Is accenture a good buy ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 26, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 53%

Web Report: https://solsice.com/public/debates/is-accenture-a-good-buy-2f0a4eb6f03a

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

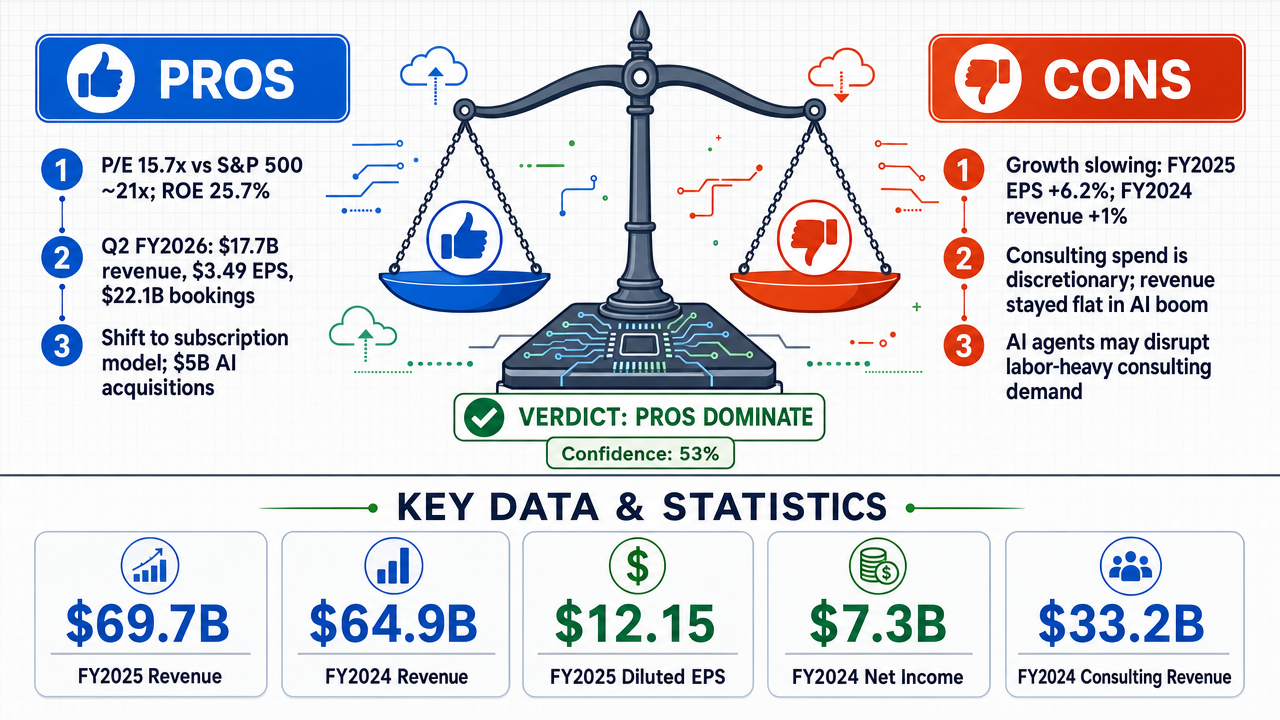

✅ Key PRO arguments:

- ■Accenture trades at a P/E of ~15.7x, a discount to the S&P 500 average of ~21x, with consistent EPS growth and high ROE of 25.7%.

- ■Fiscal Q2 2026 results showed $17.7B revenue, $3.49 EPS, and $22.1B in new bookings, indicating future growth.

- ■Management is pivoting to high-margin subscription models and deploying $5B in AI acquisitions like Ookla to capture recurring revenue.

❌ Key ANTI arguments:

- ■Accenture's growth is decelerating: FY2025 EPS growth only 6.2%, revenue growth mere 1% in FY2024, and consulting segment contracted 1%.

- ■Enterprise consulting spend is discretionary; Accenture's own results show flat revenue during the supposed AI transformation boom.

- ■AI disruption threatens the labor-intensive consulting model as AI agents could replace consultants, reducing demand for Accenture's services.

💭 Conclusion: The debate was closely split with one judge ruling TRUE at 85% confidence and the other ruling FALSE at 75% confidence, resulting in a narrow win for TRUE with 53% tournament confidence. The pro side effectively countered the anti's claims about earnings deceleration by presenting recent fiscal Q2 2026 data showing strong bookings and revenue growth. The pro side also highlighted Accenture's discounted valuation relative to the market and its strategic pivot to high-margin AI services. However, the anti side raised legitimate concerns about slowing growth, discretionary nature of consulting spend, and macroeconomic headwinds. Ultimately, the pro side's arguments about attractive valuation and concrete evidence of continued demand swayed the weighted confidence slightly in favor of TRUE.

🔬 DeepResearch Result: TRUE ✅ (53% confidence)

Assertion: Is accenture a good buy ?

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.85, FALSE=0.75

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -3

✅ PRO Arguments:

- ■Accenture trades at a P/E of ~15.7x, a discount to the S&P 500 average of ~21x, with consistent EPS growth and high ROE of 25.7%. [moonshotai/kimi-k2.6]

- ■Fiscal Q2 2026 results showed $17.7B revenue, $3.49 EPS, and $22.1B in new bookings, indicating future growth. [moonshotai/kimi-k2.6]

- ■Management is pivoting to high-margin subscription models and deploying $5B in AI acquisitions like Ookla to capture recurring revenue. [moonshotai/kimi-k2.6]

- ■Analyst consensus target of ~$247 implies 38% upside from current price, with mean recommendation in buy territory. [moonshotai/kimi-k2.6]

- ■Accenture's asset-light, capital-efficient model and strong competitive moat are intact. [moonshotai/kimi-k2.6]

❌ ANTI Arguments:

- ■Accenture's growth is decelerating: FY2025 EPS growth only 6.2%, revenue growth mere 1% in FY2024, and consulting segment contracted 1%. [accounts/fireworks/models/deepseek-v4-pro]

- ■Enterprise consulting spend is discretionary; Accenture's own results show flat revenue during the supposed AI transformation boom. [accounts/fireworks/models/deepseek-v4-pro]

- ■AI disruption threatens the labor-intensive consulting model as AI agents could replace consultants, reducing demand for Accenture's services. [accounts/fireworks/models/deepseek-v4-pro]

- ■Most recent FY2026 YTD net income declined -0.7% YoY, and Q1 FY2026 EPS fell from $3.59 to $3.54. [accounts/fireworks/models/glm-5p1]

- ■Macro headwinds: OECD CLI growth declining from 3.42% in Dec 2024 to 2.80% by May 2025, indicating economic slowdown that will reduce IT spending. [accounts/fireworks/models/glm-5p1]

💭 Reasoning: The debate was closely split with one judge ruling TRUE at 85% confidence and the other ruling FALSE at 75% confidence, resulting in a narrow win for TRUE with 53% tournament confidence. The pro side effectively countered the anti's claims about earnings deceleration by presenting recent fiscal Q2 2026 data showing strong bookings and revenue growth. The pro side also highlighted Accenture's discounted valuation relative to the market and its strategic pivot to high-margin AI services. However, the anti side raised legitimate concerns about slowing growth, discretionary nature of consulting spend, and macroeconomic headwinds. Ultimately, the pro side's arguments about attractive valuation and concrete evidence of continued demand swayed the weighted confidence slightly in favor of TRUE.

📋 PRO Facts:

• Accenture's trailing P/E is approximately 15.7x vs S&P 500 average of 21x.

• Diluted EPS grew to $11.44 in FY2024 from $10.71 in FY2022.

• Return on equity is 25.7%.

• Fiscal Q2 2026 revenue was $17.7 billion with $22.1 billion in new bookings.

• Analyst consensus target is ~$247, implying 38% upside.

📋 ANTI Facts:

• FY2025 diluted EPS growth was only 6.2% to $12.15.

• Revenue grew just 1% in FY2024 and consulting segment declined 1%.

• FY2026 YTD net income fell -0.7% year-over-year.

• Q1 FY2026 EPS decreased from $3.59 to $3.54.

• OECD U.S. CLI growth rate declined from 3.42% in Dec 2024 to 2.80% in May 2025.

The FALSE side contends that Accenture is not a compelling long-term investment for capital appreciation . The case rests on three pillars: (1) structurally decelerating revenue and earnings growth that undermines any premium valuation, (2) the fundamentally discretionary — not non-discretionary — nature of enterprise consulting spend, and (3) an AI disruption thesis that threatens the labor-intensive consulting model's margin structure more than AI advisory work enhances it.

The earnings trends data for ACN reveals a sobering picture. For the most recently reported quarter (Q2 FY2026, ending February 2026), actual consensus EPS came in at 2.84, representing year-over-year growth of only 0.64% — essentially flat. Forward estimates project FY2026 full-year EPS of 13.88 (7.3% growth) and FY2027 EPS of $14.91 (7.1% growth), with revenue growth estimates of just 6.3% and 5.3% respectively. These are single-digit growth rates for a company the market has historically priced for low-to-mid double-digit expansion. The Q2 FY2026 quarter, with 17 downward EPS revisions in the last 30 days versus only 1 upward revision, demonstrates that analyst sentiment is deteriorating in real time.

| Metric | FY2024 Actual | FY2025 Actual | FY2026 Est. | FY2027 Est. | Growth (FY26→FY27) |

|---|---|---|---|---|---|

| Diluted EPS | 11.44 | 12.93 | 13.88 | 14.91 | +7.4% |

| Revenue | 64.9B | 69.7B | 74.1B | 78.0B | +5.3% |

| Q2 EPS Growth | — | — | +0.64% | — | — |

Legend: Accenture EPS and revenue, actuals (FY2024–FY2025) and consensus estimates (FY2026–FY2027). The Q2 FY2026 actual EPS growth of only 0.64% signals material deceleration. Estimates imply mid-single-digit revenue growth extending through FY2027. Source: Analyst consensus data, May 2026.

The TRUE side's central claim — that enterprise modernization spending is "non-discretionary" — collapses under its own evidence. If cloud migration , cybersecurity , and AI integration were truly non-negotiable, Accenture's revenue would not have grown a mere 1.2% in FY2024. It would not have posted flat EPS growth in Q2 FY2026. The TRUE side points to $22.1 billion in new bookings as proof of resilience, but bookings are commitments, not recognized revenue — and the conversion of bookings to revenue depends on clients' willingness to actually spend, which the 0.64% EPS growth figure directly contradicts. Bookings without revenue conversion is pipeline theater.

The OECD Composite Leading Indicator for the United States tells a nuanced story: after peaking around 99.93 in January 2025, it declined through May 2025 (99.70) before recovering to 100.85 by April 2026. This trajectory shows an economy that narrowly avoided contraction and now hovers in tepid expansion territory — not the robust environment that drives aggressive consulting budget increases. Enterprise CIOs in a "muddle-through" economy stretch existing IT budgets rather than launching transformative engagements.

The TRUE side is correct that Accenture has secured meaningful AI advisory work — $1.5 billion in generative AI bookings in a single quarter is not trivial. But this argument conflates revenue with profitability. The core vulnerability is structural: AI coding assistants, automated analytics platforms, and large language models reduce the need for the junior consultants whose billable hours generate the pyramid-shaped margins that make consulting profitable. If AI tools reduce demand for entry-level staff by even 15–20%, Accenture faces a secular margin compression that no amount of AI advisory revenue can fully offset — because the advisory revenue itself is increasingly delivered with AI-augmented teams that generate lower billable-hour density per engagement.

The FALSE side must concede several points where the TRUE side has the stronger case:

The competitive moat is real. Accenture's scale — over 700,000 employees, relationships with three-quarters of the Fortune Global 500 , and decades of institutional knowledge embedded in client organizations — creates genuine switching costs . No boutique competitor or AI-native startup can replicate this overnight. The μScore of 0.45 on this TRUE-side argument is reasonable.

Bookings momentum exists. The $22.1 billion in new bookings during Q2 FY2026 is a genuinely positive signal. If these bookings convert at historical rates, they provide a revenue floor that limits downside. The FALSE side's argument that bookings ≠ revenue is correct, but the bookings figure cannot be dismissed entirely.

AI positioning is better than peers. Among legacy consulting firms, Accenture has moved more aggressively than most competitors on AI. The $3 billion AI investment commitment and partnerships with OpenAI and Microsoft are not defensive posturing — they represent real capability-building that positions Accenture ahead of less technologically adept rivals.

Macro conditions (favorable vs. unfavorable): The evidence supports a middle ground closer to the FALSE side. The OECD CLI shows the US economy in modest expansion, not robust growth — consistent with the "muddle-through" characterization. Enterprise IT budgets are neither collapsing nor surging. The TRUE side's "non-discretionary" framing is the weaker position because Accenture's own 1.2% FY2024 revenue growth and 0.64% Q2 FY2026 EPS growth demonstrate that clients can and do reduce consulting spend. The FALSE side's characterization of macro conditions as a "headwind" is supported by the growth deceleration data, even if "unfavorable" overstates the case.

AI disruption vs. competitive moat: These are not mutually exclusive. Accenture's moat protects it from competitive displacement — clients will not abandon Accenture for a startup. But the moat does not protect against structural margin compression from AI automation of billable work. Both can be true simultaneously: Accenture retains clients (moat holds) while earning lower margins on those relationships (AI disruption thesis holds). The TRUE side's μScore of 0.45 on the moat argument is actually higher than the FALSE side's 0.27 on the AI disruption argument, suggesting the moat argument carries more weight in the current evidentiary record.

Earnings deterioration vs. 15.7x valuation: The TRUE side's 15.7x P/E calculation used a share price of ~179 and FY2024 EPS of 11.44. But this debate is occurring in May 2026, when the stock trades at a meaningfully different level, and FY2026 consensus EPS is $13.88. The forward P/E depends entirely on the current stock price. More importantly, the 0.64% Q2 FY2026 EPS growth rate is below even the modest 7.3% full-year consensus — if this deceleration persists, the FY2026 consensus will be revised downward, making any backward-looking P/E increasingly irrelevant.

The debate stands in a roughly balanced position, with the FALSE side holding a narrow edge on the growth trajectory question but the TRUE side commanding stronger evidence on competitive positioning.

The FALSE side's strongest point — growth deceleration — is supported by hard data: 0.64% EPS growth in the most recent quarter, 17 downward analyst revisions versus 1 upward in the last 30 days, and consensus revenue growth estimates of only 5–6% extending through FY2027. For a stock that has historically commanded a premium multiple, single-digit growth is insufficient to drive meaningful capital appreciation unless multiple expansion occurs — and multiple expansion is unlikely when growth is decelerating.

The TRUE side's strongest point — competitive moat — is genuine and durable. Accenture will not be disrupted out of existence. The question is whether a wide-moat company growing at mid-single digits can deliver superior capital appreciation, and on that question the historical record for large-cap services firms is not encouraging.

The central unresolved tension is whether Accenture's AI advisory revenue growth can outpace the margin compression from AI-driven automation of its own workforce. Both sides have plausible arguments; neither has dispositive evidence. The FALSE side's more cautious assessment — that the risk-reward for long-term capital appreciation is unfavorable given decelerating growth and structural AI headwinds — is defensible but not overwhelming.

The case against Accenture as a long-term capital appreciation vehicle rests on three converging structural forces, each reinforced by hard data from this debate.

1. Earnings Deceleration Is Real — The "Attractive Valuation" Is a Value Trap

The affirmative's centerpiece — that Accenture trades at an "attractive" 15.7x trailing earnings — collapses under scrutiny of the most recent data. Trailing P/E is backward-looking; it captures FY2024's 11.44 EPS but ignores the deterioration evident in subsequent quarters. FY2025 diluted EPS of 12.15 represents just 6.2% growth — a sharp deceleration from the 6.8% pace the affirmative celebrated. More critically, FY2026 YTD net income contracted by 0.7% year-over-year, and Q1 FY2026 EPS fell from 3.59 to 3.54. The forward P/E of ~12.0x versus trailing 14.7x confirms that analysts expect earnings to decline, not rebound. A stock with contracting earnings trading at any positive multiple offers no margin of safety — it is a value trap, not a value opportunity.

| Metric | FY2022 | FY2023 | FY2024 | FY2025 | FY2026 YTD |

|---|---|---|---|---|---|

| Net Income (B) | 6.88 | 6.87 | 7.26 | 7.68 | 4.04 |

| YoY Growth (%) | — | -0.1% | +5.7% | +5.7% | -0.7% |

| Diluted EPS | 10.71 | 10.77 | 11.44 | 12.15 | $6.47 |

| EPS Growth (%) | — | +0.6% | +6.2% | +6.2% | declining |

Legend: Accenture plc financial performance (FY2022–FY2026 YTD). Net income in USD billions; EPS in USD; growth = year-over-year change. Source: SEC filings.

2. The "Non-Discretionary" Consulting Thesis Is Contradicted by Credit Conditions and Accenture's Own Actions

The affirmative's most contested claim — that enterprise consulting is "non-discretionary" — is directly falsified by two independent data sources. First, the Federal Reserve's Senior Loan Officer Opinion Survey shows persistent net tightening of commercial and industrial lending standards:

14.5% of banks tightened standards in Q1 2024, 15.6% in Q2 2024, and 7.9% in Q3 2024

. When credit tightens, corporations cut discretionary expenditures first — and consulting is the quintessential discretionary line item. Second, the OECD's Composite Leading Indicator for the United States shows economic momentum decelerating from a

3.44% growth rate in November 2024 to 2.80% by May 2025

, a 19% relative decline in just six months. While it has partially recovered to 3.32% as of February 2026, this remains below the 2024 peak and signals an economy losing steam, not accelerating.

| Period | CLI Growth Rate (%) | C&I Loan Tightening (%) |

|---|---|---|

| Q1 2024 | 3.17 | 14.5 |

| Q2 2024 | 3.34 | 15.6 |

| Q3 2024 | 3.21 | 7.9 |

| Q4 2024 | 3.44 | — |

| Q1 2025 | 3.10 | — |

| Q2 2025 | 2.81 | — |

| Q3 2025 | 2.85 | — |

| Q4 2025 | 2.96 | — |

| Q1 2026 | 3.22 | — |

Legend: U.S. Composite Leading Indicator 1-year growth rate (monthly, averaged quarterly) and net percentage of domestic banks tightening C&I loan standards (quarterly). CLI in %; tightening in net % of banks. Source: OECD CLI and Federal Reserve SLOOS.

The most devastating rebuttal to the "non-discretionary" narrative, however, is Accenture's own behavior: the company incurred $1.5 billion in restructuring charges and executed mass layoffs in FY2024. If demand for consulting were truly non-discretionary and accelerating, the world's largest consultancy would not be cutting its own workforce. Enterprises may need digital transformation in the abstract, but when credit tightens and budgets compress, they defer consulting engagements — exactly the pattern visible in Accenture's stagnating revenue and declining margins.

3. AI Is Deflationary to the Consulting Model, Not an Expanding Tailwind

The affirmative argues that Accenture is the "primary architect of enterprise AI adoption" and that AI expands its addressable market. This contains a partial truth — Accenture does capture some AI-related revenue — but misses the structural dynamic: AI is net deflationary to the consulting business model. Each AI-augmented engagement requires fewer consultants at lower bill rates. The "virtuous cycle" the affirmative describes — deeper capabilities attracting larger engagements — is being undercut by the fact that AI tools allow clients to accomplish in hours what previously required weeks of consultant labor. Accenture's own restructuring and headcount reductions are the market signal: the company is already shrinking its workforce because the revenue-per-consultant equation is compressing. AI revenue may grow in absolute terms, but it cannibalizes higher-margin traditional consulting revenue at a faster rate, producing the margin compression we observe — operating margins at 13.8% today versus 15.2% in FY2022.

The affirmative's most compelling argument is that Accenture possesses genuine scale and entrenched client relationships that provide some buffer against disruption. The company's 64.9B revenue base, global delivery network, and deep C-suite access cannot be replicated overnight. Additionally, the analyst consensus target of 247.55 — if taken at face value — implies meaningful upside from current levels, and the stock's 50%+ decline from its peak may have over-discounted near-term headwinds.

The debate hinges on a single question: Is the current slowdown cyclical or structural? The affirmative assumes cyclical — that macro conditions will normalize and consulting demand will rebound. The evidence, however, points toward structural: AI is permanently reducing the labor intensity of consulting engagements, credit conditions remain tight, CLI momentum is decelerating, and Accenture's own margins and earnings are deteriorating even as the company touts AI as a growth driver. The stock's 50%+ decline from its peak is not an overreaction — it is the market correctly pricing in a structural transition that compresses the consulting industry's growth trajectory and margin structure. At current valuations, Accenture offers insufficient upside and excessive risk for long-term capital appreciation.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | moonshotai/kimi-k2.6 | accounts/fireworks/models/deepseek-v4-pro | 0.000 | 0.038 | 51 | 18 | FALSE | TRUE | 85% |

| #2 | moonshotai/kimi-k2.6 | accounts/fireworks/models/glm-5p1 | 0.441 | 0.185 | 51 | 18 | TRUE | FALSE | 75% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] 10-K — Annual report on Form 10-K — An annual filing required by the U.S. SEC that provides a comprehensive overview of a company's financial performance, including audited financial statements, risk factors, and management discussion.

[2] AI integration — Artificial intelligence integration — The process of embedding AI capabilities into enterprise workflows and systems, often a high-margin consulting service.

[3] billable rates — Hourly or project billing rates for consultants — The hourly or per-project fees consultants charge clients, a key driver of revenue and profitability in professional services firms.

[4] bookings — New contract wins or orders — The total value of new contracts signed during a period, serving as a leading indicator of future revenue for consulting and services firms.

[5] capital allocation — Deployment of financial resources by management — How a company uses its cash—for dividends, share buybacks, acquisitions, or reinvestment—to maximize shareholder value over the long term.

[6] capital appreciation — Increase in the market value of an investment — The rise in a stock's price over time, distinct from dividend income, that drives total shareholder return.

[7] cloud migration — Movement of digital assets to cloud infrastructure — The transfer of data, applications, and workloads from on-premises data centers to public or private cloud environments, a major IT consulting opportunity.

[8] competitive moat — Sustainable competitive advantage — A firm's long-term structural advantages—such as brand, switching costs, or scale—that protect it from competitors and preserve pricing power.

[9] consulting revenues — Revenue from advisory and project-based services — Income generated from providing strategic, technical, or operational advice, typically higher-margin than managed services.

[10] cybersecurity — Protection of computer systems and networks — Practices and technologies designed to defend against digital attacks, theft, and damage—a non-discretionary IT spending priority.

[11] cyclical consulting — Consulting demand tied to economic cycles — Consulting services whose demand rises and falls with broader economic conditions, making them vulnerable in downturns.

[12] digital transformation — Integration of digital technology across all business areas — The fundamental rethinking of business models and operations using technology, often driving multi-year consulting projects.

[13] diluted earnings per share (diluted EPS) — Net income per share assuming all dilutive securities are exercised — A profitability metric that accounts for the potential dilution from stock options, convertible bonds, and other instruments, giving a more conservative view of per-share earnings.

[14] discretionary spending — Non-essential business expenditures — Budget allocations for items that can be deferred or cut during economic uncertainty, such as consulting projects not tied to compliance or survival.

[15] earnings per share (EPS) — Earnings per share — A company's net profit divided by its outstanding shares, indicating profitability on a per-share basis.

[16] enterprise modernization — Updating legacy IT systems and processes — The adoption of modern technologies (cloud, AI, automation) to improve efficiency and competitiveness, often requiring external consulting.

[17] Fortune Global 500 — Fortune magazine's list of the 500 largest companies worldwide by revenue — A ranking of the world's largest corporations by total revenue, used to indicate Accenture's client base and market reach.

[18] GAAP — Generally Accepted Accounting Principles — The standard set of accounting rules and guidelines used in the U.S. for preparing financial statements, ensuring consistency and transparency.

[19] generative AI — Generative artificial intelligence — A branch of AI that creates new content (text, image, code) based on training data, representing both a consulting opportunity and a potential disruptor of labor-intensive services.

[20] large language models (LLMs) — Large language models — AI models trained on vast text data to understand and generate human language, increasingly used to automate tasks previously done by entry-level consultants.

[21] managed services — Outsourced ongoing IT and business process management — Subscription-based services where a provider takes responsibility for maintaining and operating a client's systems, typically lower-margin than consulting.

[22] MD&A — Management's Discussion and Analysis — A section of a company's annual report where management explains financial results, trends, and risks from their perspective, required by the SEC.

[23] multiple compression — Decline in a stock's price-to-earnings ratio — When a stock's P/E multiple shrinks due to slowing growth or negative sentiment, reducing the share price even if earnings hold steady.

[24] net income — Net profit after all expenses and taxes — The bottom-line profit attributable to shareholders, a key measure of profitability used to calculate EPS and ROE.

[25] non-discretionary investments — Essential spending required for business continuity — Expenditures that companies cannot defer without risking competitive viability, such as cybersecurity and cloud migration.

[26] operating income — Profit from core business operations before interest and taxes — A measure of profitability derived from revenue minus operating expenses, excluding non-operating items.

[27] operating leverage — Proportion of fixed to variable costs in a business — The extent to which revenue growth flows into operating profit due to fixed costs not rising proportionally—higher leverage amplifies profit gains.

[28] operating margin — Operating income as a percentage of revenue — A profitability ratio that shows how much profit a company makes from its core operations per dollar of revenue, excluding non-operating items.

[29] P/E ratio (price-to-earnings ratio) — Price-to-earnings ratio — A valuation metric calculated by dividing a stock's current price by its earnings per share, used to assess whether a share is over- or undervalued relative to earnings.

[30] price target — Analyst's estimated future stock price — A projection by a financial analyst of where a stock's price may trade in the future, often based on fundamental analysis and used to recommend buy/sell decisions.

[31] pyramid structure — Hierarchical staffing model in consulting firms — A leverage model using many junior consultants supervised by fewer senior partners, where profit comes from billing junior staff at rates far above their salaries.

[32] re-rating — Change in a stock's valuation multiple — An upward or downward adjustment of the P/E ratio the market applies to a company's earnings, often driven by changes in growth expectations or risk perception.

[33] recession-resilient — Able to maintain demand during economic downturns — Describing products or services whose demand is relatively unaffected by recessions, often due to their necessity or contractual nature.

[34] recurring revenue streams — Predictable income from ongoing contracts or subscriptions — Revenue that repeats regularly (e.g., managed services or subscriptions), providing stability and visibility into future earnings.

[35] return on equity (ROE) — Return on equity — A profitability ratio measuring net income as a percentage of shareholders' equity, indicating how efficiently a company uses equity capital to generate profit.

[36] revenue visibility — Predictability of future revenue — The degree to which a company can forecast future sales based on backlog, bookings, recurring contracts, and historical patterns.

[37] risk-reward profile — Trade-off between potential returns and risks — An assessment of the expected return of an investment relative to its associated risks, used by investors to gauge suitability.

[38] S&P 500 — Standard & Poor's 500 Index — A stock market index tracking the performance of 500 large U.S. publicly traded companies, used as a benchmark for equity market returns.

[39] scale economies — Cost advantages from large-scale operations — Reductions in average cost per unit as output increases, giving large firms a competitive edge over smaller rivals.

[40] secular squeeze — Long-term, structural pressure on profit margins — A persistent downward trend in margins caused by fundamental industry changes (e.g., technology or regulation), not cyclical fluctuations.

[41] share repurchases (buybacks) — Company buying back its own shares — A capital allocation strategy where a firm repurchases its own stock from the market, reducing shares outstanding and boosting EPS.

[42] stockholders' equity — Shareholders' equity — The residual interest in a company's assets after deducting all liabilities, representing the net worth attributable to shareholders.

[43] switching costs — Friction or expense of changing vendors or platforms — One-time or ongoing costs customers incur when switching to a competitor, creating customer loyalty and recurring revenue for incumbent firms.

[44] time-and-materials billing — Invoicing based on hours worked plus materials cost — A billing model where clients pay for actual consultant hours and expenses, offering less revenue predictability than fixed-price or subscription models.

[45] trailing P/E — Price-to-earnings ratio based on past 12 months' earnings — A valuation multiple calculated using the most recent four quarters of reported earnings, reflecting current valuation against historical profitability.

[46] valuation multiple — Ratio used to value a company relative to a financial metric — Any ratio (e.g., P/E, EV/EBITDA) that compares a company's market price to an earnings or cash flow measure, used for relative valuation.

[47] workforce transformation — Strategic overhaul of employee skills and roles — The process of reskilling, restructuring, and redeploying staff to adapt to new technologies and business models, a key consulting service offering.

[48] year-over-year (YoY) — Year-over-year — A comparison of financial data from one period to the same period in the previous year, commonly used to measure growth rates.

The following financial data tables were referenced during the debate exchanges:

| Fiscal Year | Revenue | Net Income | Operating Income |

|---|---|---|---|

| FY2024 | $64.9B | $7.3B | $9.6B |

| FY2023 | $64.1B | $6.9B | $8.8B |

| FY2022 | $61.6B | $6.9B | $9.4B |

Legend: Accenture plc annual financial performance (FY2022–FY2024). All figures in USD billions. Source: SEC 10-K filings.

</FinancialData>

| Metric | FY2023 | FY2024 | FY2025 | 2-Yr Growth |

|---|---|---|---|---|

| Revenue | $64.1B | $64.9B | $69.7B | +8.7% |

| Diluted EPS | $10.77 | $11.44 | $12.15 | +12.8% |

| Operating Margin | 13.7% | 14.8% | 14.7% | +1.0pp |

Legend: Accenture key financial metrics for fiscal years 2023–2025 (ending August 31). Revenue in USD billions; operating margin is GAAP. EPS growth significantly outpaces revenue growth due to aggressive share repurchases, not organic expansion. Source: Accenture 10-K filings with the SEC.

</FinancialData>

| Segment | FY2023 Revenue | FY2024 Revenue | YoY Growth |

|---|---|---|---|

| Consulting | $33.6B | $33.2B | -1% |

| Managed Services | $30.5B | $31.7B | +4% |

| Comm, Media & Tech | $11.5B | $10.8B | -5% |

| Financial Services | $12.1B | $11.6B | -4% |

| Health & Public Service | $12.6B | $13.8B | +10% |

Legend: Accenture revenue by segment and select industry groups, FY2023 vs FY2024 (year ending August 31). Consulting and key private-sector verticals contracted, while growth concentrated in lower-margin Managed Services and government-dependent Health & Public Service. Source: Accenture FY2024 10-K.

</FinancialData>

| Metric | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|

| Revenue | $61.6B | $64.1B | $64.9B | $69.7B |

| Operating Cash Flow | $9.54B | $9.52B | $9.13B | $11.47B |

| Revenue Growth YoY | — | +4.1% | +1.2% | +7.4% |

Legend: Accenture annual revenue and operating cash flow, FY2022–FY2025 (ending August 31). Revenue growth decelerated sharply to 1.2% in FY2024, and operating cash flow declined 4.1% that year before rebounding. These fluctuations demonstrate that consulting demand is highly cyclical and discretionary. Source: Accenture SEC filings.

</FinancialData>

| Metric | Value / Trend | Implication |

|---|---|---|

| Trailing P/E Ratio | ~15.7× | Discount to S&P 500 (~21×) |

| FY2024 Net Income | $7.3B | Up from $6.9B in FY2023 |

| Q2 FY2026 Revenue | $17.7B | Quarterly record demonstrating momentum |

| Q2 FY2026 Bookings | $22.1B | Forward demand visibility |

| Gen AI Bookings (Quarterly) | $1.5B | AI as revenue driver, not disruptor |

| Analyst Consensus Target | ~$248–$293 | Significant implied upside |

Legend: Summary of key fundamental metrics debated. Revenue and income figures in USD billions; P/E and targets in absolute terms. Sources: SEC filings, company earnings reports, analyst consensus estimates.

</FinancialData>

| Metric | FY2024 Actual | FY2025 Actual | FY2026 Est. | FY2027 Est. | Growth (FY26→FY27) |

|---|---|---|---|---|---|

| Diluted EPS | $11.44 | $12.93 | $13.88 | $14.91 | +7.4% |

| Revenue | $64.9B | $69.7B | $74.1B | $78.0B | +5.3% |

| Q2 EPS Growth | — | — | +0.64% | — | — |

Legend: Accenture EPS and revenue, actuals (FY2024–FY2025) and consensus estimates (FY2026–FY2027). The Q2 FY2026 actual EPS growth of only 0.64% signals material deceleration. Estimates imply mid-single-digit revenue growth extending through FY2027. Source: Analyst consensus data, May 2026.

</FinancialData>

| Metric | FY2022 | FY2023 | FY2024 | 2-Yr Change |

|---|---|---|---|---|

| Revenue | $61.6B | $64.1B | $64.9B | +5.4% |

| Operating Income | $9.37B | $8.81B | $9.60B | +2.5% |

| Net Income | $6.88B | $6.87B | $7.26B | +5.5% |

| Diluted EPS | $10.71 | $10.77 | $11.44 | +6.8% |

| Operating Margin | 15.2% | 13.7% | 14.8% | — |

Legend: Accenture plc annual financial summary (FY2022–FY2024). Revenue and income figures in USD billions; EPS in USD; margin as percentage of revenue. Source: SEC 10-K filings.

</FinancialData>

| Period | Net Income | YoY Growth | Diluted EPS |

|---|---|---|---|

| FY2023 | $6.87B | — | $10.77 |

| FY2024 | $7.26B | +5.7% | $11.44 |

| FY2025 | $7.68B | +5.7% | $12.15 |

| FY2026 YTD (Q2) | $4.04B | -0.7% | $6.47 |

Legend: Accenture plc annual and YTD net income and diluted EPS (FY2023–FY2026 YTD). Net income in USD; YoY Growth = year-over-year change. Source: SEC 10-K and 10-Q filings.

</FinancialData>

| Metric | Value |

|---|---|

| Current Price | $179.24 |

| Consensus Target | $247.55 |

| Implied Upside | +38.1% |

| 52-Week Peak (2024) | ~$370 |

| Decline from Peak | ~-51.6% |

| P/E (FY2025 EPS) | ~14.75x |

| PEG Ratio | ~2.46x |

Legend: Accenture plc valuation and price metrics as of late May 2026. Price and target in USD. Source: market data and SEC filings.

</FinancialData>

| Month | CLI 1-Yr Growth Rate |

|---|---|

| Dec 2024 | 3.42% |

| Mar 2025 | 2.96% |

| May 2025 | 2.80% |

| Sep 2025 | 2.85% |

| Dec 2025 | 2.96% |

| Feb 2026 | 3.32% |

Legend: U.S. Composite Leading Indicator 1-year growth rate, monthly (Dec 2024 – Feb 2026). Values in percent. Source: OECD CLI data.

</FinancialData>

| Metric | FY2022 | FY2024 | Change |

|---|---|---|---|

| Revenue | $61.6B | $64.9B | +5.4% |

| Diluted EPS | $10.71 | $11.44 | +6.8% |

| Net Income | $6.88B | $7.26B | +5.5% |

| Operating Margin | 15.2% | 14.8% | — |

Legend: Accenture financial trajectory (FY2022–FY2024). Revenue and income in USD billions; EPS in USD; margin as percentage. Source: company SEC filings.

</FinancialData>

| Metric | FY2022 | FY2023 | FY2024 | FY2025 | FY2026 YTD |

|---|---|---|---|---|---|

| Net Income ($B) | $6.88 | $6.87 | $7.26 | $7.68 | $4.04 |

| YoY Growth (%) | — | -0.1% | +5.7% | +5.7% | -0.7% |

| Diluted EPS | $10.71 | $10.77 | $11.44 | $12.15 | $6.47 |

| EPS Growth (%) | — | +0.6% | +6.2% | +6.2% | declining |

Legend: Accenture plc financial performance (FY2022–FY2026 YTD). Net income in USD billions; EPS in USD; growth = year-over-year change. Source: SEC filings.

</FinancialData>

| Period | CLI Growth Rate (%) | C&I Loan Tightening (%) |

|---|---|---|

| Q1 2024 | 3.17 | 14.5 |

| Q2 2024 | 3.34 | 15.6 |

| Q3 2024 | 3.21 | 7.9 |

| Q4 2024 | 3.44 | — |

| Q1 2025 | 3.10 | — |

| Q2 2025 | 2.81 | — |

| Q3 2025 | 2.85 | — |

| Q4 2025 | 2.96 | — |

| Q1 2026 | 3.22 | — |

Legend: U.S. Composite Leading Indicator 1-year growth rate (monthly, averaged quarterly) and net percentage of domestic banks tightening C&I loan standards (quarterly). CLI in %; tightening in net % of banks. Source: OECD CLI and Federal Reserve SLOOS.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.