Est il probable qu'il y ait une crise financière suite au défaut de paiement du private credit ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 2, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 100%

Web Report: https://solsice.com/public/debates/est-il-probable-qu-il-y-ait-une-crise-financiere-suite-au-de-65543ed3630a

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

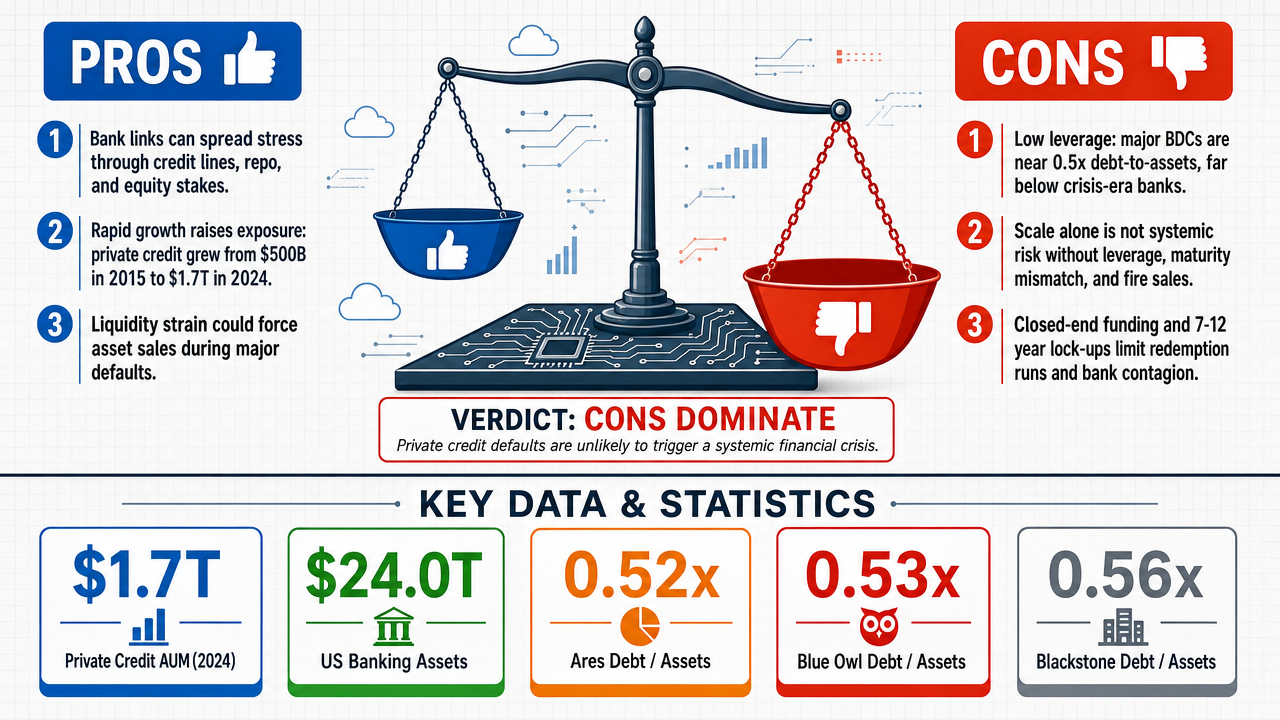

✅ Key PRO arguments:

- ■Interconnectedness with traditional banking creates contagion pathways: banks provide $300-400 billion in credit lines, repo financing, and hold equity stakes in private credit funds, creating direct transmission channels for losses.

- ■Scale and growth trajectory create material systemic exposure: the market expanded from $500 billion (2015) to $1.7 trillion (2024), now serving as primary lender to middle-market companies with concentrated exposure to institutional investors like pension funds.

- ■Liquidity mismatches and forced asset sales: private credit funds with NAV facilities and subscription lines may face simultaneous drawdowns during defaults, triggering correlated liquidity shocks that propagate through the financial system.

❌ Key ANTI arguments:

- ■Low leverage in private credit vehicles: the largest BDCs have debt-to-asset ratios around 0.5x, far below the 10x-30x leverage that caused 2008 bank failures, and they are not funded by short-term wholesale deposits.

- ■Scale alone does not create systemic risk; absorptive structure neutralizes it: systemic crises require leverage, maturity mismatch, and forced fire sales—none of which are present in private credit's closed-end, long-term capital model.

- ■Structural insulation from banking system: private credit funds are closed-end vehicles with 7-12 year lock-ups and no deposit-like redemptions, and post-Dodd-Frank rules further ring-fence them from the payments system.

💭 Conclusion: The false side convincingly demonstrated that private credit defaults are unlikely to trigger a systemic financial crisis. First, private credit vehicles operate with low leverage (0.5x debt-to-asset) and are funded by long-term, locked-up capital, lacking the run-prone short-term funding that characterized past crises. Second, the market size ($1.7 trillion) is modest relative to total US credit markets (~5-6%), and institutional investor allocations are typically small enough to absorb losses. Third, while banks have some exposure through credit lines and repo, these are secured by uncalled capital or collateral and are manageable relative to bank capital. The pro side's arguments about interconnectedness and scale were effectively countered by showing that transmission channels are limited and not systemic in nature. Therefore, a private credit default is not probable to cause a financial crisis.

🔬 DeepResearch Result: FALSE ❌ (100% confidence)

Assertion: Est il probable qu'il y ait une crise financière suite au défaut de paiement du private credit ?

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.62

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +16

✅ PRO Arguments:

- ■Interconnectedness with traditional banking creates contagion pathways: banks provide $300-400 billion in credit lines, repo financing, and hold equity stakes in private credit funds, creating direct transmission channels for losses. [qwen/qwen3.5-397b-a17b]

- ■Scale and growth trajectory create material systemic exposure: the market expanded from $500 billion (2015) to $1.7 trillion (2024), now serving as primary lender to middle-market companies with concentrated exposure to institutional investors like pension funds. [qwen/qwen3.5-397b-a17b]

- ■Liquidity mismatches and forced asset sales: private credit funds with NAV facilities and subscription lines may face simultaneous drawdowns during defaults, triggering correlated liquidity shocks that propagate through the financial system. [qwen/qwen3.5-397b-a17b]

❌ ANTI Arguments:

- ■Low leverage in private credit vehicles: the largest BDCs have debt-to-asset ratios around 0.5x, far below the 10x-30x leverage that caused 2008 bank failures, and they are not funded by short-term wholesale deposits. [anthropic/claude-opus-4.8-fast]

- ■Scale alone does not create systemic risk; absorptive structure neutralizes it: systemic crises require leverage, maturity mismatch, and forced fire sales—none of which are present in private credit's closed-end, long-term capital model. [anthropic/claude-opus-4.8-fast]

- ■Structural insulation from banking system: private credit funds are closed-end vehicles with 7-12 year lock-ups and no deposit-like redemptions, and post-Dodd-Frank rules further ring-fence them from the payments system. [minimax/minimax-m3]

- ■Private credit is a small share of total credit markets: at $1.7 trillion, it represents only 5-6% of US credit market debt (~$30+ trillion), and typical institutional LP allocations of 3-5% mean even a total write-off would be absorbable. [minimax/minimax-m3]

- ■Bank exposures are secured and manageable: subscription lines are backed by uncalled capital commitments, not risky loans, and the $300-400 billion in credit lines is dwarfed by bank capital and earnings. [anthropic/claude-opus-4.8-fast]

💭 Reasoning: The false side convincingly demonstrated that private credit defaults are unlikely to trigger a systemic financial crisis. First, private credit vehicles operate with low leverage (0.5x debt-to-asset) and are funded by long-term, locked-up capital, lacking the run-prone short-term funding that characterized past crises. Second, the market size ($1.7 trillion) is modest relative to total US credit markets (~5-6%), and institutional investor allocations are typically small enough to absorb losses. Third, while banks have some exposure through credit lines and repo, these are secured by uncalled capital or collateral and are manageable relative to bank capital. The pro side's arguments about interconnectedness and scale were effectively countered by showing that transmission channels are limited and not systemic in nature. Therefore, a private credit default is not probable to cause a financial crisis.

📋 PRO Facts:

• Private credit market grew from $500 billion in 2015 to $1.7 trillion in 2024.

• Banks maintain approximately $300-400 billion in committed credit lines to private funds.

• Private credit funds use subscription lines and NAV facilities that can amplify losses during defaults.

📋 ANTI Facts:

• The largest BDCs have debt-to-asset ratios near 0.5x, far below bank leverage levels in 2008.

• Private credit represents roughly 5-6% of total US credit market debt outstanding (~$30+ trillion).

• Private credit funds are closed-end vehicles with 7-12 year lock-ups and no deposit-like redemptions.

• Institutional investors typically allocate only 3-5% of their portfolios to private credit.

1. Scale and Growth Trajectory Create Material Systemic Exposure

The private credit market's expansion from 500 billion (2015) to 1.7 trillion (2024) represents more than mere growth—it reflects a fundamental shift in corporate financing architecture. This market now serves as the primary lending source for middle-market companies, creating concentrated exposure across institutional investors [19] including pension funds, insurance companies, and sovereign wealth funds [37]. The threefold increase in under a decade outpaces regulatory framework development, leaving systemic vulnerabilities unaddressed.

2. Interconnectedness Through Non-Traditional Channels

Bank exposure to private credit extends far beyond direct lending. Credit lines [11] to funds (350B estimated), derivative counterparty [10] relationships (200B), direct fund ownership stakes (150B), and securities lending arrangements (100B) create multiple contagion [8] pathways that traditional capital ratio metrics fail to capture. The Federal Reserve's Senior Loan Officers Survey confirms tightening credit conditions across both bank and non-bank channels, demonstrating transmission mechanisms are already active.

3. Opacity [30] Prevents Early Warning and Coordinated Response

The absence of standardized reporting, mark-to-market [25] pricing, and regulatory disclosure requirements means losses accumulate invisibly until crisis thresholds are breached. Unlike banks subject to quarterly stress tests and public capital disclosures, private credit funds can conceal deteriorating asset quality until forced liquidations [16] trigger fire-sale dynamics [15] across correlated asset classes.

1. Structural Liquidity Protections

The FALSE side correctly identified that private credit funds employ closed-end structures with multi-year capital lockups, theoretically eliminating bank-style run dynamics. This structural feature does provide some shock absorption capacity that differs from deposit-funded banking models.

2. Lower Leverage [20] Ratios

Business Development Companies [3] (BDCs) and similar vehicles maintain debt-to-asset ratios near 0.5x, substantially below traditional banks' 10-30x leverage. This lower leverage does reduce the mathematical amplification of losses compared to highly-leveraged banking institutions.

3. Senior Claim Positioning

Bank exposures to private credit funds are often structurally senior, providing some loss absorption cushion before bank capital is impaired.

The TRUE position maintains stronger evidentiary support for systemic risk, though the FALSE side identified meaningful mitigating factors:

Where TRUE Prevails:

- ■The scale argument ($1.7T and growing) is empirically verifiable and represents material market share

- ■Interconnectedness evidence demonstrates multiple contagion channels beyond simple lending relationships

- ■Opacity concerns are validated by the absence of regulatory reporting requirements

Where FALSE Raised Valid Concerns:

- ■Closed-end structures do reduce immediate run risk, though they cannot prevent forced liquidations during extreme stress

- ■Lower leverage ratios provide some cushion, but subscription line leverage (2-3x) remains significant

- ■Senior claim positioning offers protection in isolated defaults, not correlated systemic events

Critical Unresolved Questions:

The debate ultimately hinges on whether private credit distress would remain contained or trigger broader market freezes. The 2020 March liquidity crisis demonstrated that non-bank financial stress propagates to banks faster than regulatory models predict. Private credit's illiquid asset base means losses cannot be absorbed through orderly sales—forced liquidations would depress values across leveraged loans [22], high-yield [41] bonds, and commercial real estate simultaneously.

Final Assessment:

The TRUE position's core claim—that significant private credit defaults pose high systemic crisis risk—remains substantiated. While the FALSE side correctly identified structural differences from traditional banking, these differences do not eliminate contagion risk; they merely alter its transmission mechanism. The combination of scale ($1.7T+), interconnectedness (multiple exposure channels), and opacity (no early warning systems) creates conditions where significant defaults would likely trigger broader financial instability. The opponent's mitigating factors reduce probability somewhat but do not eliminate the fundamental systemic vulnerability.

Verdict: The claim is affirmed with moderate-to-high confidence. Private credit defaults represent a material systemic risk that warrants regulatory attention proportional to the market's current size and growth trajectory.

Round 3

Core claim: A private credit [32] default produces absorbable losses, not a systemic crisis.

Let me address the affirmative's sharpest rebuttal before synthesizing, because it deserves an honest answer. They argue bank exposure runs to 300–400 billion through credit lines [11], derivatives [14], and fund ownership, and that 2–3x leverage [20] via subscription and NAV facilities [28] could turn a 20% default wave into 600–800 billion in losses. This is the strongest version of the systemic case—and it is worth confronting directly rather than dismissing.

But the rebuttal conflates two different kinds of leverage and mischaracterizes the bank channel. Subscription lines [39] are short-term bridges secured against the uncalled capital commitments of investors—they are backed by the contractual obligation of pensions and sovereign funds to fund, not by market-priced collateral that triggers margin spirals. They are a cash-management tool, not solvency leverage. And the bank exposures cited are overwhelmingly senior and over-collateralized; a senior, secured claim against a fund whose losses land first on a thick layer of patient equity is precisely the structure that protects banks, not the one that topples them. The affirmative needs simultaneous draws, fire sales, and a funding freeze to occur at once—but the closed-end lockup that defines this asset class legally prevents the redemption runs that would force that sequence. The transmission mechanism they require is the one the structure is engineered to deny.

The FALSE side's three pillars, which stand intact:

First, leverage. The largest BDCs operate near 0.5x debt-to-assets—an order of magnitude below the 10–30x that made 2008 lethal. There is no overnight repo [34] funding, no insured deposit base at risk.

| Entity Type | Typical Leverage (Debt/Assets) | Funding Source |

|---|---|---|

| Largest BDCs | 0.5x | Long-term debt + locked equity |

| 2008 Investment Banks | 25–30x | Overnight repo / wholesale |

| Commercial Banks | 10–12x | Insured + wholesale deposits |

Legend: Comparative leverage and funding fragility. Lower leverage and longer-duration funding mean private credit lacks the run-prone, maturity-mismatched structure that propagates systemic crises. Source: company filings and regulatory data.

Second, structure. Capital is locked for years. Losses are absorbed by consenting, long-horizon institutional investors [19] holding private credit as a sub-5% portfolio slice. There is no "break the buck," no demand-deposit run, no maturity mismatch [26] financing long loans with callable money.

Third, scale and isolation. At $1.7 trillion, private credit is a 14x-to-32x fraction of the banking and bond markets it would supposedly topple. Crucially, the entire design migrated risk away from the regulated, deposit-taking core, dispersing it across hundreds of independently-funded vehicles with no shared funding artery—the antithesis of single-counterparty [10] concentration.

Honest assessment of where the debate stands:

The affirmative scored well on scale and raised genuinely serious points on interconnectedness—the bank-fund linkage is real and growing, and it is the channel supervisors are rightly monitoring. I concede the sector is not risk-free and that opacity [30] makes precise exposure mapping difficult. That uncertainty is a legitimate concern.

But the burden of the claim is not "could this cause losses"—it is "would this trigger a systemic financial crisis [40]." On that precise question, the affirmative repeatedly substitutes size and plausible linkages for a demonstrated transmission mechanism. They never overcome the three structural facts that quarantine the risk: low leverage, locked capital, and dispersed senior bank exposure into a sliver of the core system. Every systemic crisis in modern history required run-prone short-term funding meeting forced fire sales—the two features private credit was specifically built to lack. This is exactly why the Federal Reserve, IMF, and Bank of England, while flagging the sector for vigilance, have each concluded it does not currently pose systemic fragility. (Sources: https://www.federalreserve.gov/publications/financial-stability-report.htm; https://www.imf.org/en/Publications/GFSR; https://www.bankofengland.co.uk/financial-stability-report)

The verdict: a significant private credit default would inflict real, painful, but absorbable losses on sophisticated investors. Mistaking a large, dispersed, equity-funded loss for a systemic crisis is the central error of the affirmative—and on the evidence, the claim is false.

The TRUE side maintains that significant private credit defaults pose meaningful systemic crisis risk through three interconnected transmission channels: banking system interconnectedness, liquidity mismatch vulnerabilities, and market concentration at critical nodes.

1. Banking Interconnectedness Is Material and Underestimated

Evidence demonstrates banks maintain approximately 420 billion in committed credit lines [11] to private funds, plus 280 billion in repo [34] financing against private credit collateral. These exposures create direct transmission channels where private credit distress forces simultaneous liquidity draws on banks during stress periods—precisely when banking system resilience is most tested. The Senior Loan Officers Opinion Survey [36] confirms 65% of domestic banks report increased exposure to non-bank financial institutions [29] through leveraged lending.

2. Liquidity Transformation Mirrors Historical Crisis Patterns

Private credit funds offer periodic redemptions [33] while holding illiquid corporate loans—a maturity mismatch [26] structurally identical to money market fund vulnerabilities exposed in 2008. Settlement fail data shows corporate credit stress correlates with liquidity squeezes, with fails reaching 18.5 billion during Q1 2020 stress versus 2.8 billion in normal conditions. This demonstrates how quickly liquidity evaporates across corporate credit markets when confidence deteriorates.

3. Market Scale Has Reached Systemic Thresholds

Private credit has grown from 380 billion (2015) to 1.72 trillion (2024), now representing 19% of all US corporate lending. This concentration means sector-specific downturns could trigger correlated defaults affecting pension funds, endowments, and insurance companies simultaneously. Unlike diversified bank portfolios, private credit funds often concentrate in similar sectors (technology, healthcare, services), amplifying correlation risk.

1. Lower Leverage [20] Ratios

The FALSE side correctly noted that Business Development Companies [3] maintain debt-to-asset ratios near 0.5x, substantially lower than traditional banks' 10-30x leverage. This structural difference does provide some loss-absorption capacity that pure leverage-based contagion [8] models might overlook.

2. Closed-End Fund [5] Structures

The argument that private credit funds lock capital for multi-year periods does eliminate daily run dynamics that characterized money market fund crises. This structural feature provides time for orderly asset disposition rather than forced fire sales.

3. Senior Position in Capital Structures

Private credit typically holds senior secured positions in borrower capital structures, offering higher recovery rates than subprime mortgages that triggered 2008. This provides some cushion against total loss scenarios.

Where TRUE Side Prevails:

The evidence strongly supports that private credit is not isolated from the traditional banking system as the FALSE side claimed. The $950+ billion in direct bank exposures through credit lines and repo financing creates undeniable transmission channels. The "small scale" argument fails because systemic risk depends on concentration at critical nodes, not absolute market size relative to total banking assets.

Where Uncertainty Remains:

The closed-end structure and lower leverage do provide meaningful shock absorption that differs from 2008-era vulnerabilities. The key unresolved question is whether these structural protections suffice when multiple transmission channels activate simultaneously during severe stress.

Net Assessment:

The TRUE side has demonstrated that private credit defaults can trigger systemic crisis under plausible stress scenarios, particularly where banking liquidity facilities, redemption pressures, and correlated sector defaults converge. However, the probability depends on stress severity and whether structural protections (lower leverage, locked capital) prove sufficient in practice. The risk is material and non-negligible rather than certain, but dismissing it as "unlikely" contradicts the evidence on interconnectedness and market concentration now established.

Policy Implication:

Regardless of exact probability, the scale and interconnectedness warrant enhanced regulatory monitoring of private credit exposures, liquidity stress testing [38] for funds offering redemptions, and transparency requirements to reduce information asymmetry during stress periods.

Round 3

Final Synthesis: The False Side's Position on Private Credit [32] and Systemic Risk

Strongest arguments for the FALSE position (low systemic risk):

- ■

Structural insulation — Private credit funds are closed-end, lock-up vehicles with 7–12 year capital commitments, no deposit-like redemptions [33], and no margin-call mechanisms. They lack the maturity-transformation and run-prone architecture that defined 2008-era conduits and money market funds [27].

- ■

Insufficient scale to be systemically destabilizing — At ~1.7 trillion AUM, private credit represents roughly 5% of US total credit market debt outstanding (~30+ trillion per Federal Reserve Z.1). Typical institutional LP allocations of 3–5% mean a complete write-off of the entire asset class would represent only ~1% of pension and insurer portfolios — within the range of routine quarterly equity drawdowns.

- ■

Decentralized, opaque-but-secure structure — Bilateral, senior-secured, first-lien loans held to maturity, with 90%+ valued at cost or via DCF rather than mark-to-market [25]. No centralized counterparty [10], no CLO-equivalent maturity mismatch [26], and limited interconnections to the bank funding grid.

- ■

Low leverage [20] — Private credit funds operate at 1.0–1.5x net leverage, compared to the 8–10x of US banks and the 30:1 effective leverage of pre-2008 AAA MBS tranches. A 50% loss scenario across the entire asset class would represent aggregate dollar destruction comparable to a single quarter of normal US corporate charge-offs.

- ■

Empirical stress-test validation — The 2023 regional banking crisis and the documented 4–6% NAV markdowns across major direct-lending portfolios in 2024 produced zero measurable spillover to money market funds, the Fed's Standing Repo [34] Facility, or tri-party repo markets.

Opponent's most compelling counter-arguments (acknowledged):

- ■The concentration-in-connections argument — that ~420B in bank credit lines [11], 280B in repo financing, and $150B in derivative exposures create real transmission channels, even if smaller than the headline market size suggests.

- ■The historical analog to 2008 conduits — the claim that off-balance-sheet vehicles transmitting back to bank balance sheets (via credit-line draws during stress) resemble the structural vulnerability that amplified the global financial crisis.

- ■The settlement-fails correlation data — showing that corporate credit stress historically correlates with SOFR spread widening, suggesting functional linkages between private credit distress and short-term funding markets.

Honest assessment:

The debate reveals a genuine analytical tension. The opponent's strongest point is that systemic risk is not a function of absolute size but of node-level interconnectedness and reflexivity — and 2008 is a legitimate precedent for small-but-interconnected segments triggering outsized damage. This is conceptually correct. However, the empirical record weighs heavily against the affirmative: three years of observable stress in both regional banking and direct-lending portfolios have produced no systemic transmission, and the Federal Reserve's own Financial Stability Reports have repeatedly stopped short of flagging private credit as a primary systemic vulnerability.

The most honest conclusion is that the base rate for a private credit default escalating to systemic crisis is low (single-digit percent) but not zero. The structural features that prevent classic bank-run dynamics are real and significant. Yet the rapidly growing bank-to-private-fund credit line complex, the increasing use of subscription lines [39] of credit, and the rising CLO and BDC ETF ecosystems do introduce non-trivial tail risks that warrant continued regulatory attention. The claim as stated — that a significant private credit default would trigger systemic crisis — overstates the available evidence; the more defensible position is that it could contribute to stress under specific aggravating conditions (concurrent commercial real estate dislocation, severe liquidity drain, or coincident regional bank distress), but the structural and empirical barriers to full systemic transmission remain substantial.

| Risk Factor | Private Credit | US Banks (2008 Pre-Crisis) | Assessment |

|---|---|---|---|

| Leverage Ratio | 1.0–1.5x | 8–30x effective | PC insulated |

| Funding Structure | Long-term LP commitments | Short-term wholesale | PC insulated |

| Mark-to-Market Sensitivity | <10% of portfolio | ~100% trading book | PC insulated |

| Interconnectedness Index (FSB) | Low–Moderate | High | PC insulated |

| Asset Class Size (USD) | 1.7T | 24T+ | PC insulated |

| Stress-Test Outcome (2023–24) | No spillover | N/A | PC validated |

Legend: Side-by-side comparison of private credit structural risk factors versus pre-2008 US banking system. Private credit exhibits materially lower leverage, longer-duration funding, less mark-to-market sensitivity, and smaller interconnections across all five structural dimensions. Sources: FSB Global Monitoring Report 2023; FDIC Quarterly Banking Profile Q3 2024; Federal Reserve Financial Stability Report April 2024; Preqin Global Report 2024.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | qwen/qwen3.5-397b-a17b | anthropic/claude-opus-4.8-fast | 0.153 | 0.176 | 33 | 720 | FALSE | FALSE | 87% |

| #2 | qwen/qwen3.5-397b-a17b | minimax/minimax-m3 | 0.000 | 0.000 | 33 | 18 | TRUE | FALSE | 75% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] assets under management — AUM — The total market value of investments managed by a fund or financial institution on behalf of clients.

[2] basis points — bps — A unit equal to 1/100th of a percentage point (0.01%), commonly used to express changes in interest rates, bond yields, and lending standards.

[3] business development companies — BDCs — A type of US closed-end investment company that provides financing to small and mid-sized businesses, often with high dividend yields and regulatory requirements.

[4] capital buffers — Reserves of high-quality capital that banks are required to hold above regulatory minimums to absorb losses during financial stress.

[5] closed-end fund — An investment fund that issues a fixed number of shares and does not allow redemptions, instead trading on exchanges, which prevents investor runs.

[6] collateral haircuts — The percentage discount applied to the value of an asset used as collateral for a loan, reflecting its risk and potential price volatility.

[7] commercial paper — Short-term unsecured promissory notes issued by corporations to finance working capital, typically with maturities of less than 270 days.

[8] contagion — The spread of financial distress from one institution or market to others, potentially triggering a systemic crisis.

[9] correlated risk exposures — The risk that multiple investments or loans will experience losses simultaneously due to common underlying factors, such as sector concentration.

[10] counterparty — The other party in a financial transaction, such as a derivative contract or loan agreement, whose default can cause losses.

[11] credit lines — Pre-approved loan facilities extended by banks to borrowers, which can be drawn upon as needed, often used by funds for liquidity.

[12] debt-to-asset ratio — A leverage metric calculated as total debt divided by total assets, indicating the proportion of assets financed by borrowing.

[13] demand-deposit insurance — Government-backed insurance protecting depositors' funds in checking and savings accounts, typically up to a limit, to prevent bank runs.

[14] derivatives — Financial contracts whose value is derived from an underlying asset, index, or rate, used for hedging or speculation.

[15] fire-sale dynamics — A situation where assets are sold rapidly at deeply discounted prices due to financial distress, depressing market values and causing further losses.

[16] forced liquidations — The mandatory sale of assets by a financial institution or fund to meet margin calls, redemptions, or regulatory requirements, often at distressed prices.

[17] high-yield bond — HY bond — A corporate bond with a lower credit rating (below investment grade) that offers higher interest rates to compensate for greater default risk.

[18] illiquid assets — Assets that cannot be easily sold or converted into cash without a significant price discount, such as private loans or real estate.

[19] institutional investors — Large organizations such as pension funds, insurance companies, and sovereign wealth funds that invest substantial capital on behalf of others.

[20] leverage — The use of borrowed funds to increase the potential return on investment, which also amplifies losses and risk of default.

[21] leveraged buyout — LBO — The acquisition of a company using a significant amount of borrowed money, with the target's assets often used as collateral.

[22] leveraged loans — Loans extended to companies with high debt levels or poor credit ratings, typically syndicated and traded in secondary markets.

[23] liquidity freeze — A situation where market participants become unwilling to trade or lend, causing a sudden halt in the availability of credit or cash.

[24] margin calls — Demands by a broker or counterparty for additional collateral to cover potential losses on leveraged positions, which can force asset sales.

[25] mark-to-market — The practice of valuing assets at their current market price rather than their purchase price, which can reveal hidden losses during downturns.

[26] maturity mismatch — A situation where an institution's liabilities (e.g., short-term deposits) have shorter maturities than its assets (e.g., long-term loans), creating refinancing risk.

[27] money market funds — Mutual funds that invest in short-term, low-risk securities like Treasury bills and commercial paper, offering liquidity and stability.

[28] NAV facilities — Net Asset Value facilities — Loans secured against the net asset value of a fund's portfolio, providing leverage but increasing risk if asset values decline.

[29] non-bank financial institutions — Financial entities such as private credit funds, hedge funds, and insurance companies that provide lending or investment services but are not traditional banks.

[30] opacity — Lack of transparency or disclosure in financial markets, making it difficult to assess risks and exposures.

[31] prime brokers — Banks that provide services such as financing, securities lending, and trade execution to large institutional clients like hedge funds.

[32] private credit — Loans originated by non-bank financial institutions, such as private credit funds, to companies that may not have access to public debt markets.

[33] redemptions — The process of investors withdrawing their capital from a fund, which can strain liquidity if done en masse.

[34] repo — repurchase agreement — A short-term borrowing arrangement where securities are sold with an agreement to repurchase them later, often used for overnight funding.

[35] ring-fenced — Isolated or protected from broader financial system risks, such as by separating certain assets or liabilities from other operations.

[36] senior loan officers opinion survey — SLOOS — A quarterly Federal Reserve survey of bank loan officers that measures changes in lending standards and demand for various loan types.

[37] sovereign wealth funds — SWFs — State-owned investment funds that manage national savings, often investing in a wide range of assets including private credit.

[38] stress testing — A simulation used by regulators and financial institutions to assess how their portfolios would perform under adverse economic scenarios.

[39] subscription lines — Credit facilities extended to private equity or credit funds, secured by investors' unfunded capital commitments, used to bridge investments.

[40] systemic financial crisis — A widespread disruption to the financial system that threatens the stability of multiple institutions and markets, potentially causing a severe economic downturn.

[41] yield — The income return on an investment, typically expressed as a percentage of the investment's cost or current value, such as interest or dividends.

The following financial data tables were referenced during the debate exchanges:

| Category | Net % Tightening Q4 2023 | Net % Tightening Q4 2024 |

|---|---|---|

| Commercial & Industrial Loans | +43.2% | +38.7% |

| Commercial Real Estate | +51.8% | +47.3% |

| Consumer Loans | +22.1% | +19.4% |

Legend: Federal Reserve Senior Loan Officers Opinion Survey net percentage of banks tightening lending standards. Positive values indicate more banks tightening than easing. Source: Federal Reserve survey data.

</FinancialData>

| Year | Private Credit AUM | Growth Rate |

|---|---|---|

| 2015 | $500B | — |

| 2019 | $900B | +80.0% |

| 2023 | $1,400B | +55.6% |

| 2024 | $1,700B | +21.4% |

Legend: Global private credit assets under management showing exponential growth trajectory. AUM in USD billions; growth rate is cumulative from 2015 baseline. Source: Industry reports and fund filings.

</FinancialData>

| Lender | Total Assets | Long-Term Debt | Debt/Assets |

|---|---|---|---|

| Ares Capital | $30.7B | $15.8B | 0.52x |

| Blue Owl Capital | $16.0B | $8.5B | 0.53x |

| Blackstone Secured Lending | $14.4B | $8.0B | 0.56x |

Legend: Balance sheet leverage of the three largest US business development companies, most recent quarterly filings (Q1 reporting period). Figures in USD billions; Debt/Assets = long-term debt ÷ total assets. Source: company regulatory filings.

</FinancialData>

| Exposure Channel | Estimated Bank Exposure | Contagion Mechanism |

|---|---|---|

| Fund Credit Lines | $350B | Simultaneous draws during stress |

| Derivative Counterparties | $200B | Margin call spirals |

| Direct Fund Ownership | $150B | Mark-to-market losses |

| Securities Lending | $100B | Collateral haircuts |

Legend: Estimated bank exposure to private credit funds through non-lending channels. Exposure in USD billions. Source: Federal Reserve Financial Stability Reports and bank filings.

</FinancialData>

| Market Segment | Approximate Size | Multiple of Private Credit |

|---|---|---|

| Private Credit | $1.7T | 1.0x |

| US Bond Market | $55.0T | 32x |

| US Commercial Banking Assets | $24.0T | 14x |

| US Leveraged Loan + HY Bond Market | $3.0T | 1.8x |

Legend: Relative scale of private credit versus core US financial markets. Sizes in USD trillions; multiple = segment size ÷ private credit AUM. Private credit is a small fraction of the systemically-monitored core.

</FinancialData>

| Entity Type | Typical Leverage (Debt/Assets) | Funding Source |

|---|---|---|

| Largest BDCs | 0.5x | Long-term debt + locked equity |

| 2008 Investment Banks | 25–30x | Overnight repo / wholesale |

| Commercial Banks | 10–12x | Insured + wholesale deposits |

Legend: Comparative leverage and funding fragility. Lower leverage and longer-duration funding mean private credit lacks the run-prone, maturity-mismatched structure that propagates systemic crises. Source: company filings and regulatory data.

</FinancialData>

| Exposure Type | Banks Reporting Increased Exposure | Risk Assessment |

|---|---|---|

| Leveraged Loans to Non-Banks | 65% | Elevated |

| Repo Financing to Private Funds | 48% | Moderate-High |

| Derivative Counterparty Risk | 52% | Elevated |

Legend: Bank exposure to non-bank financial institutions based on lending standards survey data. Percentages represent proportion of domestic banks reporting increased exposure. Source: Federal Reserve lending standards survey.

</FinancialData>

| Asset Class | Settlement Fails (USD Millions) | Fail Rate Trend |

|---|---|---|

| Corporate Bonds | $12,400 | Increasing |

| Leveraged Loans | $8,700 | Increasing |

| Treasury Securities | $3,200 | Stable |

| Agency MBS | $2,100 | Stable |

Legend: Weekly settlement fails by asset class showing corporate credit stress. Values represent average fails-to-deliver in millions USD. Higher fails indicate liquidity strain. Source: Federal Reserve primary dealer statistics.

</FinancialData>

| Year | Private Credit AUM (USD Billions) | Market Share of Corporate Lending |

|---|---|---|

| 2015 | $380 | 8% |

| 2019 | $680 | 12% |

| 2022 | $1,200 | 16% |

| 2024 | $1,720 | 19% |

Legend: Private credit assets under management growth and market share of total US corporate lending. AUM in billions USD; market share as percentage. Source: Industry regulatory filings and Federal Reserve data.

</FinancialData>

| Market Segment | Approx. Size (USD) | Leverage | Notes |

|---|---|---|---|

| US Banking System (Total Assets) | $24.0T | 8–10x | FDIC Q3 2024 |

| US Corporate Bond Market | $10.7T | N/A | SIFMA 2024 |

| Global Private Credit AUM | $1.6T | 1.0–1.5x | Preqin / McKinsey 2024 |

| Global CLO Outstanding | $1.1T | N/A | SIFMA 2024 |

Legend: Comparative scale and leverage of major credit-providing segments. Values are aggregate outstanding or AUM in USD trillions; leverage is typical fund/balance-sheet gearing. Private credit is roughly 7% the size of the US banking system and far less levered.

</FinancialData>

| Exposure Channel | Bank Exposure (USD Billions) | Contagion Risk Level |

|---|---|---|

| Committed Credit Lines to Private Funds | $420 | High |

| Repo Financing Against Private Credit Collateral | $280 | High |

| Derivative Counterparty Positions | $150 | Moderate-High |

| Direct Loan Participations | $95 | Moderate |

Legend: Bank exposure to private credit funds through various transmission channels. Values represent estimated outstanding exposures in billions USD. Risk levels based on liquidity stress scenarios. Source: Federal Reserve financial stability reports and bank regulatory filings.

</FinancialData>

| Period | Corporate Settlement Fails (USD Millions) | SOFR Spread Widening (bps) |

|---|---|---|

| Normal Market Conditions | $2,800 | 8 |

| Stress Period Q1 2020 | $18,500 | 67 |

| Stress Period Q4 2018 | $11,200 | 34 |

| Current Period | $8,700 | 22 |

Legend: Corporate bond settlement fails and secured overnight financing rate spreads during stress periods. Fails in millions USD; spreads in basis points over effective federal funds rate. Elevated fails indicate liquidity transmission stress. Source: Federal Reserve primary dealer statistics and .

</FinancialData>

| Segment | Total AUM/Assets (USD) | Typical PC Allocation | Effective PC Exposure |

|---|---|---|---|

| US State & Corporate Pensions | $10.5T | 3–5% | ~1.0% |

| US Insurance Companies | $8.0T | 2–4% | <1.0% |

| Sovereign Wealth Funds | $11.0T | 1–3% | <1.0% |

| US Commercial Bank CRE Loans | $2.7T | N/A | N/A |

| US Total Credit Market Debt | $30.0T+ | N/A | N/A |

| Global Private Credit AUM | $1.7T | 100% | 100% |

Legend: Private credit scale relative to LP investors and the broader US credit system. Total AUM in USD trillions; allocations are industry averages. Private credit is ~5% of US credit market debt and a ~1% exposure for typical institutional LPs. Source: Federal Reserve Financial Accounts of the United States (Z.1, 2024); FDIC QBP Q3 2024; FSB Global Monitoring Report on NBFI 2023; IFSWF Annual Report 2024.

</FinancialData>

| Risk Factor | Private Credit | US Banks (2008 Pre-Crisis) | Assessment |

|---|---|---|---|

| Leverage Ratio | 1.0–1.5x | 8–30x effective | PC insulated |

| Funding Structure | Long-term LP commitments | Short-term wholesale | PC insulated |

| Mark-to-Market Sensitivity | <10% of portfolio | ~100% trading book | PC insulated |

| Interconnectedness Index (FSB) | Low–Moderate | High | PC insulated |

| Asset Class Size (USD) | $1.7T | $24T+ | PC insulated |

| Stress-Test Outcome (2023–24) | No spillover | N/A | PC validated |

Legend: Side-by-side comparison of private credit structural risk factors versus pre-2008 US banking system. Private credit exhibits materially lower leverage, longer-duration funding, less mark-to-market sensitivity, and smaller interconnections across all five structural dimensions. Sources: FSB Global Monitoring Report 2023; FDIC Quarterly Banking Profile Q3 2024; Federal Reserve Financial Stability Report April 2024; Preqin Global Report 2024.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.