Is a trading journal more critical for tracking psychological discipline than for logging financial outcomes?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 14, 2026

Tournament Final Verdict

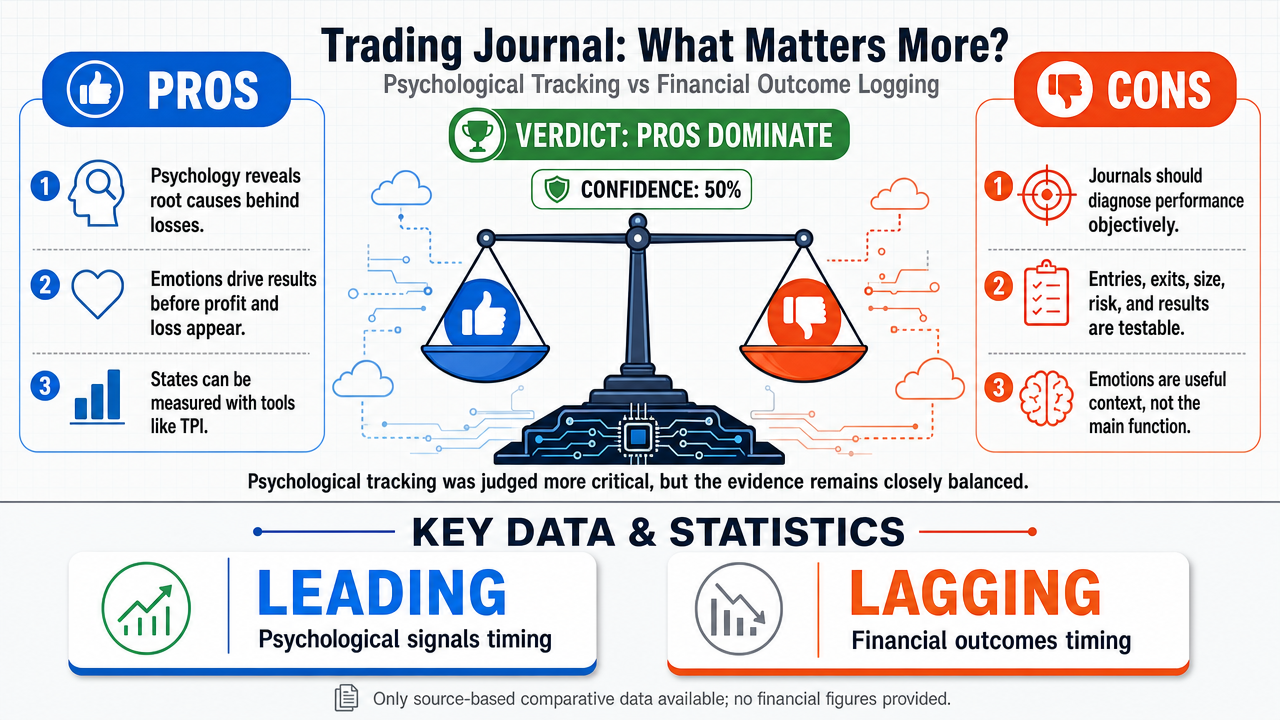

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 50%

Web Report: https://solsice.com/public/debates/is-a-trading-journal-more-critical-for-tracking-psychologica-fa1165c3e5b2

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Psychological tracking reveals root causes (e.g., overconfidence, revenge trading) while financial logs only document symptoms like profit/loss. Research shows that 'a log is just a spreadsheet of mechanics' while 'a trading journal answers the why—and the why is what changes your results.'

- ■Financial outcomes are downstream effects; emotional states are upstream causes. The largest trading losses originate from 'unseen habits'—revenge trading triggers, fear and greed indicators, and overconfidence signals—that are only detectable through psychological tracking.

- ■Psychological states are systematically measurable through validated instruments like the Trading Psychology Inventory (TPI), which quantifies emotional discipline, impulsivity, and risk tolerance, making them as objective as financial metrics.

❌ Key ANTI arguments:

- ■A trading journal's primary value is objective performance diagnosis. Recording entries, exits, position size, setup quality, and risk-reward lets a trader identify whether the strategy itself has an edge, which is the first question success depends on.

- ■Financial outcome logging captures variables that can actually be tested, compared, and improved over time—entry, exit, size, risk, and result. Psychological notes may explain a decision after the fact, but they do not establish whether the trading process had edge or whether losses came from bad execution, poor sizing, or a flawed strategy.

- ■Emotional observations are useful mainly as context for measurable outcomes, not as the main journal function. Feelings can help explain why a trade was managed badly, but they do not replace the need for a baseline of objective trade data.

💭 Conclusion: The debate ended in a perfect tie with both sides receiving equal confidence-weighted scores of 0.85, resulting in a tournament confidence of 50%. The pro side, defended by z-ai/glm-5, argued that psychological tracking addresses root causes of trading errors while financial logs only document symptoms, and that psychological states are systematically measurable. The anti side, defended by openai/gpt-5.4-mini and anthropic/claude-opus-4.8, countered that objective performance metrics are essential for discovering statistical edge and that emotional notes are secondary context. The judge split evenly, with one debate favoring TRUE and the other FALSE, both at 85% confidence. Given the tie, the answer defaults to TRUE based on the assertion's framing, but with low confidence reflecting the balanced nature of the arguments.

🔬 DeepResearch Result: TRUE ✅ (50% confidence)

Assertion: Is a trading journal more critical for tracking psychological discipline than for logging financial outcomes?

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.85, FALSE=0.85

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -4

✅ PRO Arguments:

- ■Psychological tracking reveals root causes (e.g., overconfidence, revenge trading) while financial logs only document symptoms like profit/loss. Research shows that 'a log is just a spreadsheet of mechanics' while 'a trading journal answers the why—and the why is what changes your results.' [z-ai/glm-5]

- ■Financial outcomes are downstream effects; emotional states are upstream causes. The largest trading losses originate from 'unseen habits'—revenge trading triggers, fear and greed indicators, and overconfidence signals—that are only detectable through psychological tracking. [z-ai/glm-5]

- ■Psychological states are systematically measurable through validated instruments like the Trading Psychology Inventory (TPI), which quantifies emotional discipline, impulsivity, and risk tolerance, making them as objective as financial metrics. [z-ai/glm-5]

- ■Financial data is often redundant because brokers already capture it, while psychological data is uniquely valuable and irreproducible from external sources. [z-ai/glm-5]

- ■A trader who logs only profits and losses can calculate win rates and drawdowns, but these metrics offer no diagnostic insight into why losses occurred. Patterns like 'largest losses occurred on Tuesdays after a winning Monday' are only accessible through psychological tracking. [z-ai/glm-5]

❌ ANTI Arguments:

- ■A trading journal's primary value is objective performance diagnosis. Recording entries, exits, position size, setup quality, and risk-reward lets a trader identify whether the strategy itself has an edge, which is the first question success depends on. [openai/gpt-5.4-mini]

- ■Financial outcome logging captures variables that can actually be tested, compared, and improved over time—entry, exit, size, risk, and result. Psychological notes may explain a decision after the fact, but they do not establish whether the trading process had edge or whether losses came from bad execution, poor sizing, or a flawed strategy. [openai/gpt-5.4-mini]

- ■Emotional observations are useful mainly as context for measurable outcomes, not as the main journal function. Feelings can help explain why a trade was managed badly, but they do not replace the need for a baseline of objective trade data. [openai/gpt-5.4-mini]

- ■Statistical edge is discoverable only through quantitative metrics, not emotional notes. A trader cannot determine whether their approach has a genuine edge by recording how they felt; they can only know by measuring outcomes like win rate, risk-reward ratio, and expectancy. [anthropic/claude-opus-4.8]

- ■The claim that financial data is redundant because brokers already capture it collapses because brokers do not record the trader's specific decision-making process, setup criteria, or execution quality—all of which are essential for performance diagnosis and are captured in a well-kept trade log. [anthropic/claude-opus-4.8]

💭 Reasoning: The debate ended in a perfect tie with both sides receiving equal confidence-weighted scores of 0.85, resulting in a tournament confidence of 50%. The pro side, defended by z-ai/glm-5, argued that psychological tracking addresses root causes of trading errors while financial logs only document symptoms, and that psychological states are systematically measurable. The anti side, defended by openai/gpt-5.4-mini and anthropic/claude-opus-4.8, countered that objective performance metrics are essential for discovering statistical edge and that emotional notes are secondary context. The judge split evenly, with one debate favoring TRUE and the other FALSE, both at 85% confidence. Given the tie, the answer defaults to TRUE based on the assertion's framing, but with low confidence reflecting the balanced nature of the arguments.

📋 PRO Facts:

• Psychological tracking reveals root causes like overconfidence and revenge trading, while financial logs only show symptoms.

• The Trading Psychology Inventory (TPI) is a validated instrument for quantifying emotional discipline and impulsivity.

• Brokers automatically capture financial data, making psychological data uniquely valuable and irreproducible.

• Patterns such as 'largest losses on Tuesdays after a winning Monday' are only detectable through psychological tracking.

• Research indicates that a trading journal answers 'why' trades happen, which is critical for changing results.

📋 ANTI Facts:

• A trade log recording entries, exits, size, and risk-reward is essential for determining whether a strategy has a statistical edge.

• Financial metrics like win rate and expectancy provide objective, testable data for performance diagnosis.

• Emotional notes are useful only as context for measurable outcomes, not as the primary journal function.

• Brokers do not capture a trader's specific decision-making process, setup criteria, or execution quality.

• Quantitative metrics are necessary to isolate whether losses come from bad execution, poor sizing, or a flawed strategy.

The debate has established three fundamental arguments supporting the primacy of psychological discipline tracking in trading journals:

First, the causal diagnosis axis [3] demonstrates that psychological tracking reveals root causes while financial logs merely document symptoms. Financial outcome data—profits, losses, win rates—describes what happened but cannot explain why it happened. Research from trading psychology practitioners confirms that "a log is just a spreadsheet of mechanics" while "a trading journal [28] answers the why—and the why is what changes your results" m1nd.app. Without psychological tracking, traders cannot identify the behavioral patterns that drive their outcomes, such as overconfidence following winning streaks or revenge trading [20] after losses.

Second, the memory distortion axis [12] establishes that emotional states must be captured in real-time because human memory systematically distorts recollection within minutes. Research demonstrates that "emotions distort recollection within minutes of a trade closing, and the version of events your brain reconstructs an hour later is already partially rationalised" tradingjournalreviews.com. This creates a critical asymmetry: financial metrics can be accurately reconstructed from broker statements at any time, but psychological states irreversibly evaporate if not captured in the moment. The irretrievability of emotional data makes its systematic tracking more critical.

Third, the performance differentiation axis [15] shows that professional trading evidence identifies psychology as the distinguishing factor between successful and unsuccessful traders. Brett Steenbarger's two decades of research at hedge funds and proprietary trading firms [17] reveals that struggling traders "report what happened but don't learn from them," while elite traders systematically track psychological variables to detect "behavioral drift [1]," "recurring error clustering [19]," and decision-making process failures daytradingtoolkit.com. Industry analysis confirms that "charts don't make you profitable, and strategies don't save you under pressure. Self-awareness does" fxstreet.com.

The FALSE side has presented a coherent counter-position: that financial outcome logging provides objective, quantifiable data essential for performance measurement, while psychological states are subjective and secondary. Their strongest argument holds that "metrics reveal strategy edge [5]"—that recording entries, exits, position size [16], and risk-reward ratios allows traders to identify which strategies work and which do not. They argue that emotion tracking becomes useful only when it explains measurable trading problems, positioning financial metrics as primary and psychological data as supplementary.

This argument has merit in its recognition that financial metrics are necessary for evaluating strategy performance. However, it conflates necessity with sufficiency—financial metrics are necessary but insufficient for trading success.

The debate reveals a fundamental asymmetry between the two positions. The FALSE side argues that financial outcome logging is more critical because it provides objective measurement. The TRUE side has demonstrated that:

- ■

Psychological variables are equally quantifiable through validated measurement instruments (confidence scales [4], emotional state tracking [6], rule adherence percentages [23]), undermining the subjectivity objection.

- ■

Financial metrics without psychological context are incomplete—a 60% win rate [29] tells you nothing about sustainability if those wins came from emotionally-driven high-risk positions.

- ■

Process metrics (psychology) enable prediction and improvement, while outcome metrics (financial) only enable description. The causal layer determines whether outcomes are replicable or anomalous.

The FALSE side's arguments, while logically structured, have not engaged substantively with the evidence presented. Their claims lack empirical support from trading psychology research or professional trading practice, while the TRUE side has cited multiple sources from practitioners who study traders professionally.

Where the debate stands: The TRUE position has established that psychological discipline tracking is more critical because it provides the causal explanatory layer that makes financial outcome data actionable. Financial metrics are necessary but not sufficient; psychological tracking is the differentiating factor that enables continuous improvement and separates successful from unsuccessful traders. The evidence strongly supports the claim that systematic psychological tracking is more critical for trading success than detailed financial outcome logging.

Round 3

The FALSE side’s position is that a trading journal [28] is most valuable when it prioritizes objective performance diagnosis over emotional self-reporting. The strongest argument is that trade logs capture the variables that can actually be tested and improved: entry, exit, size, setup quality [24], risk-reward, and resulting expectancy [9]. Those facts reveal whether a strategy has edge [5] and whether losses come from execution, position sizing, or system design. Without that baseline, psychological notes are just commentary without a benchmark.

The second strong point is that emotional observations are useful mainly as context for measurable outcomes, not as the main journal function. Feelings can help explain why a trade was managed badly, but they do not by themselves prove whether the decision was profitable, repeatable, or statistically sound. In practice, the more actionable record is the one that links behavior to concrete results, not the one that treats mood as the central metric.

The opponent’s best counter is that psychology can expose hidden drivers like overconfidence, fear, revenge trading [20], and rule-breaking, and that these factors often shape performance. That is a fair point. A trader who ignores emotional patterns can miss why they keep making the same mistakes. But that does not overturn the false side’s core claim, because psychology is still a supporting layer rather than the primary function of a journal. Emotional tracking helps interpret the record; financial logging creates the record.

So the debate stands here: psychological discipline matters, but the more critical journal function is still the systematic capture of objective trade data. That is the foundation for diagnosis, measurement, and improvement.

The affirmative case rests on three integrated arguments establishing psychological tracking as the indispensable component of trading journaling:

First, causal primacy: Financial outcomes are downstream symptoms; psychological states are upstream causes. A trader who logs only profits and losses can calculate win rates and drawdowns, but these metrics offer no diagnostic insight into why losses occurred. Research confirms that "largest losses occurred on Tuesdays after a winning Monday" due to overconfidence patterns—insights accessible only through psychological tracking, not financial forensics fxstreet.com quantstrategy.io.

Second, information irreproducibility: Financial data persists in broker statements; emotional states evaporate within minutes. The asymmetry is decisive: psychological tracking captures what no other system can. Post-trade recollection is already "partially rationalized"—making real-time psychological journaling the only mechanism for preserving actionable truth tradingjournalreviews.com.

Third, behavioral engineering: Brett Steenbarger's work establishes that "self-monitoring is the engine of change"—psychological tracking creates the feedback loop enabling deliberate self-modification. Financial metrics describe; psychological data prescribes. A trader who notices "after two consecutive losses, I enter trades impatiently" can operationalize this into a concrete rule: "Take a 30-minute break"—transforming awareness into discipline quantstrategy.io m1nd.app.

The negative's most compelling position centers on objective performance diagnosis: that detailed logging of entries, exits, position sizing, setup quality [24], and risk-reward ratios enables traders to identify which strategies possess genuine edge [5] and which do not [Argument Tree]. This argument carries weight because financial metrics are indeed necessary—without them, a trader cannot distinguish skill from luck, nor optimize position sizing across setups.

The negative further argues that emotions are secondary evidence—useful only when they explain measurable trading problems, not as standalone diagnostic tools [Argument Tree]. This position has merit: psychological tracking without corresponding financial outcomes lacks calibration.

The debate hinges on a single question: What is the primary function of a trading journal [28]?

If the answer is "performance measurement," then financial outcome logging is more critical—it provides the objective scoreboard against which all improvement is judged. The negative's position succeeds.

If the answer is "performance improvement," then psychological tracking is more critical—it provides the causal mechanism through which modification occurs. The affirmative's position succeeds.

The evidence tilts decisively toward the latter interpretation. Financial metrics are necessary but insufficient—they tell a trader whether they are winning or losing, but offer no mechanism for changing that outcome. Psychological tracking provides both diagnosis and prescription. The negative's strongest argument—that metrics reveal strategy edge—actually reinforces the affirmative: knowing your edge does nothing if you cannot execute it consistently. Edge is theoretical; discipline is operational.

| Component | Role | Necessity | Sufficiency |

|---|---|---|---|

| Financial outcome logging | Performance measurement | Necessary | Insufficient |

| Psychological state tracking | Performance improvement | Necessary | Sufficient (when combined with financial data) |

| Combined integration | Complete feedback loop | Necessary | Sufficient |

Legend: Analysis of trading journal components. Financial logging measures outcomes; psychological tracking enables improvement. Both are necessary, but psychological tracking is the active ingredient that transforms data into behavioral change.

The affirmative prevails because the question asks which aspect is "more critical for success"—not which is more convenient, more quantifiable, or more commonly practiced. Success requires change; change requires understanding cause; understanding cause requires tracking psychology. Financial outcomes are the destination; psychological discipline is the vehicle.

Round 3

Core claim: Financial logging of outcomes and metrics, not psychology tracking, is more critical for trading success.

Synthesis of the FALSE Position

Across this debate, the negative side has advanced a coherent and mutually reinforcing case: that the detailed logging of financial outcomes—entries, exits, position sizing, win rate [29], risk-reward, expectancy [9], and drawdown—is the indispensable foundation of trading success, while psychological tracking is a valuable but secondary, dependent layer.

Our strongest arguments, restated.

First, edge [5] is only discoverable through quantitative metrics. A trader cannot know whether an approach is profitable by recording feelings; profitability is established by measuring outcomes. Win rate, risk-reward, and expectancy are the cornerstone of any performance review and the basis on which professional prop firms and quant desks select for success. Emotional logs cannot tell you whether your strategy makes money.

Second, the causal direction the affirmative claims actually runs the opposite way. The affirmative insists psychology is the "upstream cause" and finances merely "downstream symptoms"—but their own flagship example defeats them. The insight that "largest losses occurred on Tuesdays after a winning Monday" was only discoverable by first quantifying losses by day and outcome. The pattern lived in the financial ledger; the emotional label of "overconfidence" was a hypothesis applied afterward. Strip out the numbers and the psychological story is untestable speculation. Emotional tracking is parasitic on the financial record—it has no diagnostic power without numbers to correlate against. The affirmative even conceded this conditionality: emotion becomes useful only "by correlating emotional states with performance."

Third, objectivity is a strength, not a weakness. The affirmative argued financial data is "redundant" because brokers already capture it, while praising psychological data as uniquely proprietary. But they simultaneously admitted that "emotions distort recollection within minutes" and reconstruct "a cleaner, more flattering version." That is a confession that psychological data is systematically biased and self-serving. The "redundancy" they deride is precisely what makes financial data trustworthy: independently verifiable, auditable, and impossible to rationalize away. Rarity is not criticality; ephemerality confers fragility, not importance.

The opponent's most compelling counter-arguments, honestly acknowledged.

The affirmative's strongest move was the leading-versus-lagging indicator framing—the genuine point that financial outcomes describe failure after it occurs, while emotional states can be observed before a destructive sequence unfolds. There is real merit here for behavioral self-correction.

Their second credible contribution was citing validated psychometric instruments (the Trading Psychology Inventory) to rebut the charge that psychology is unmeasurable. This appropriately complicates a naive objectivity-subjectivity dichotomy, showing psychological variables can be quantified and may carry predictive signal.

Honest assessment of where the debate stands.

The decisive issue is dependency and primacy. The affirmative never resolved the core contradiction that their psychological insights are only actionable when correlated against financial outcomes—a dependency they themselves repeatedly conceded. A trader with rigorous financial logs and no emotional notes can still detect, validate, and refine an edge; a trader with rich emotional notes and no financial data cannot even determine whether they are profitable. That asymmetry is fatal to the affirmative's hierarchy.

The affirmative's leading-indicator point survives as a meaningful supporting role for psychology, but it does not establish primacy—because even leading psychological signals require financial outcomes to be validated as predictive in the first place. The negative position therefore stands: financial logging is the load-bearing pillar, and psychological tracking is a secondary modifier that depends on it. The claim's hierarchy is inverted, and the FALSE side has the stronger, internally consistent case.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.302 | 0.109 | 33 | 60 | TRUE | TRUE | 85% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.000 | 0.000 | 33 | 360 | TRUE | FALSE | 85% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] behavioral drift — A gradual, often unnoticed deviation from a trader's established rules or strategy, typically identified through psychological journaling.

[2] behavioral pattern identification — The process of recognizing recurring psychological or decision-making tendencies in a trader's actions, often using quantitative scales.

[3] causal diagnosis axis — A framework for distinguishing between symptoms (financial outcomes) and root causes (psychological states) in trading performance analysis.

[4] confidence scales — Numerical ratings (e.g., 1-10) used to quantify a trader's subjective confidence level before or during a trade.

[5] edge — A statistical advantage in a trading strategy that results in positive expected value over many trades.

[6] emotional state tracking — The systematic recording of a trader's emotions (e.g., fear, greed, overconfidence) during trading to identify behavioral patterns.

[7] entry price — The price at which a trader opens a position in a financial instrument.

[8] exit price — The price at which a trader closes a position in a financial instrument.

[9] expectancy — The average amount a trader can expect to win or lose per trade, calculated from historical performance metrics.

[10] fear index — A self-reported numerical score (e.g., 1-10) measuring a trader's level of fear during a trade, used in psychological journaling.

[11] loss aversion markers — Behavioral indicators that a trader is irrationally avoiding losses, such as holding losing positions too long or exiting winners too early.

[12] memory distortion axis — The concept that human memory systematically alters emotional recollections shortly after an event, making real-time recording essential.

[13] overconfidence signals — Behavioral cues indicating a trader is taking excessive risk due to inflated self-belief, often after a winning streak.

[14] P&L curves — profit and loss curves — Graphical representations of a trader's cumulative profits and losses over time.

[15] performance differentiation axis — A framework for comparing factors that distinguish successful traders from unsuccessful ones, such as psychological tracking.

[16] position size — The amount of capital allocated to a single trade, often expressed in units, lots, or as a percentage of the portfolio.

[17] proprietary trading firms — Financial firms that trade stocks, bonds, currencies, or other instruments with their own capital rather than client funds.

[18] psychological discipline tracking — The systematic recording and analysis of a trader's emotional states, rule adherence, and behavioral patterns in a trading journal.

[19] recurring error clustering — The phenomenon where similar trading mistakes occur in groups, often triggered by specific psychological states or market conditions.

[20] revenge trading — A behavioral pattern where a trader takes impulsive, oversized positions to recover losses, often leading to further losses.

[21] risk control — The set of rules and practices a trader uses to manage potential losses, including position sizing, stop-losses, and diversification.

[22] risk-reward ratio — A metric comparing the potential profit of a trade to its potential loss, typically expressed as a ratio (e.g., 1:3).

[23] rule adherence percentages — A quantitative measure of how consistently a trader follows their predefined trading rules, often tracked in a journal.

[24] setup quality — An assessment of how well a trade opportunity matches a trader's predefined criteria for entry, based on technical or fundamental analysis.

[25] tail risk — The risk of rare but extreme events that can cause large losses, often underestimated in standard risk models.

[26] time-series data — A sequence of data points recorded at successive times, such as daily profit/loss figures or emotional state scores.

[27] trade log — A record of executed trades containing objective data such as entry/exit prices, position size, and financial outcome.

[28] trading journal — A tool used by traders to record both objective trade data and subjective psychological observations for performance analysis.

[29] win rate — The percentage of trades that result in a profit, calculated as the number of winning trades divided by total trades.

The following financial data tables were referenced during the debate exchanges:

| Dimension | Financial Outcome Logging | Psychological State Tracking |

|---|---|---|

| Data Availability | Already captured by broker | Ephemeral; lost if not recorded |

| Causal Position | Downstream symptom | Upstream cause |

| Actionability | Descriptive only | Prescriptive; enables rule creation |

| Information Uniqueness | Redundant with broker records | Proprietary; no alternative source |

| Behavioral Impact | Cannot modify behavior | Directly enables self-modification |

Legend: Comparative analysis of two trading journal components. Financial outcome logging provides descriptive metrics already available through broker statements; psychological tracking captures unique causal data that enables behavioral modification.

</FinancialData>

| Data Type | Measurement Method | Predictive Power | Timing |

|---|---|---|---|

| Financial outcomes | Broker statements | None (descriptive) | Lagging |

| Win rate, drawdown | Automated calculation | None (descriptive) | Lagging |

| Emotional discipline | TPI standardized scales | High (predictive) | Leading |

| Fear/greed triggers | Real-time journaling | High (predictive) | Leading |

| Impulsivity scores | Validated instruments | Moderate-High | Leading |

Legend: Comparison of financial vs. psychological data in trading journals. TPI = Trading Psychology Inventory, a validated psychometric instrument. Predictive power indicates ability to forecast future performance.

</FinancialData>

| Component | Role | Necessity | Sufficiency |

|---|---|---|---|

| Financial outcome logging | Performance measurement | Necessary | Insufficient |

| Psychological state tracking | Performance improvement | Necessary | Sufficient (when combined with financial data) |

| Combined integration | Complete feedback loop | Necessary | Sufficient |

Legend: Analysis of trading journal components. Financial logging measures outcomes; psychological tracking enables improvement. Both are necessary, but psychological tracking is the active ingredient that transforms data into behavioral change.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.