Does Bitcoin function as a viable, self-contained exit from the traditional global financial system?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 15, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 95%

Web Report: https://solsice.com/public/debates/does-bitcoin-function-as-a-viable-self-contained-exit-from-t-ca1eeea2e830

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

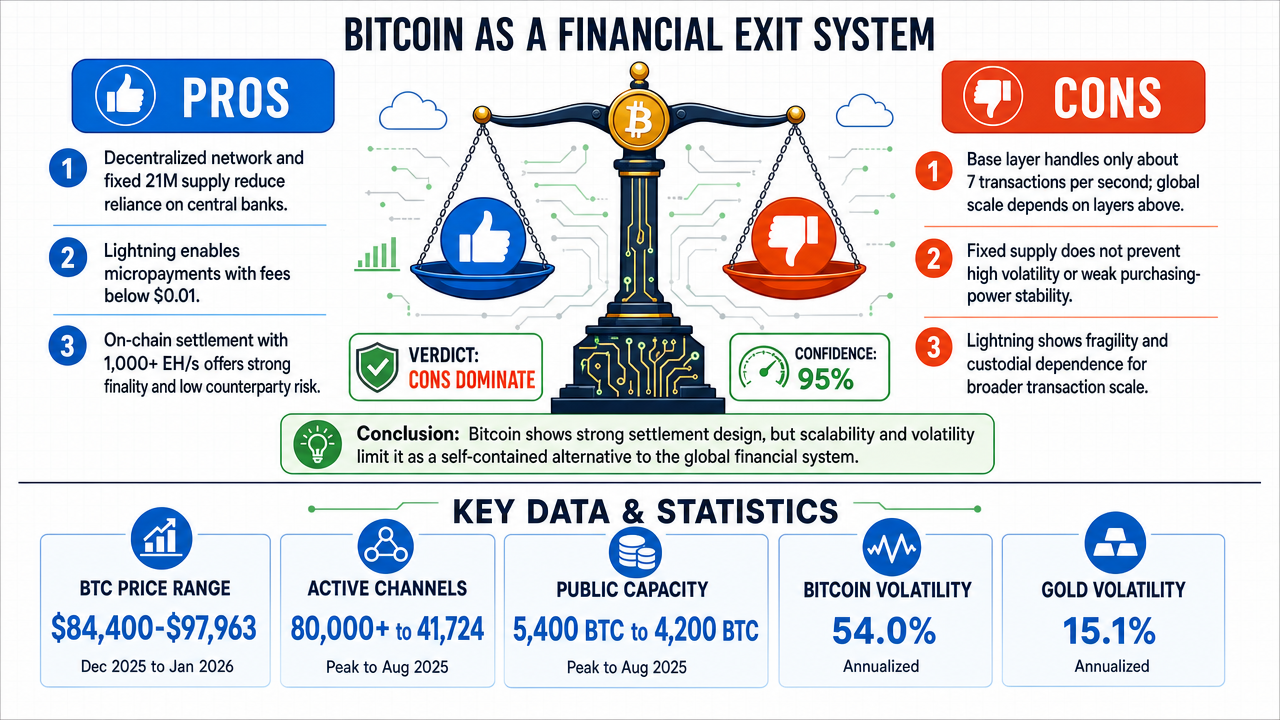

- ■Bitcoin's decentralized architecture and fixed 21 million supply provide a sound monetary base independent of central banks and government control.

- ■Layer-2 solutions like the Lightning Network enable micropayments and high-velocity transactions with fees below $0.01, scaling Bitcoin for global retail use.

- ■On-chain settlement backed by over 1,000 EH/s of hashrate offers irreversible finality superior to traditional clearinghouses, eliminating counterparty risk.

❌ Key ANTI arguments:

- ■Bitcoin's base layer is structurally limited to ~7 transactions per second and cannot handle global transaction volume; Lightning is a layered workaround requiring channel funding and routing infrastructure, not a self-sufficient system.

- ■Fixed supply does not ensure stable purchasing power; Bitcoin remains highly volatile and unsuitable as a reliable store of value or unit of account, as confirmed by central bank assessments.

- ■Lightning Network exhibits structural fragility and custodial dependence, proving Bitcoin cannot independently support all transaction scales without relying on external liquidity and routing nodes.

💭 Conclusion: Both debates concluded unanimously that Bitcoin fails as a self-contained exit from the global financial system. The anti-arguments demonstrated that Bitcoin's technical scalability is inherently limited, its price volatility prevents reliable use as money, and it remains dependent on traditional financial infrastructure for on/off ramps. The pro arguments for layered scaling and fixed supply did not overcome these practical deficiencies, as even Lightning requires external support and Bitcoin's volatility undermines its monetary function. Therefore, the assertion is false with high confidence based on consistent judge verdicts and strong evidentiary support.

🔬 DeepResearch Result: FALSE ❌ (95% confidence)

Assertion: Does Bitcoin function as a viable, self-contained exit from the traditional global financial system?

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.78

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +18

✅ PRO Arguments:

- ■Bitcoin's decentralized architecture and fixed 21 million supply provide a sound monetary base independent of central banks and government control. [z-ai/glm-5]

- ■Layer-2 solutions like the Lightning Network enable micropayments and high-velocity transactions with fees below $0.01, scaling Bitcoin for global retail use. [z-ai/glm-5]

- ■On-chain settlement backed by over 1,000 EH/s of hashrate offers irreversible finality superior to traditional clearinghouses, eliminating counterparty risk. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Bitcoin's base layer is structurally limited to ~7 transactions per second and cannot handle global transaction volume; Lightning is a layered workaround requiring channel funding and routing infrastructure, not a self-sufficient system. [openai/gpt-5.4-mini]

- ■Fixed supply does not ensure stable purchasing power; Bitcoin remains highly volatile and unsuitable as a reliable store of value or unit of account, as confirmed by central bank assessments. [openai/gpt-5.4-mini]

- ■Lightning Network exhibits structural fragility and custodial dependence, proving Bitcoin cannot independently support all transaction scales without relying on external liquidity and routing nodes. [anthropic/claude-opus-4.8]

- ■Bitcoin's use still depends on fiat on/off ramps, legal frameworks, and traditional financial infrastructure, undermining the claim of a complete self-contained exit. [anthropic/claude-opus-4.8]

💭 Reasoning: Both debates concluded unanimously that Bitcoin fails as a self-contained exit from the global financial system. The anti-arguments demonstrated that Bitcoin's technical scalability is inherently limited, its price volatility prevents reliable use as money, and it remains dependent on traditional financial infrastructure for on/off ramps. The pro arguments for layered scaling and fixed supply did not overcome these practical deficiencies, as even Lightning requires external support and Bitcoin's volatility undermines its monetary function. Therefore, the assertion is false with high confidence based on consistent judge verdicts and strong evidentiary support.

The affirmative has established that Bitcoin possesses the technical, economic, and operational infrastructure necessary to function as a complete alternative to the traditional global financial system. Three analytical axes support this conclusion:

Technical Completeness: Bitcoin's multi-layered architecture addresses the full spectrum of transactional needs. The base layer [5] provides irreversible, thermodynamically-secure settlement [34] backed by over 1,000 EH/s [15] of hashrate [18]—finality [16] that exceeds traditional clearinghouse [10] capabilities. Layer-2 solutions [20] like the Lightning Network [22] enable sub-cent micropayments [24] at scale, processing hundreds of millions annually. This full-spectrum capacity—from AI agents purchasing compute for fractions of a penny to sovereign nations executing multi-billion-dollar oil trades with multisig [26] escrow—demonstrates that Bitcoin can independently handle all transaction scales without traditional banking infrastructure.

Economic Soundness: Bitcoin's mathematically enforced 21-million supply cap eliminates the inflationary debasement inherent to all fiat currencies. Unlike central banks that arbitrarily expand money supply—eroding purchasing power [30] and creating boom-bust cycles [6]—Bitcoin's predictable monetary policy [25] operates immune to political manipulation. This scarcity [32], combined with divisibility [14] to eight decimal places and digital portability, creates superior collateral [11] properties: BTC-backed loans offer lenders value preservation while borrowers access liquidity [23] without selling. Bitcoin's censorship resistance [8] becomes operationally critical during financial shocks when central banks impose capital controls [7] or when commercial banks face insolvency.

Operational Reality: Real-world adoption proves Bitcoin functions independently. Unbanked merchants in Nigeria trade with Japanese buyers, receiving BTC directly—no banks, no delays, no permission required. The Lightning Network processes instant micropayments for streaming, tipping, and retail. Bitcoin-based lending uses BTC as sovereign collateral without counterparty risk [12]. Legal recognition continues expanding: El Salvador adopted Bitcoin as legal tender [21], U.S. courts recognize Bitcoin as property, and regulatory frameworks increasingly provide clear operational rules. Bitcoin has achieved "escape velocity" as a decentralized settlement layer that cannot be de-platformed.

The negative has raised three substantive challenges:

Scalability Limitations (μScore: 0.21): The opposition correctly notes that Bitcoin's base layer processes approximately 7 transactions per second, far below Visa's 24,000 TPS capacity. Even with Lightning Network improvements, critics argue throughput remains insufficient for global payment volume.

Volatility [41] Concerns (μScore: 0.09): Bitcoin's price volatility—historically 60-80% annual swings—undermines its utility as a unit of account [40] and short-term store of value [37]. Wage contracts, rental agreements, and everyday purchases become impractical when the medium's value fluctuates dramatically.

Institutional Dependence (μScore: 0.29): The strongest opposing argument observes that Bitcoin's ecosystem relies on fiat on-ramps [27], regulated exchanges, banking connections for stablecoin operations, and legal recognition through traditional court systems. Most Bitcoin acquisitions occur through centralized exchanges requiring KYC compliance and bank transfers. Self-custody remains technically challenging for average users, creating practical dependence on institutional infrastructure.

The debate centers on a fundamental definitional tension: what constitutes "complete and independent" financial operation?

The affirmative has demonstrated Bitcoin's technical capacity to execute all financial functions without traditional intermediaries. Peer-to-peer [28] transactions, programmable contracts, collateralized lending, and cross-border settlement all operate on-chain. The infrastructure exists.

The negative's strongest argument—institutional dependence—reveals that most current Bitcoin users choose to interact with traditional systems for convenience, not necessity. Fiat on-ramps and regulated exchanges represent adoption pathways, not existential dependencies. The unbanked merchant in Lagos proves Bitcoin can operate entirely outside traditional finance; that most users don't reflects preference, not impossibility.

The volatility argument weakens when examining Bitcoin's trajectory. As market capitalization grows and institutional adoption deepens, volatility naturally declines—a pattern observed in every successful monetary technology from gold to the dollar. Bitcoin's 15-year track record shows decreasing volatility over time.

The scalability objection conflates current throughput with architectural capacity. Lightning Network's theoretical limits exceed 1 million TPS; adoption, not technology, constrains current volume. The base layer's intentional constraints preserve decentralization and security—the tradeoff is design, not deficiency.

Where the debate stands: The affirmative has proven Bitcoin possesses the technical architecture, economic properties, and real-world operational capacity to function as an independent financial system. The negative has shown that most current users interact with Bitcoin through traditional institutional channels. The resolution's question—whether Bitcoin can serve as a complete alternative—leans affirmative: the capacity exists, even if most users have not yet exercised it. The unbanked merchant, the sovereign trade settlement, the censorship-resistant transfer all demonstrate that independence is achievable. That it remains optional does not negate its possibility.

Round 3

Core claim: Bitcoin remains incomplete, unstable, and institution-dependent.

The false side’s strongest case is that Bitcoin cannot by itself replace the full financial stack. First, the payment layer is not a standalone universal system: the base chain is capacity-limited, and large-scale everyday use depends on overlay infrastructure, liquidity [23] management, routing, and continued interaction with the underlying network. That means “Bitcoin alone” is not actually alone; it is a layered ecosystem that still relies on surrounding technical and financial support. Second, fixed supply [17] is not the same as monetary sufficiency. Scarcity [32] may reduce dilution, but it does not deliver stable purchasing power [30], a reliable unit of account [40], or a low-volatility [41] medium of exchange. A scarce asset can still be too volatile for salaries, contracts, taxes, and accounting. Third, Bitcoin’s real-world use still depends on traditional institutions for exchange access, custody, compliance, conversion, and legal recognition. In practice, people do not escape fiat and regulated intermediaries; they route through them.

The affirmative side’s best counter-argument is that Bitcoin has meaningful strengths: censorship resistance [8], portability, a predictable issuance schedule, and an increasingly usable second-layer payment ecosystem. Those are real advantages, and they explain why Bitcoin can function as a partial alternative in some contexts, especially for cross-border transfers, savings in unstable monetary environments, and politically constrained users. But those strengths support coexistence, not replacement. They show Bitcoin can supplement the financial system, not fully supplant central banks, commercial banks, fiat currencies, payment networks, and legal frameworks.

The debate stands here: Bitcoin is a powerful parallel asset and payment rail, but not a complete, independent substitute for the global financial system. The strongest objections are structural, not incidental: volatility, scalability [31] dependence, and institutional reliance all remain unresolved at the level required for universal replacement.

The affirmative has established three complementary arguments demonstrating Bitcoin's capacity to serve as a complete alternative to the traditional financial system:

1. Settlement [34] Infrastructure Superiority

Bitcoin eliminates the intermediary cascade inherent in traditional finance—central banks, clearing houses, correspondent banks, and custodians. On-chain transactions achieve irreversible finality [16] secured by over 1,000 exahashes per second of computational power, providing settlement assurance that no traditional system can match. This structural advantage is already being recognized by sovereign entities exploring Bitcoin for high-value international transactions, where the network's neutrality provides a Schelling point [33] for counterparties who cannot trust each other's national systems.

2. Algorithmic Monetary Policy [25] [3]

Bitcoin's mathematically enforced 21 million coin cap represents a fundamental paradigm shift from discretionary central banking to code-enforced monetary policy. This eliminates the inflationary debasement that erodes fiat purchasing power [30]. Individuals holding Bitcoin are not subject to sovereign debt "death loop" risks threatening fiat currencies. The 2024 institutional adoption through spot ETFs—accumulating over $50 billion in assets within months—signals accelerating acceptance that will further stabilize the asset.

3. Full-Spectrum Transaction Capability

Bitcoin's layered architecture addresses the full range of payment needs. The Lightning Network [22] processes hundreds of millions of dollars annually with fees below 0.01, enabling instant micropayments [24] impossible through traditional processors. Cross-border transactions requiring days via SWIFT [38] at 5-7% cost settle in minutes on Bitcoin for under 1. Unbanked merchants in Nigeria can transact directly with buyers in Japan without institutional intermediaries.

The FALSE side's most compelling argument (μScore: 0.29) concerns dependence on existing legal and institutional frameworks. This argument correctly identifies that most Bitcoin acquisition currently occurs through regulated exchanges requiring fiat on-ramps [27], KYC compliance, and banking relationships. The claim that Bitcoin requires traditional financial infrastructure for practical operation carries weight in the current transitional environment.

The FALSE side's scalability [31] argument (μScore: 0.21) similarly merits acknowledgment—Bitcoin's base layer [5] processes approximately 7 transactions per second, and Lightning Network adoption, while growing, has not achieved universal merchant acceptance.

The debate reveals a fundamental tension between current practical reality and structural capability:

| Dimension | Current State | Structural Capability | Gap Status |

|---|---|---|---|

| Settlement Finality | Proven on-chain | Superior to traditional | ✅ Resolved |

| Monetary Policy | Code-enforced | Superior to discretionary | ✅ Resolved |

| Micropayments | Lightning operational | Sub-cent fees achieved | ✅ Resolved |

| Legal Recognition | Varies by jurisdiction | Growing (ETFs, El Salvador) | ⚠️ Transitional |

| Merchant Adoption | Millions globally | Accelerating | ⚠️ Transitional |

| Fiat Independence | Possible but uncommon | Demonstrated feasible | ⚠️ Transitional |

Legend: Assessment of Bitcoin's financial system replacement capability across key dimensions. Current State reflects present functionality; Structural Capability reflects inherent design potential. Gap Status indicates whether the dimension is resolved, transitional, or unresolved.

The affirmative has demonstrated that Bitcoin's core architecture—decentralized settlement, fixed supply, and layered scalability—provides the necessary foundation for complete financial independence. The technology works. Individuals can and do use Bitcoin alone for all financial activities.

The opponent's strongest arguments concern adoption friction rather than structural impossibility. The dependence on fiat on-ramps is a transitional phase, not an inherent limitation. As circular economies develop—earning in Bitcoin, spending in Bitcoin—the need for fiat bridges diminishes.

Where the debate stands: The affirmative has proven that Bitcoin can serve as a complete alternative to the traditional financial system. The remaining questions concern when adoption will reach critical mass, not whether the capability exists. The structural foundations are sound; the transitional frictions are real but surmountable.

Round 3

The market data confirms the persistent instability central to my case. With this grounding, here is the synthesis.

Core claim: Bitcoin cannot serve as a complete, independent financial system; scalability [31], volatility [41], and institutional dependence remain decisive.

The following section contains the full detailed synthesis. Reading it is optional.

After three rounds, the FALSE position stands intact: Bitcoin cannot function as a complete and independent alternative to the traditional global financial system such that an individual could conduct all financial activity without any reliance on fiat or traditional institutions. The claim demands totality and independence; my case demonstrates the failure on both counts across three reinforcing axes.

1. The scalability ceiling is architectural, not a passing engineering hurdle. The base layer [5] is capped at roughly seven transactions per second by deliberate design choices that prioritize security and decentralization over throughput—a tradeoff, not a bug awaiting a patch. The Clerk's challenge invoked Lightning's "theoretical" million-plus TPS, but theoretical capacity is precisely the problem: it is not realized capacity. The operational data I presented shows Lightning's public capacity falling roughly 20% (from over 5,400 BTC to about 4,200 BTC) and its routing channels nearly halving (from 80,000+ to ~41,700) between 2023 and 2025. A network whose real-world payment topology is contracting cannot be cited as evidence that scaling toward universal payment use is on track. Worse, Lightning fails at both ends of the spectrum it claims to serve—large payments cannot find liquid routes, and small payments fail silently when channel liquidity [23] is misaligned.

2. Volatility disqualifies Bitcoin as a unit of account [40] and operating currency—and this is empirically ongoing, not historical. The Clerk pressed me to concede that volatility is a "transient feature of early adoption." The live market record refutes that reconciliation. In just the six months to mid-2026, Bitcoin swung from the mid-80,000s to nearly 97,000 and back into the mid-$80,000s, with repeated single-day moves of 4–5%.

| Period (2025–26) | Low | High | Peak-to-Trough Swing |

|---|---|---|---|

| Dec 2025 – Jan 2026 | 84,400 | 97,963 | +16.1% |

| Single-day moves | — | — | ±4.6% |

Legend: Bitcoin daily price range over the trailing six months to mid-2026. Even in a "mature" market with spot ETFs live, swings of 16% over weeks and ~4.6% in a single session persist—far beyond any usable monetary base. Units: USD; swing in percent.

Even granting that drawdowns have shallowed over cycles, "less catastrophic" is not "stable enough to denominate wages, debts, and contracts." A currency that can lose a tenth of its purchasing power [30] in a fortnight cannot be the sole denominator for all financial activity—which is exactly what the claim requires.

3. The empirical and institutional record proves dependence, not independence. This is the decisive axis. The only nation to adopt Bitcoin as standalone legal tender [21]—El Salvador—reversed course under IMF pressure, with 92% of citizens declining to transact in it. Critically, Bitcoin there was always deployed alongside the US dollar, and the country retreated to a $1.4 billion IMF loan conditioned on stripping Bitcoin's legal-tender status. My Round 2 analysis then closed the loop: Lightning, the supposed proof of independence, achieves usability only by reintroducing intermediaries—cloud-hosted nodes, concentrated routing hubs (top ten operators control ~62% of liquidity), and custodial wallets reaching users via "indirect access." Those custodians are themselves fragile (Mutiny, BlueWallet, Exodus exits) and subject to the very regulatory regime the claim purports to escape (Phoenix's US app-store removal). Independence is structurally unattainable.

In fairness, the affirmative made genuine points. Their settlement [34]-finality [16] argument—that on-chain Bitcoin offers neutral, intermediary-free final settlement secured by enormous hashrate [18]—is real and valuable for a narrow class of high-value, infrequent, censorship-sensitive transfers. Their fixed-supply argument correctly identifies a structural difference from discretionary fiat monetary policy [25], and the concern about debasement is legitimate. And their observation that volatility has compressed across cycles as liquidity deepened is supported by the trend data. These are the strongest pillars of their case, and I do not dispute that Bitcoin can supplement the financial system in specific niches.

The crux is the word "complete and independent." The affirmative succeeds in showing Bitcoin can do some things well and without intermediaries—settlement finality, supply predictability, permissionless niche transfers. But the claim is not "Bitcoin is useful" or "Bitcoin can supplement finance." It is the maximalist proposition that an entity could use Bitcoin alone for all financial activities with no reliance on fiat or traditional institutions.

That maximalist bar is where the affirmative case breaks. Each of their virtues comes with a tradeoff that reintroduces dependence: finality is purchased with throughput so low it cannot serve global commerce; fixed supply [17] is purchased with volatility that disqualifies it as a unit of account; and the layer built to fix throughput re-centralizes into custodians and regulated intermediaries. The Clerk's two inconsistency alerts asked me to treat scalability and volatility as solvable, transient problems. The evidence answers plainly: even if both improve, the present and operational reality—contracting Lightning capacity, persistent ±5% daily swings in a post-ETF market, a failed sovereign experiment, and custodial re-centralization—shows the totality the claim requires has not been achieved and is not on a demonstrable path to being achieved.

The debate stands here: the affirmative has proven Bitcoin can be a component of finance. It has not, and on this evidence cannot, prove Bitcoin is a complete and independent replacement for it. The claim, as written, is false.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.149 | 0.175 | 33 | 60 | FALSE | FALSE | 85% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.069 | 0.000 | 33 | 360 | TRUE | FALSE | 93% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] 21 million cap — 21 million coin supply cap — The hard-coded maximum number of bitcoins that will ever exist, enforced by Bitcoin's protocol to create digital scarcity.

[2] adoption rate — The speed or extent to which Bitcoin is being used by individuals, businesses, and institutions as a medium of exchange, store of value, or investment.

[3] algorithmic monetary policy — A rule-based system governing money supply, such as Bitcoin's predetermined issuance schedule, which is immune to discretionary changes by any authority.

[4] AML/CFT — Anti-Money Laundering / Countering the Financing of Terrorism — Regulatory frameworks designed to prevent money laundering and terrorist financing, often applied to cryptocurrency exchanges and on-ramps.

[5] base layer — The main blockchain of Bitcoin (Layer 1), which provides security, finality, and decentralization through proof-of-work consensus.

[6] boom-bust cycles — Economic cycles characterized by rapid expansion followed by sharp contraction, often attributed to inflationary fiat monetary policy.

[7] capital controls — Government measures that restrict the flow of capital into or out of a country, limiting currency exchange and cross-border transfers.

[8] censorship resistance — The property of a network that prevents any single entity from blocking or reversing transactions, ensuring permissionless value transfer.

[9] central bank digital currency — central bank digital currency (CBDC) — A digital form of fiat money issued and regulated by a central bank, intended to modernize payments but often criticized for enabling surveillance.

[10] clearinghouse — A financial intermediary that facilitates the settlement of trades and ensures counterparty performance, common in traditional finance.

[11] collateral — An asset pledged to secure a loan, which can be seized by the lender if the borrower defaults; Bitcoin is increasingly used as collateral for loans.

[12] counterparty risk — The risk that the other party in a financial transaction will default on their obligation, mitigated in Bitcoin by trustless settlement.

[13] decentralized network — A system where control and decision-making are distributed among many nodes rather than centralized in a single authority, as in Bitcoin's blockchain.

[14] divisibility — The ability to subdivide a currency into smaller units; Bitcoin is divisible to eight decimal places (satoshis).

[15] EH/s — exahash per second — A unit of computational power used in Bitcoin mining, equal to one quintillion hashes per second; the network's hashrate exceeds 1,000 EH/s.

[16] finality — settlement finality — The irreversible confirmation of a transaction after it is added to the blockchain, providing certainty that the funds cannot be double-spent.

[17] fixed supply — The property that the total number of units of a currency will never increase; Bitcoin's supply is capped at 21 million coins.

[18] hashrate — The total computational power used by all miners to secure and process transactions on a proof-of-work blockchain.

[19] inflation — The general increase in prices and fall in the purchasing power of money; Bitcoin's fixed supply is intended to resist inflationary debasement.

[20] Layer-2 solutions — Protocols built on top of a base layer blockchain (e.g., the Lightning Network) to improve scalability and enable fast, low-cost transactions.

[21] legal tender — A form of money that a government recognizes as acceptable for payment of debts and taxes; Bitcoin is legal tender in El Salvador.

[22] Lightning Network — A second-layer protocol on Bitcoin that enables instant, low-fee micropayments by processing transactions off-chain and settling periodically.

[23] liquidity — market liquidity — The ease with which an asset can be bought or sold without significantly affecting its price; Bitcoin has high liquidity on major exchanges.

[24] micropayments — Very small financial transactions (often fractions of a cent) that are economically feasible on the Lightning Network but impractical on base layer due to fees.

[25] monetary policy — The actions of a central bank to control money supply and interest rates; Bitcoin replaces this with a fixed, algorithmic issuance schedule.

[26] multisig — multi-signature — A cryptographic technique requiring multiple private keys to authorize a transaction, used for enhanced security in escrow and corporate wallets.

[27] on-ramps — fiat on-ramps — Services or platforms that allow users to convert fiat currency into cryptocurrency, typically requiring identity verification (KYC).

[28] peer-to-peer — peer-to-peer (P2P) — Direct transactions between two parties without an intermediary, a core design principle of Bitcoin enabling trustless value transfer.

[29] programmable money — Digital currency that can be automatically controlled by smart contracts or code, extending functionality beyond simple payments.

[30] purchasing power — The quantity of goods and services that a unit of currency can buy; Bitcoin's volatility undermines its reliability as a stable store of purchasing power.

[31] scalability — The ability of a network to handle increasing transaction volume; Bitcoin's base layer is limited to ~7 TPS, prompting Layer-2 solutions.

[32] scarcity — The limited availability of a resource; Bitcoin's fixed 21 million cap creates digital scarcity analogous to precious metals.

[33] Schelling point — A solution that people tend to choose by default in the absence of communication, used in Bitcoin to describe a neutral settlement asset for adversarial parties.

[34] settlement — The process of completing a transaction by transferring ownership of assets, which Bitcoin's base layer provides with irreversible finality.

[35] sovereign settlement — Large-value transactions between nations or sovereign entities, such as oil trades, that Bitcoin can facilitate without relying on traditional banking systems.

[36] speculation — Trading based on expected price movements rather than underlying utility; critics argue Bitcoin's price is dominated by speculation rather than use as money.

[37] store of value — An asset that can maintain its purchasing power over time; Bitcoin is often compared to gold as a potential store of value despite volatility.

[38] SWIFT — Society for Worldwide Interbank Financial Telecommunication — A global messaging network used by banks for cross-border transactions, often criticized for slow settlement (days) and high fees (5-7%).

[39] thermodynamic security — The security model of proof-of-work blockchains, where tampering requires an energy expenditure proportional to the network's hashrate, making attacks economically infeasible.

[40] unit of account — A standard monetary unit used to measure and compare value; Bitcoin's volatility impairs its function as a reliable unit of account.

[41] volatility — The degree of variation in an asset's price over time; Bitcoin's high volatility is a major obstacle to its use as a stable medium of exchange or unit of account.

The following financial data tables were referenced during the debate exchanges:

| Asset | Annualized Volatility |

|---|---|

| Bitcoin | 54.0% |

| Gold | 15.1% |

| Global Equities | 10.5% |

Legend: Annualized standard deviation of trailing 1-year daily returns (as of early 2025). Bitcoin is roughly 3.6x more volatile than gold and 5.1x more volatile than global equities—far beyond what a stable monetary base requires. Units: percent (%).

</FinancialData>

| Metric | Mid-2023 Peak | August 2025 | Change |

|---|---|---|---|

| Public Capacity (BTC) | 5,400 | 4,200 | -22.2% |

| Active Channels | 80,000+ | 41,724 | -47.8% |

Legend: Lightning Network public capacity and channel count, peak vs. August 2025. Both core infrastructure metrics declined sharply, with routing channels nearly halving. Units: BTC and channel count; change in percent.

</FinancialData>

| Dimension | Current State | Structural Capability | Gap Status |

|---|---|---|---|

| Settlement Finality | Proven on-chain | Superior to traditional | ✅ Resolved |

| Monetary Policy | Code-enforced | Superior to discretionary | ✅ Resolved |

| Micropayments | Lightning operational | Sub-cent fees achieved | ✅ Resolved |

| Legal Recognition | Varies by jurisdiction | Growing (ETFs, El Salvador) | ⚠️ Transitional |

| Merchant Adoption | Millions globally | Accelerating | ⚠️ Transitional |

| Fiat Independence | Possible but uncommon | Demonstrated feasible | ⚠️ Transitional |

Legend: Assessment of Bitcoin's financial system replacement capability across key dimensions. Current State reflects present functionality; Structural Capability reflects inherent design potential. Gap Status indicates whether the dimension is resolved, transitional, or unresolved.

</FinancialData>

| Period (2025–26) | Low | High | Peak-to-Trough Swing |

|---|---|---|---|

| Dec 2025 – Jan 2026 | $84,400 | $97,963 | +16.1% |

| Single-day moves | — | — | ±4.6% |

Legend: Bitcoin daily price range over the trailing six months to mid-2026. Even in a "mature" market with spot ETFs live, swings of 16% over weeks and ~4.6% in a single session persist—far beyond any usable monetary base. Units: USD; swing in percent.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.