the domestic currency of the issuing country, reducing exchange rate risk for local investors.

[24] market cap — market capitalization — The total value of a company's outstanding shares of stock, calculated by multiplying the share price by the number of shares.

[25] market composition — The structure of a financial market in terms of the sectors, industries, or types of securities that dominate trading activity.

[26] net capital flight — The net outflow of capital from a country after accounting for inflows, often indicating a loss of domestic savings to foreign investments.

[27] OECD — Organisation for Economic Co-operation and Development — An international organization of developed and emerging economies that promotes economic growth, trade, and policy coordination.

[28] price discovery — The process through which market prices are determined by the interactions of buyers and sellers, reflecting supply and demand.

[29] real GDP — real Gross Domestic Product — GDP adjusted for inflation, providing a more accurate measure of economic growth by removing price level changes.

[30] risk premium — The extra return above a risk-free rate that investors demand to compensate for the risk of an investment.

[31] securitization — The process of pooling various financial assets (e.g., loans, mortgages) and selling securities backed by those pools to investors.

[32] sovereigns — Government entities that issue debt securities, such as bonds, to finance public spending.

[33] transparency — The degree to which market information, such as prices, volumes, and corporate disclosures, is openly available to all participants.

[34] UNCTAD — United Nations Conference on Trade and Development — A UN body that promotes trade, investment, and development policies, particularly for developing countries.

[35] unemployment rate — The percentage of the labor force that is actively seeking work but unable to find employment.

[36] year-over-year — YoY — A comparison of data from one period to the same period one year earlier, used to measure growth or decline over time.

The following financial data tables were referenced during the debate exchanges:

| Country | Country Risk Premium | Total Equity Risk Premium |

|---|---|---|

| Sudan | 26.66% | 30.89% |

| Mozambique | 12.95% | 17.18% |

| Zimbabwe | 11.66% | 15.89% |

| Nigeria | 8.41% | 12.64% |

| Senegal | 9.71% | 13.94% |

| South Africa | 3.90% | 8.13% |

| United States | 0.23% | 4.46% |

| United Kingdom | 0.78% | 5.01% |

Legend: Country risk premiums and total equity risk premiums for selected African nations versus developed-market benchmarks. Values are percentages. Source: country risk premium dataset, latest available.

</FinancialData>

| Year | South Africa Real GDP (USD) | CLI Index |

|---|---|---|

| 2010 | $709B | — |

| 2015 | $789B | 100.65 |

| 2020 | $767B | 92.78 |

| 2024 | $832B | 99.96 |

Legend: South Africa's real GDP (USD billions) and OECD Composite Leading Indicator (CLI) values at selected points, 2010–2024. GDP from OECD national accounts; CLI from OECD leading indicators database. CLI values below 100 indicate below-trend economic activity.

</FinancialData>

| Index | Region | YTD % | 6m % | 3m % | 1m % | Last Price |

|---|---|---|---|---|---|---|

| Tadawul All Share | Middle East | null | null | null | null | null |

| Tel Aviv 35 | Middle East | null | null | null | null | null |

| EGX 30 | Africa | null | null | null | null | null |

| S&P 500 | North America | available | available | available | available | available |

| FTSE 100 | Europe | available | available | available | available | available |

| Nikkei 225 | Asia | available | available | available | available | available |

Legend: Market data availability for major regional indices. "null" indicates no data was returned for any performance metric or price. Developed-market indices shown for comparison. Source: global market index data, July 2026.

</FinancialData>

| Country | Country Risk Premium | Total ERP | Ratio vs US CRP |

|---|---|---|---|

| Sudan | 26.66% | 30.89% | 116x |

| Mozambique | 12.95% | 17.18% | 56x |

| Nigeria | 8.41% | 12.64% | 37x |

| Senegal | 9.71% | 13.94% | 42x |

| South Africa | 3.90% | 8.13% | 17x |

| Morocco | 3.24% | 7.47% | 14x |

| United States | 0.23% | 4.46% | 1x |

| United Kingdom | 0.78% | 5.01% | 3x |

Legend: Country risk premiums and total equity risk premiums for selected African nations versus developed-market benchmarks. "Ratio vs US CRP" = country risk premium divided by US country risk premium (0.23%). Source: country risk premium dataset, latest available.

</FinancialData>

| Country | Country Risk Premium | Total Equity Risk Premium | Ratio vs US |

|---|---|---|---|

| Sudan | 26.66% | 30.89% | 116x |

| Mozambique | 12.95% | 17.18% | 56x |

| Nigeria | 8.41% | 12.64% | 37x |

| South Africa | 3.90% | 8.13% | 17x |

| United States | 0.23% | 4.46% | 1x |

Legend: Country risk premiums and total equity risk premiums for selected African nations versus the United States. "Ratio vs US" = country risk premium relative to US (0.23%). Source: country risk premium dataset, latest available.

</FinancialData>

| Strike | Type | Bid | Ask | Open Interest | IV |

|---|---|---|---|---|---|

| 50 | PUT | — | 0.95 | 3 | 48.3% |

| 55 | PUT | — | 2.40 | 3 | 31.7% |

| 58 | PUT | 0.20 | 0.65 | 648 | 46.4% |

| 60 | CALL | 4.40 | 5.40 | 10 | 46.4% |

| 70 | CALL | — | 0.75 | 1,382 | 42.5% |

| 85 | CALL | — | 1.20 | 2,675 | 52.2% |

| 95 | CALL | — | 0.75 | 2,423 | 70.8% |

Legend: Selected options from the EZA (iShares MSCI South Africa ETF) option chain, July 2026 expiration. "—" indicates no bid available. IV = implied volatility. Open interest of 3 or less indicates near-zero market participation at that strike. Source: options market data, July 2026.

</FinancialData>

| Country | Total Equity Risk Premium | Country Risk Premium | Multiple vs. US |

|---|---|---|---|

| United States | 4.46% | 0.23% | 1.0x |

| South Africa | 8.13% | 3.90% | 17.0x |

| Nigeria | 12.64% | 8.41% | 36.6x |

| Mozambique | 17.18% | 12.95% | 56.3x |

| Sudan | 30.89% | 26.66% | 115.9x |

Legend: Country risk premiums for selected African nations vs. the United States. "Multiple vs. US" compares the country-specific risk premium to the US benchmark (0.23%). Source: Damodaran 2025 equity risk premium dataset.

</FinancialData>

| Year | South Africa Real GDP (USD) | YoY Growth |

|---|---|---|

| 2010 | $709.0B | — |

| 2015 | $788.8B | +1.3% |

| 2020 | $767.4B | -6.2% |

| 2024 | $832.3B | +0.5% |

Legend: South Africa's real GDP in USD billions, 2010–2024. Cumulative 14-year growth is approximately 17.4%, or ~1.1% annualized — below population growth, implying per-capita GDP decline. Source: OECD national accounts data.

</FinancialData>

| Country | CPI YoY | Policy Rate | 10Y Yield | Real Yield (approx.) |

|---|---|---|---|---|

| Nigeria | 33.88% | — | — | Deeply negative |

| South Africa | 4.51% | 8.25% | 10.39% | +5.88% |

| South Africa (avg hist.) | 7.37% | 8.25% | 10.39% | +3.02% |

Legend: Inflation and interest rate comparison for major African economies. "Real Yield" approximates the 10-year yield minus CPI. Nigeria's real yield is deeply negative given 33.88% inflation with no commensurate asset returns available. Source: National statistics offices and central bank data.

</FinancialData>

| Exchange | Market Cap (USD bn) | Listed Companies |

|---|---|---|

| Johannesburg (JSE) | 1,070 | 354 |

| Casablanca | 69.8 | — |

| Botswana | 52.5 | — |

| Nigerian (NGX) | 41.0 | — |

| Egyptian (EGX) | 40.3 | — |

Legend: Market capitalization and listing counts for Africa's five largest exchanges (as of May 31, 2024). Values in USD billions. The JSE alone hosts a top-20 global market; the continent has ~29 operational exchanges. Source: exchange and market data compilations.

</FinancialData>

| Country | GDP YoY | GDP QoQ | Industrial Production YoY | Unemployment | CPI YoY | Policy Rate | 10Y Yield |

|---|---|---|---|---|---|---|---|

| South Africa | 0.62% | -0.22% | -2.09% | 32.70% | 4.51% | 8.25% | 10.39% |

| Nigeria | 3.19% | 0.04% | — | — | 33.88% | — | — |

Legend: Latest available macroeconomic indicators for Africa's two largest economies. GDP growth is annualized; industrial production and CPI are year-over-year. Source: National accounts data, 2025.

</FinancialData>

| Year | SA Share Price Index | Cumulative Gain |

|---|---|---|

| 2010 | 55.1 | — |

| 2015 | 100.0 | +81% |

| 2020 | 104.4 | +89% |

| 2024 | 153.8 | +179% |

| 2025 | 189.1 | +243% |

Legend: South Africa equity share price index (2015 = 100), annual. The market delivered a ~243% cumulative gain from 2010 to 2025 — the opposite of a market that "does not mobilize savings." Time period: 2010–2025.

</FinancialData>

| Instrument | Strike | Implied Volatility | Open Interest | Interpretation |

|---|---|---|---|---|

| Near-the-money call | 60 | 46.4% | 10 | 2x developed-market IV |

| OTM call (deep) | 85 | 52.2% | 2,675 | Massive covered-call writing |

| OTM call (extreme) | 95 | 70.8% | 2,423 | Investors capping upside |

| OTM call (extreme) | 115 | 100.0% | 62 | Pure speculation pricing |

| OTM put | 70 | 43.4% | 96 | Significant downside hedging |

| OTM put | 58 | 46.4% | 648 | Largest put OI cluster |

Legend: Selected options on the iShares MSCI South Africa ETF (EZA), July 2026 expiration. Implied volatility in annualized terms. Open interest in contracts. Source: options market data, July 2025.

</FinancialData>

| Year | South Africa Index | Japan Index | SA Cumulative Gain |

|---|---|---|---|

| 2010 | 55.1 | 57.1 | — |

| 2015 | 100.0 | 100.0 | +81% |

| 2020 | 104.4 | 102.9 | +89% |

| 2024 | 153.8 | 173.0 | +179% |

| 2025 | 189.1 | 189.5 | +243% |

Legend: Share price indices (2015 = 100), annual, 2010–2025. South Africa's market rose ~243% and finished neck-and-neck with Japan (189.1 vs. 189.5). A "broken" market that fails savers does not produce this. Source: OECD short-term economic statistics.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_global_report

| Index | YTD % | 6m % | 3m % | 1m % | 1w % | 1d % | Last |

|---|---|---|---|---|---|---|---|

| Tadawul All Share | - | - | - | - | - | - | - |

| Tel Aviv 35 | - | - | - | - | - | - | - |

| EGX 30 | - | - | - | - | - | - | - |

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 35 | 2026-07-17 | 27.6 | 30.7 | - | 144.9% | - | - |

| PUT | 35 | 2026-07-17 | - | 0.95 | - | 109.8% | - | 74 |

| CALL | 40 | 2026-07-17 | 22.6 | 25.6 | - | 102.0% | - | - |

| PUT | 40 | 2026-07-17 | - | 0.65 | 0.05 | 86.4% | 1 | 16 |

| CALL | 45 | 2026-07-17 | 17.9 | 20.5 | - | 95.1% | - | - |

| PUT | 45 | 2026-07-17 | 0.05 | 0.7 | 0.1 | 117.6% | 2 | 6 |

| CALL | 50 | 2026-07-17 | 13.2 | 15.1 | - | 63.9% | - | - |

| PUT | 50 | 2026-07-17 | - | 0.95 | - | 48.3% | - | 3 |

| CALL | 55 | 2026-07-17 | 8.5 | 10.4 | - | 60.0% | - | - |

| PUT | 55 | 2026-07-17 | - | 2.4 | - | 31.7% | - | 3 |

| CALL | 56 | 2026-07-17 | 7.6 | 9.5 | - | 59.0% | - | - |

| PUT | 56 | 2026-07-17 | - | 1.75 | - | 27.8% | - | - |

| CALL | 57 | 2026-07-17 | 6.2 | 8.5 | - | 45.4% | - | - |

| PUT | 57 | 2026-07-17 | - | 1.9 | - | 24.9% | - | 5 |

| CALL | 58 | 2026-07-17 | 5.3 | 7.5 | - | 42.5% | - | - |

| PUT | 58 | 2026-07-17 | 0.2 | 0.65 | - | 46.4% | - | 648 |

| CALL | 59 | 2026-07-17 | 4.7 | 6.8 | - | 48.3% | - | - |

| PUT | 59 | 2026-07-17 | 0.1 | 2.3 | - | 62.9% | - | 5 |

| CALL | 60 | 2026-07-17 | 4.4 | 5.4 | 5.0 | 46.4% | 2 | 10 |

| PUT | 60 | 2026-07-17 | 0.45 | 1.2 | - | 46.4% | - | 610 |

| CALL | 61 | 2026-07-17 | 3.0 | 5.5 | - | 47.3% | - | - |

| PUT | 61 | 2026-07-17 | 0.1 | 2.6 | - | 51.2% | - | 2 |

| CALL | 62 | 2026-07-17 | 2.35 | 5.3 | - | 52.2% | - | - |

| PUT | 62 | 2026-07-17 | 0.35 | 2.85 | - | 49.3% | - | - |

| CALL | 63 | 2026-07-17 | 1.65 | 4.4 | - | 47.3% | - | - |

| PUT | 63 | 2026-07-17 | 0.8 | 3.9 | - | 56.1% | - | 85 |

| CALL | 64 | 2026-07-17 | 1.1 | 3.2 | 3.25 | 40.5% | - | 2 |

| PUT | 64 | 2026-07-17 | 1.2 | 4.1 | - | 52.2% | - | - |

| CALL | 65 | 2026-07-17 | 0.55 | 3.1 | - | 43.4% | - | - |

| PUT | 65 | 2026-07-17 | 1.7 | 4.3 | - | 48.3% | - | - |

| CALL | 66 | 2026-07-17 | 0.35 | 3.0 | - | 48.3% | - | - |

| PUT | 66 | 2026-07-17 | 2.3 | 4.7 | 2.98 | 46.4% | 1 | 123 |

| CALL | 67 | 2026-07-17 | 0.05 | 2.8 | 4.2 | 49.3% | - | 2 |

| PUT | 67 | 2026-07-17 | 2.95 | 5.4 | - | 46.4% | - | 41 |

| CALL | 68 | 2026-07-17 | 0.05 | 2.45 | 3.9 | 52.2% | - | 11 |

| PUT | 68 | 2026-07-17 | 3.7 | 6.3 | - | 48.3% | - | 2 |

| CALL | 69 | 2026-07-17 | - | 2.3 | 3.35 | 16.1% | - | - |

| PUT | 69 | 2026-07-17 | 4.7 | 7.0 | - | 51.2% | - | - |

| CALL | 70 | 2026-07-17 | 0.2 | 0.75 | 0.6 | 42.5% | - | 1382 |

| PUT | 70 | 2026-07-17 | 5.8 | 7.0 | - | 43.4% | - | 96 |

| CALL | 71 | 2026-07-17 | - | 1.9 | - | 22.0% | - | - |

| PUT | 71 | 2026-07-17 | 6.3 | 8.3 | - | 45.4% | - | - |

| CALL | 72 | 2026-07-17 | - | 1.75 | 1.07 | 23.9% | - | 12 |

| PUT | 72 | 2026-07-17 | 7.2 | 9.6 | - | 52.2% | - | 10 |

| CALL | 73 | 2026-07-17 | - | 0.75 | 0.97 | 26.9% | - | 5 |

| PUT | 73 | 2026-07-17 | 8.1 | 10.5 | - | 53.2% | - | 36 |

| CALL | 74 | 2026-07-17 | 0.05 | 0.5 | 1.15 | 51.2% | - | 61 |

| PUT | 74 | 2026-07-17 | 9.1 | 11.6 | - | 59.0% | - | 1 |

| CALL | 75 | 2026-07-17 | - | 1.4 | 5.0 | 31.7% | - | 1 |

| PUT | 75 | 2026-07-17 | 10.0 | 12.3 | - | 54.2% | - | - |

| CALL | 76 | 2026-07-17 | - | 0.75 | 0.98 | 33.7% | - | 19 |

| PUT | 76 | 2026-07-17 | 10.6 | 13.0 | - | 1.5% | - | - |

| CALL | 80 | 2026-07-17 | - | 0.2 | 0.05 | 42.5% | - | 113 |

| PUT | 80 | 2026-07-17 | 15.6 | 16.6 | - | 67.8% | - | 5 |

| CALL | 85 | 2026-07-17 | - | 1.2 | 0.2 | 52.2% | - | 2675 |

| PUT | 85 | 2026-07-17 | 19.7 | 22.1 | - | 59.0% | - | - |

| CALL | 90 | 2026-07-17 | - | 0.75 | 0.05 | 62.0% | - | 4 |

| PUT | 90 | 2026-07-17 | 24.4 | 27.5 | - | 80.5% | - | - |

| CALL | 95 | 2026-07-17 | - | 0.75 | 0.15 | 70.8% | - | 2423 |

| PUT | 95 | 2026-07-17 | 29.6 | 32.4 | - | 98.1% | - | - |

| CALL | 100 | 2026-07-17 | - | 0.05 | 0.05 | 78.6% | - | 109 |

| PUT | 100 | 2026-07-17 | 34.4 | 37.5 | - | 102.9% | - | - |

| CALL | 105 | 2026-07-17 | - | 0.1 | 0.05 | 86.4% | - | 88 |

| PUT | 105 | 2026-07-17 | 39.4 | 42.5 | - | 113.7% | - | - |

| CALL | 110 | 2026-07-17 | - | 0.05 | 0.05 | 93.2% | - | 116 |

| PUT | 110 | 2026-07-17 | 44.4 | 47.5 | - | 123.4% | - | - |

| CALL | 115 | 2026-07-17 | - | 0.75 | 0.05 | 100.0% | - | 62 |

| PUT | 115 | 2026-07-17 | 49.4 | 52.5 | - | 133.2% | - | - |

| CALL | 40 | 2026-08-21 | 22.8 | 25.7 | - | 58.1% | - | - |

| PUT | 40 | 2026-08-21 | - | 0.95 | - | 48.3% | - | - |

| CALL | 45 | 2026-08-21 | 18.3 | 20.7 | - | 60.0% | - | - |

| PUT | 45 | 2026-08-21 | - | 0.95 | - | 36.6% | - | - |

| CALL | 50 | 2026-08-21 | 13.8 | 15.7 | - | 52.2% | - | - |

| PUT | 50 | 2026-08-21 | - | 2.15 | - | 26.9% | - | - |

| CALL | 55 | 2026-08-21 | 8.7 | 11.2 | - | 40.5% | - | - |

| PUT | 55 | 2026-08-21 | - | 2.6 | - | 17.1% | - | - |

| CALL | 58 | 2026-08-21 | 6.6 | 9.0 | - | 43.4% | - | - |

| PUT | 58 | 2026-08-21 | 0.55 | 3.5 | - | 50.3% | - | - |

| CALL | 59 | 2026-08-21 | 5.9 | 8.3 | - | 43.4% | - | - |

| PUT | 59 | 2026-08-21 | 0.75 | 3.8 | - | 49.3% | - | - |

| CALL | 60 | 2026-08-21 | 5.1 | 7.7 | - | 42.5% | - | - |

| PUT | 60 | 2026-08-21 | 1.1 | 4.0 | - | 48.3% | - | - |

| CALL | 61 | 2026-08-21 | 4.5 | 7.2 | - | 43.4% | - | - |

| PUT | 61 | 2026-08-21 | 1.5 | 4.3 | - | 47.3% | - | - |

| CALL | 62 | 2026-08-21 | 4.0 | 6.6 | - | 43.4% | - | - |

| PUT | 62 | 2026-08-21 | 1.9 | 4.7 | - | 47.3% | - | - |

| CALL | 63 | 2026-08-21 | 3.4 | 6.1 | - | 43.4% | - | - |

| PUT | 63 | 2026-08-21 | 2.35 | 5.0 | - | 46.4% | - | - |

| CALL | 64 | 2026-08-21 | 2.85 | 5.6 | - | 43.4% | - | - |

| PUT | 64 | 2026-08-21 | 2.8 | 5.2 | - | 44.4% | - | - |

| CALL | 65 | 2026-08-21 | 2.35 | 5.1 | - | 42.5% | - | - |

| PUT | 65 | 2026-08-21 | 3.3 | 6.1 | - | 45.4% | - | - |

| CALL | 66 | 2026-08-21 | 1.9 | 4.6 | - | 42.5% | - | - |

| PUT | 66 | 2026-08-21 | 3.9 | 6.7 | - | 46.4% | - | 3 |

| CALL | 67 | 2026-08-21 | 1.6 | 4.2 | - | 42.5% | - | - |

| PUT | 67 | 2026-08-21 | 4.4 | 7.2 | - | 45.4% | - | - |

| CALL | 68 | 2026-08-21 | 1.1 | 3.9 | - | 41.5% | - | - |

| PUT | 68 | 2026-08-21 | 5.1 | 7.7 | - | 44.4% | - | - |

| CALL | 69 | 2026-08-21 | 0.95 | 3.8 | 1.75 | 44.4% | - | 1 |

| PUT | 69 | 2026-08-21 | 5.8 | 8.4 | - | 44.4% | - | - |

| CALL | 70 | 2026-08-21 | 0.65 | 3.6 | 2.9 | 44.4% | - | 1 |

| PUT | 70 | 2026-08-21 | 6.4 | 9.0 | - | 43.4% | - | - |

| CALL | 71 | 2026-08-21 | 0.65 | 3.2 | 2.0 | 45.4% | - | 1 |

| PUT | 71 | 2026-08-21 | 7.2 | 9.7 | - | 43.4% | - | - |

| CALL | 72 | 2026-08-21 | 0.35 | 2.85 | 1.68 | 44.4% | 1 | 3 |

| PUT | 72 | 2026-08-21 | 7.9 | 10.0 | - | 40.5% | - | - |

| CALL | 73 | 2026-08-21 | 0.55 | 2.6 | 1.55 | 46.4% | 2 | 2 |

| PUT | 73 | 2026-08-21 | 8.9 | 11.1 | - | 43.4% | - | - |

| CALL | 74 | 2026-08-21 | 0.1 | 2.4 | 1.3 | 44.4% | 1 | 1 |

| PUT | 74 | 2026-08-21 | 9.7 | 11.9 | - | 43.4% | - | - |

| CALL | 75 | 2026-08-21 | - | 2.3 | 0.7 | 17.1% | - | 10 |

| PUT | 75 | 2026-08-21 | 10.4 | 12.4 | - | 39.5% | - | - |

| CALL | 76 | 2026-08-21 | - | 2.15 | 1.02 | 18.1% | - | 1 |

| PUT | 76 | 2026-08-21 | 11.3 | 13.7 | - | 43.4% | - | - |

| CALL | 77 | 2026-08-21 | - | 2.0 | 0.97 | 19.0% | - | 1 |

| PUT | 77 | 2026-08-21 | 12.0 | 14.3 | - | 39.5% | - | - |

| CALL | 78 | 2026-08-21 | - | 1.95 | - | 21.0% | - | - |

| PUT | 78 | 2026-08-21 | 12.8 | 15.2 | - | 37.6% | - | - |

| CALL | 80 | 2026-08-21 | - | 1.75 | - | 23.0% | - | - |

| PUT | 80 | 2026-08-21 | 14.7 | 17.1 | - | 39.5% | - | - |

| CALL | 85 | 2026-08-21 | - | 0.75 | - | 28.8% | - | - |

| PUT | 85 | 2026-08-21 | 19.6 | 22.9 | - | 57.1% | - | - |

| CALL | 35 | 2026-10-16 | 28.3 | 31.1 | - | 67.8% | - | - |

| PUT | 35 | 2026-10-16 | 0.15 | 1.3 | - | 80.5% | - | 1 |

| CALL | 40 | 2026-10-16 | 23.5 | 26.4 | 25.0 | 61.0% | - | 4 |

| PUT | 40 | 2026-10-16 | 0.2 | 1.55 | - | 69.8% | - | 11 |

| CALL | 45 | 2026-10-16 | 19.0 | 20.9 | 23.9 | 47.3% | - | 2 |

| PUT | 45 | 2026-10-16 | 0.45 | 1.4 | 1.34 | 56.1% | 2 | 22 |

| CALL | 50 | 2026-10-16 | 14.0 | 17.1 | 21.26 | 45.4% | - | 9 |

| PUT | 50 | 2026-10-16 | 0.05 | 2.85 | - | 51.2% | - | 27 |

| CALL | 55 | 2026-10-16 | 9.5 | 12.8 | - |

…(truncated)…

MCP tool: price_option_path

{"option_path": [1.2768676255130949, 1.5295781986071315, 1.850717855298182, 2.1393764315508506, 2.54463164992535, 3.059455354182866, 3.6499022019563796, 4.162649173174692, 4.54467601618326, 5.153181399220529], "volatility_used": 0.3260625865052725, "symbol": "EZA"}

MCP tool: price_option_path

{"option_path": [2.0780638239247793, 3.0787967760805657, 4.503241737555424, 5.699296951156072, 7.14824941135133, 8.839476648645551, 9.76598891753958, 10.752635060878738, 11.781306304576184, 12.831247920612569, 13.887105648865763, 14.943522168239369], "volatility_used": 0.3260625865052725, "symbol": "EZA"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.