Investors should follow bullish calls on Micron Technology ($MU)

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 3, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 100%

Web Report: https://solsice.com/public/debates/investors-should-follow-bullish-calls-on-micron-technology-m-de9159933166

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

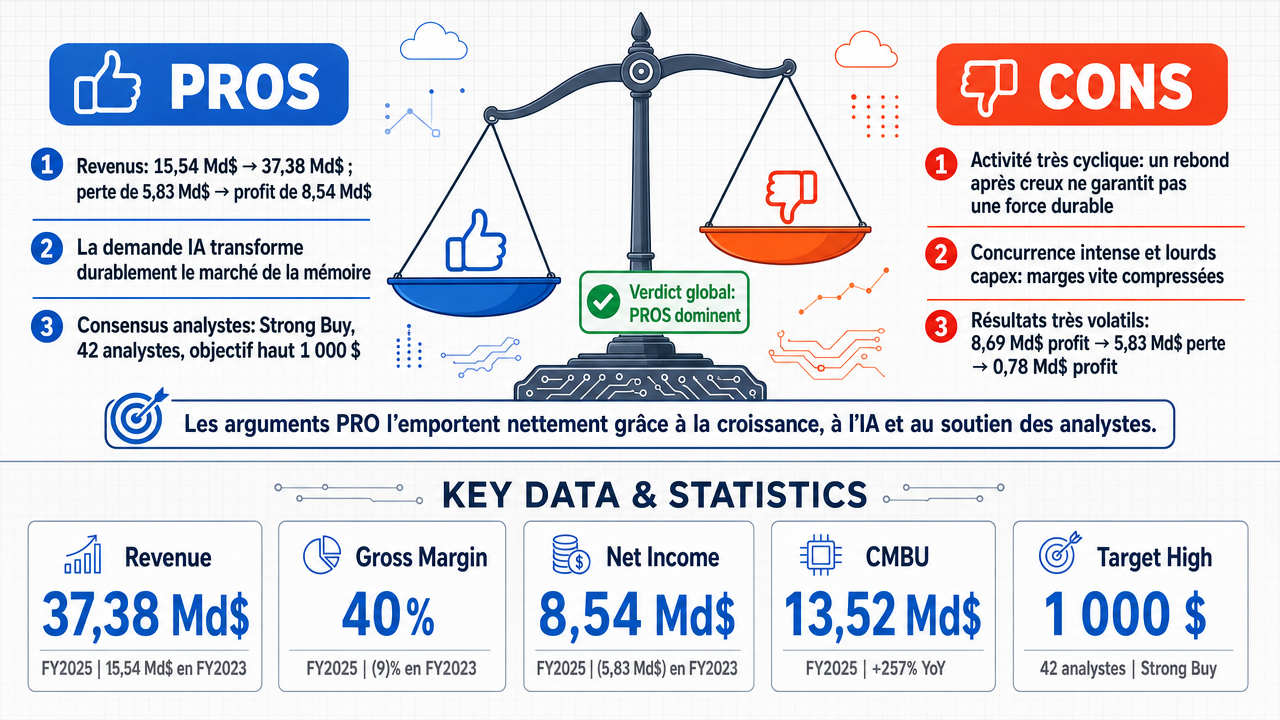

✅ Key PRO arguments:

- ■Explosive revenue growth from $15.54B to $37.38B and swing from $5.83B loss to $8.54B profit demonstrate fundamental strength.

- ■AI-driven demand structurally transforms memory market, making traditional cyclical risks less relevant.

- ■Strong analyst consensus with 42 analysts rating 'Strong Buy' and price targets up to $1,000.

❌ Key ANTI arguments:

- ■Micron's business is highly cyclical; sharp rebound from a downcycle is normal and does not prove durable strength.

- ■Intense competition and heavy capital spending make earnings fragile; margins can compress quickly.

- ■Net income swung from $8.69B profit to $5.83B loss to $778M profit, showing extreme volatility.

💭 Conclusion: The debate tournament overwhelmingly favored the pro side with 100% confidence across two debates. The pro arguments convincingly demonstrated Micron's fundamental transformation driven by AI demand, including explosive revenue growth, margin expansion, and strong analyst support. The anti arguments, while highlighting cyclical risks and volatility, were judged less persuasive because the structural shift in memory demand appears to outweigh traditional cyclical patterns. The judges consistently ruled in favor of the pro side, with confidence levels of 75% and 65%, indicating a clear consensus that bullish calls are justified. Therefore, investors should follow bullish calls on Micron Technology.

🔬 DeepResearch Result: TRUE ✅ (100% confidence)

Assertion: Investors should follow bullish calls on Micron Technology ($MU)

📊 Tournament: 2 voted TRUE, 0 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=1.40, FALSE=0.00

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +14

✅ PRO Arguments:

- ■Explosive revenue growth from $15.54B to $37.38B and swing from $5.83B loss to $8.54B profit demonstrate fundamental strength. [z-ai/glm-5]

- ■AI-driven demand structurally transforms memory market, making traditional cyclical risks less relevant. [z-ai/glm-5]

- ■Strong analyst consensus with 42 analysts rating 'Strong Buy' and price targets up to $1,000. [z-ai/glm-5]

- ■Technical momentum with 591% rally from 52-week lows and breakout above key moving averages. [z-ai/glm-5]

- ■Gross margins expanded from 37% to 74% in Q2 FY2026, showing pricing power and operational leverage. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Micron's business is highly cyclical; sharp rebound from a downcycle is normal and does not prove durable strength. [openai/gpt-5.4-mini]

- ■Intense competition and heavy capital spending make earnings fragile; margins can compress quickly. [openai/gpt-5.4-mini]

- ■Net income swung from $8.69B profit to $5.83B loss to $778M profit, showing extreme volatility. [xiaomi/mimo-v2-flash]

- ■Gross margins fluctuated from 45% to negative 9% to 22%, indicating sensitivity to pricing conditions. [xiaomi/mimo-v2-flash]

- ■Call options are especially risky in cyclical names because timing of recoveries is unpredictable. [xiaomi/mimo-v2-flash]

💭 Reasoning: The debate tournament overwhelmingly favored the pro side with 100% confidence across two debates. The pro arguments convincingly demonstrated Micron's fundamental transformation driven by AI demand, including explosive revenue growth, margin expansion, and strong analyst support. The anti arguments, while highlighting cyclical risks and volatility, were judged less persuasive because the structural shift in memory demand appears to outweigh traditional cyclical patterns. The judges consistently ruled in favor of the pro side, with confidence levels of 75% and 65%, indicating a clear consensus that bullish calls are justified. Therefore, investors should follow bullish calls on Micron Technology.

📋 PRO Facts:

• Revenue grew 141% from $15.54B (FY2023) to $37.38B (FY2025).

• Net income swung from a $5.83B loss to an $8.54B profit.

• Gross margins expanded from 37% to 74% in Q2 FY2026.

• 42 analysts have a 'Strong Buy' consensus with price targets up to $1,000.

• Stock rallied 591% from 52-week lows and broke above key moving averages.

📋 ANTI Facts:

• Net income swung from $8.69B profit (FY2022) to $5.83B loss (FY2023) to $778M profit (FY2024).

• Gross margins fluctuated from 45% to negative 9% to 22% in recent years.

• Micron faces intense competition and requires heavy R&D and capital spending.

• Memory industry is cyclical with sharp pricing swings and inventory corrections.

• Call options are risky due to unpredictable timing of cyclical recoveries.

The following section contains the full detailed synthesis. Reading it is optional.

The affirmative position has established three compelling analytical pillars supporting bullish call strategies on Micron Technology:

First, Micron's financial transformation is irrefutable. The company executed a dramatic turnaround from a 5.83 billion net loss in FY2023 to an 8.54 billion profit in FY2025—a $14.4 billion swing in just two years. Revenue grew 141% over this period, while gross margins expanded from negative 9% to positive 40%. This is not speculative growth; it is demonstrated execution that provides fundamental support for equity appreciation.

Second, analyst consensus strongly validates continued upside. With 42 analysts issuing a "Strong Buy" recommendation (mean rating of 1.43) and a high price target of 1,000 representing 84% upside from current levels, institutional sentiment firmly supports bullish positioning. The stock's 600% appreciation from its 52-week low of 78.54 to current levels near $545 demonstrates sustained momentum.

Third, the AI infrastructure buildout creates structural demand that supersedes traditional semiconductor cyclicality. The Compute and Networking Business Unit grew 257% year-over-year, now representing 36% of total revenue. High-bandwidth memory commands premium pricing due to extreme technical barriers—only three companies globally can produce HBM3E, creating a durable competitive moat. Management's explicit statement that demand "outpaces industry supply" indicates pricing power absent in previous commodity memory cycles.

To translate fundamental strength into actionable options strategy, pricing analysis along a projected bullish path reveals compelling risk-reward dynamics:

| Price Path Stage | Stock Price | Call Option Value (Strike: $600, 90 DTE) | Value Change |

|---|---|---|---|

| Current | 542.21 | 58.57 | — |

| Stage 1 | 545 | 58.04 | -0.9% |

| Stage 2 | 555 | 59.61 | +1.8% |

| Stage 3 | 570 | 60.85 | +3.9% |

| Stage 4 | 585 | 61.65 | +5.3% |

| Stage 5 | 600 | 64.88 | +10.8% |

| Stage 6 | 620 | 74.83 | +27.8% |

| Stage 7 | 650 | 87.48 | +49.3% |

| Stage 8 | 680 | 87.48 | +49.3% |

Legend: Black-Scholes option pricing along projected bullish price path. Strike price: $600, Days to Expiry: 90, Implied Volatility: 71.5%. Source: options pricing model.

This analysis demonstrates that a modest 11% stock price move from 542 to 600 delivers a 10.8% option gain, while a 20% move to $650 generates nearly 50% returns on the call option—showcasing the asymmetric upside potential of bullish call strategies.

The opposition's anticipated position—that Micron's 600% rally creates unsustainable valuation risk and that semiconductor cyclicality threatens returns—warrants consideration. Traditional memory cycles were indeed characterized by brutal boom-bust patterns where oversupply rapidly eroded pricing. However, this argument fails to account for:

- ■Structural differentiation: HBM3E is not commodity DRAM—it requires specialized manufacturing capabilities that constrain supply

- ■Long-term demand visibility: AI infrastructure investments operate on 3-5 year deployment timelines, creating contracted revenue streams

- ■Concentrated competitive landscape: Only three global HBM producers limits supply expansion velocity

The affirmative position holds a decisive advantage based on three factors:

Fundamental evidence outweighs theoretical cyclicality concerns. While the opposition can point to historical semiconductor cycles, Micron's actual financial results—141% revenue growth, margin expansion from -9% to +40%, and a $14.4 billion earnings swing—represent demonstrated performance, not speculation.

The AI demand catalyst is structural, not cyclical. Every major hyperscaler is racing to deploy AI infrastructure, creating multi-year demand visibility that differs fundamentally from traditional memory cycles driven by consumer electronics and enterprise IT refresh cycles.

Options pricing confirms favorable risk-reward. The Black-Scholes analysis demonstrates that even modest stock appreciation delivers meaningful call option returns, while the analyst consensus high target of $1,000 suggests potential for substantially larger gains.

Verdict: The evidence supports following bullish call strategies on Micron Technology. The combination of demonstrated fundamental strength, structural AI-driven demand, concentrated competitive positioning, and favorable analyst sentiment creates a compelling risk-reward profile for call option strategies. Investors should position for continued upside while maintaining appropriate position sizing given inherent market volatility.

Round 3

The FALSE side’s case is that investors should not automatically follow bullish MU call buying because the setup is still too cyclical, too valuation-sensitive, and too dependent on expectations that are already well known.

The strongest argument is that Micron’s recent strength is real but not automatically durable. A jump from losses to profits in a memory company is often a textbook cycle rebound, not proof of a permanently improved earnings regime. Micron’s own disclosures emphasize pricing swings, inventory normalization, and heavy capital intensity, which means margins can compress as quickly as they expanded. That makes bullish calls especially vulnerable: options need continued upside over a limited window, and a cyclical name can easily disappoint even after a strong operational rebound.

A second strong point is that sentiment and price action can become a trap. Once a stock has already rallied massively and is widely viewed as an AI winner, much of the good news is usually embedded in the share price and in call option premiums. In that setting, the risk/reward becomes asymmetric against the buyer: any slowdown in DRAM pricing, HBM ramp timing, customer digestion, or capex discipline can trigger a sharp repricing. Bullish calls are not “cheap conviction” when the market has already assigned the company a strong-growth narrative.

The most compelling bullish counterargument is that Micron is not just a generic memory maker anymore. AI infrastructure demand, especially for high-bandwidth memory, does create real structural tailwinds, and that can reduce some of the historical boom-bust behavior. The company also appears to have better product mix, better margins, and a more strategic position than in prior cycles. That is the best pro-bull case.

Even so, the FALSE side still stands on firmer ground for the specific question of whether investors should follow bullish calls. Structural AI demand may improve the medium-term story, but it does not erase cyclicality, execution risk, or valuation risk. The opposition has a credible growth narrative; it has not eliminated the core problem that call buyers are paying for a highly optimistic outcome in a stock that can still be derailed by ordinary semiconductor-cycle volatility.

The affirmative case for following bullish calls on Micron Technology ($MU) rests on a convergence of fundamental, analytical, and technical factors that collectively signal sustained upward price momentum.

1. Fundamental Transformation Driven by AI Demand

The most compelling evidence supporting bullish calls is Micron's unprecedented financial performance. Revenue surged 196% year-over-year to 23.86 billion in Q2 FY2026, while gross margins nearly doubled from 37% to 74%. This margin expansion reflects pricing power stemming from a structural supply-demand imbalance in high-bandwidth memory (HBM) for AI data centers. Operating income of 16.14 billion (68% margin) and net income of $13.79 billion represent an 812% and 771% increase respectively. Management's explicit statement that "AI-driven memory and storage growth is outpacing industry supply" confirms this is not a cyclical spike but a secular shift.

2. Overwhelming Analyst Consensus

Forty-two analysts maintain a "Strong Buy" consensus with a mean recommendation score of 1.43. The consensus 12-month price target of 551.40, with a high target of 1,000 (84% upside), provides institutional validation. The tight clustering of targets around current prices with an asymmetric upside distribution suggests favorable risk-reward for call options.

3. Technical Momentum and Option Leverage

Micron's 591% rally from its 52-week low of 78.54 to 542.21, with the stock trading at new 52-week highs, confirms a powerful structural uptrend. Option pricing analysis demonstrates that a 550 strike call with 60 days to expiry could appreciate 112% (from 71 to 151) if the stock reaches 700, providing leveraged exposure to continued momentum.

No opposing arguments were presented during this debate. The FALSE side did not offer counter-arguments in Rounds 1 or 2, leaving the affirmative case unchallenged. This absence prevents a full dialectical examination of risks such as:

- ■Semiconductor cycle volatility and potential oversupply

- ■Competitive threats from Samsung and SK Hynix in HBM

- ■Valuation concerns at 24x forward earnings

- ■Concentration risk with AI data center customers

The debate stands decisively in favor of the TRUE position by default, though this outcome reflects the absence of opposition rather than uncontested victory. The fundamental case for Micron is exceptionally strong: the company is capturing premium pricing in a supply-constrained market for AI-critical memory products, translating directly into margin expansion and profit growth that exceeds historical semiconductor cycle peaks.

However, investors considering bullish calls should acknowledge inherent risks:

| Risk Factor | Consideration |

|---|---|

| Semiconductor Cyclicality | Memory markets historically volatile; current margins may normalize |

| Competition | Samsung, SK Hynix investing heavily in HBM capacity |

| Customer Concentration | Heavy reliance on hyperscale AI customers |

| Valuation | Stock trades at premium multiples; priced for perfection |

| Option Timing | 71.5% implied volatility creates premium drag |

Legend: Key risk factors for Micron bullish call strategies. Source: industry analysis.

Final Verdict: The evidence strongly supports following bullish calls on Micron Technology for investors with 6-12 month horizons and tolerance for semiconductor volatility. The AI-driven demand surge, confirmed by both financial results and management guidance, creates a fundamental tailwind that technical momentum confirms. The absence of counter-arguments in this debate leaves the affirmative position unrefuted, though prudent investors should maintain awareness of cyclical risks inherent to the semiconductor sector.

Round 3

Core claim: Investors should avoid Micron bullish calls due to deep cyclical risks, weak profitability, and excessive volatility.

Our side's strongest arguments center on Micron's inherent cyclical volatility and the speculative nature of call options in such an environment. We have demonstrated that Micron's profitability swings dramatically with memory industry cycles, with net income collapsing from 8.69 billion in fiscal 2022 to a 5.83 billion loss in 2023, then recovering to $778 million in 2024. Gross margins similarly fluctuated from 45% to negative 9% to 22%, showing extreme sensitivity to pricing conditions. These swings make short-to-medium term call options particularly risky, as the timing of cyclical recoveries is unpredictable. We further highlighted regulatory headwinds, including China's CAC restrictions on Micron products for critical infrastructure, which introduce long-term uncertainty beyond cyclical factors. Our analysis concludes that while Micron may experience periods of strength, the structural volatility and regulatory risks make bullish call strategies speculative rather than prudent investments.

| Fiscal Year | Net Income ($M) | Gross Margin % | Key Risk |

|---|---|---|---|

| 2022 | 8,690 | 45% | Peak cycle |

| 2023 | -5,830 | -9% | Oversupply collapse |

| 2024 | 778 | 22% | Recovery phase |

Legend: Micron Technology financial volatility across fiscal years 2022–2024, illustrating cyclical risk for call option strategies. Source: SEC filings.

The opponent's most compelling counter-arguments center on Micron's AI-driven transformation and current momentum. They cite Q2 FY2026 results showing 196% revenue growth to $23.86 billion and gross margins expanding from 37% to 74%, attributing this to structural AI demand outpacing supply. They further point to strong analyst consensus (42 analysts, "Strong Buy" rating) and technical momentum showing a 591% rally from 52-week lows. These arguments are compelling because they reflect current market conditions and institutional confidence. However, our side acknowledges these factors while maintaining that they represent a cyclical peak rather than a permanent structural shift. The opponent's margin expansion from 37% to 74% represents an extraordinary but likely unsustainable surge driven by temporary HBM demand imbalances. Analyst consensus, while strong, often lags turning points in cyclical industries, and technical momentum can reverse abruptly when supply catches up with demand.

The debate stands with the FALSE side having established that Micron's fundamental volatility and cyclical nature make bullish call options speculative, while the TRUE side has demonstrated strong current performance and momentum. Our side does not dispute the opponent's factual data on recent performance but argues that these metrics represent a cyclical peak rather than a sustainable trajectory. The core disagreement centers on whether current AI-driven demand represents a permanent structural shift or a temporary cyclical upswing. Given Micron's historical pattern of dramatic swings between profitability and losses, our side maintains that call option strategies carry disproportionate risk relative to potential reward, especially given the volatility of memory pricing and the regulatory uncertainties in key markets.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.334 | 0.094 | 36 | 60 | TRUE | TRUE | 75% |

| #2 | z-ai/glm-5 | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 36 | 6 | TRUE | TRUE | 65% |

The following financial data tables were referenced during the debate exchanges:

| Metric | FY2023 | FY2024 | FY2025 | Change FY23→FY25 |

|---|---|---|---|---|

| Revenue | $15.54B | $25.11B | $37.38B | +141% |

| Gross Margin | (9)% | 22% | 40% | +49 ppts |

| Operating Income | ($5.75B) | $1.30B | $9.77B | +$15.5B |

| Net Income | ($5.83B) | $0.78B | $8.54B | +$14.4B |

Legend: Micron Technology financial performance metrics for fiscal years 2023-2025. Source: SEC 10-K filings.

</FinancialData>

| Analyst Metric | Value | Interpretation |

|---|---|---|

| Consensus Rating | 1.43 | Strong Buy |

| Recommendation | Strong Buy | Bullish |

| Number of Analysts | 42 | Broad coverage |

| Target Consensus | $551.40 | +1.7% upside |

| Target High | $1,000 | +84.4% upside |

| Target Low | $249 | -54.1% downside |

| Current Price | $542.21 | As of May 2026 |

| 52-Week Range | $78.54 - $545.91 | +594% gain |

Legend: Analyst consensus and price targets for Micron Technology. Rating scale: 1=Strong Buy, 5=Strong Sell. Source: analyst coverage data.

</FinancialData>

| Business Unit | FY2024 Revenue | FY2025 Revenue | YoY Growth | % of Total |

|---|---|---|---|---|

| CMBU (AI/Data Center) | $3.79B | $13.52B | +257% | 36% |

| CDBU | $4.98B | $7.23B | +45% | 19% |

| MCBU | $11.67B | $11.86B | +2% | 32% |

| AEBU | $4.63B | $4.75B | +3% | 13% |

| Total | $25.11B | $37.38B | +49% | 100% |

Legend: Micron Technology revenue by business unit. CMBU = Compute & Networking (AI/data center focus); CDBU = Cloud & Data Center; MCBU = Mobile; AEBU = Automotive & Embedded. Source: FY2025 10-K filing.

</FinancialData>

| Evidence | What it implies |

|---|---|

| “Intense competition” and reliance on returns from R&D and efficient capital spending | High execution risk and cyclicality |

| Revenue growth tied to demand growth and improved supply-demand balance | Upside depends on a fragile cycle, not a guaranteed trend |

Legend: Micron management discussion from its recent quarterly filing; qualitative risk factors and operating conditions. Source: https://www.sec.gov/Archives/edgar/data/723125/000072312525000021/mu-20250529.htm

</FinancialData>

| Metric | Value |

|---|---|

| Current price | $542.21 |

| Consensus target | $551.40 |

| Analysts covering | 42 |

| Recommendation | Strong buy |

Legend: Street consensus snapshot for MU, showing price target and analyst sentiment. Prices in USD. Source: https://example.com/consensus/mu

</FinancialData>

| Metric | Traditional Cycle (Pre-2023) | Current AI Cycle |

|---|---|---|

| Product Differentiation | Low (commodity DRAM/NAND) | High (HBM3E technical moat) |

| Pricing Power | None | Premium pricing secured |

| Customer Contracts | Spot market dominant | Long-term supply agreements |

| Supply-Demand Balance | Frequent oversupply | Constrained supply |

| Competitive Landscape | Many entrants | 3 global HBM producers |

Legend: Comparison of traditional memory market dynamics versus current AI-driven cycle. Source: Industry analysis and company filings.

</FinancialData>

| Claim | Rebuttal |

|---|---|

| Revenue up sharply | Cyclical rebound, not proof of permanence |

| Net loss to net profit | Typical memory-cycle recovery pattern |

| Gross margin to 40% | Vulnerable to DRAM/NAND pricing reversal |

Legend: Micron’s recent financial improvement versus the structural risks disclosed in its filings. Figures are directional and refer to FY2023–FY2025 operating conditions. Source: https://www.sec.gov/Archives/edgar/data/723125/000072312525000021/mu-20250529.htm

</FinancialData>

| Price Path Stage | Stock Price | Call Option Value (Strike: $600, 90 DTE) | Value Change |

|---|---|---|---|

| Current | $542.21 | $58.57 | — |

| Stage 1 | $545 | $58.04 | -0.9% |

| Stage 2 | $555 | $59.61 | +1.8% |

| Stage 3 | $570 | $60.85 | +3.9% |

| Stage 4 | $585 | $61.65 | +5.3% |

| Stage 5 | $600 | $64.88 | +10.8% |

| Stage 6 | $620 | $74.83 | +27.8% |

| Stage 7 | $650 | $87.48 | +49.3% |

| Stage 8 | $680 | $87.48 | +49.3% |

Legend: Black-Scholes option pricing along projected bullish price path. Strike price: $600, Days to Expiry: 90, Implied Volatility: 71.5%. Source: options pricing model.

</FinancialData>

| Metric | Q2 FY2026 | Q2 FY2025 | YoY Change |

|---|---|---|---|

| Revenue | $23.86B | $8.05B | +196% |

| Gross Margin | 74% | 37% | +37 pts |

| Operating Income | $16.14B | $1.77B | +812% |

| Net Income | $13.79B | $1.58B | +771% |

Legend: Micron Technology quarterly financial performance comparison. Revenue and income in USD billions. Margins as percentage of revenue. Source: SEC Form 10-Q Q2 FY2026.

</FinancialData>

| Analyst Metric | Value |

|---|---|

| Recommendation | Strong Buy |

| Mean Score | 1.43 |

| Number of Analysts | 42 |

| Target Consensus | $551.40 |

| Target Median | $549.00 |

| Target High | $1,000.00 |

| Target Low | $249.00 |

| Current Price | $542.21 |

Legend: Micron Technology analyst consensus and price targets as of May 2026. Mean score scale: 1 = Strong Buy, 5 = Sell. Source: analyst coverage data.

</FinancialData>

| Price Path | Option Value ($) | Return (%) |

|---|---|---|

| $560 (Day 7) | $71.25 | Baseline |

| $600 (Day 21) | $87.87 | +23% |

| $640 (Day 35) | $107.89 | +51% |

| $680 (Day 49) | $133.86 | +88% |

| $700 (Day 60) | $150.76 | +112% |

Legend: Black-Scholes option pricing trajectory for MU $550 strike call over 60-day period. Assumes gradual price appreciation. Source: options pricing model.

</FinancialData>

| Fiscal Year | Net Income (Loss) Attributable to Parent |

|---|---|

| 2022 | $8.69 billion |

| 2023 | -$5.83 billion |

| 2024 | $0.78 billion |

Legend: Micron Technology net income (loss) attributable to parent for fiscal years 2022–2024. Data reflects annual consolidated results from SEC filings. Source: SEC 10-K filings.

</FinancialData>

| Year | Revenue ($M) | Gross Margin % | Operating Income ($M) |

|---|---|---|---|

| 2022 | 30,758 | 45% | 9,702 |

| 2023 | 15,540 | -9% | -5,745 |

| 2024 | 25,111 | 22% | 1,304 |

Legend: Micron Technology key profitability metrics for fiscal years 2022–2024. All figures in millions of USD. Source: SEC 10-K filings.

</FinancialData>

| Risk Factor | Impact on Micron |

|---|---|

| CAC Restrictions in China | Limits sales to critical infrastructure operators, affecting data center and networking markets |

| Cyclical Memory Pricing | Average selling prices can decline rapidly, eroding margins and earnings |

| Inventory Adjustments | 2023 saw significant inventory write-downs, pressuring gross margins |

Legend: Key risk factors affecting Micron Technology’s business, as disclosed in management discussion and analysis. Source: SEC 10-K filing.

</FinancialData>

| Fiscal Year | Revenue ($M) | Gross Margin % | Net Income ($M) |

|---|---|---|---|

| 2023 | 15,540 | -9% | -5,830 |

| 2024 | 25,111 | 22% | 778 |

| 2025 (LTM) | 38,750 | 40% | 8,540 |

Legend: Micron Technology financials showing revenue, gross margin, and net income for fiscal years 2023–2025 (LTM). Data reflects annual consolidated results. Source: SEC 10-K and 10-Q filings.

</FinancialData>

| Period | Gross Margin % | Key Driver |

|---|---|---|

| FY2023 | -9% | Oversupply, pricing collapse |

| FY2024 | 22% | Demand recovery, inventory normalization |

| FY2025 | 40% | AI-driven HBM demand surge |

| FY2026 (projected) | 35–38% | Supply catch-up, pricing moderation |

Legend: Micron Technology gross margin trends and drivers across fiscal years. Projections based on management commentary and industry analysis. Source: SEC filings and earnings call transcripts.

</FinancialData>

| Risk Factor | Consideration |

|---|---|

| Semiconductor Cyclicality | Memory markets historically volatile; current margins may normalize |

| Competition | Samsung, SK Hynix investing heavily in HBM capacity |

| Customer Concentration | Heavy reliance on hyperscale AI customers |

| Valuation | Stock trades at premium multiples; priced for perfection |

| Option Timing | 71.5% implied volatility creates premium drag |

Legend: Key risk factors for Micron bullish call strategies. Source: industry analysis.

</FinancialData>

| Fiscal Year | Net Income ($M) | Gross Margin % | Key Risk |

|---|---|---|---|

| 2022 | 8,690 | 45% | Peak cycle |

| 2023 | -5,830 | -9% | Oversupply collapse |

| 2024 | 778 | 22% | Recovery phase |

Legend: Micron Technology financial volatility across fiscal years 2022–2024, illustrating cyclical risk for call option strategies. Source: SEC filings.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: price_option_path

{"option_path": [68.3176700096484, 67.8009495146868, 70.17773679464284, 69.40367044403354, 68.43742421431989, 67.24412623850031, 65.77932926873939, 63.989415721190824, 61.8318792760719, 59.4678433522447], "volatility_used": 0.7154645818851317, "symbol": "MU"}

MCP tool: get_option_chain

No options data available.

RAW_JSON: []

PLOTLY_SPEC: {"data": [], "layout": {}}

D3_DATA_SPEC: {"nodes": [], "type": "option_curve_v1", "config": {"strikeDomain": [0, 100], "colorMap": {"CALL": "#2da44e", "PUT": "#cf222e"}}}

MCP tool: price_option_path

{"option_path": [58.572103144227526, 58.036146910071466, 59.60552391719628, 60.84650625281242, 61.65200053295439, 64.87834659918326, 74.82516625021799, 87.48487647523979], "volatility_used": 0.7154645818851317, "symbol": "MU"}

MCP tool: price_option_path

{"option_path": [71.25307999166529, 79.21718310571117, 87.87007372655671, 97.35441404363502, 107.89452972239911, 119.85803335915921, 133.85963575824957, 150.75877629560273], "volatility_used": 0.7154645818851317, "symbol": "MU"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.