is Fiserv Inc a good buy ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 1, 2026

Tournament Final Verdict

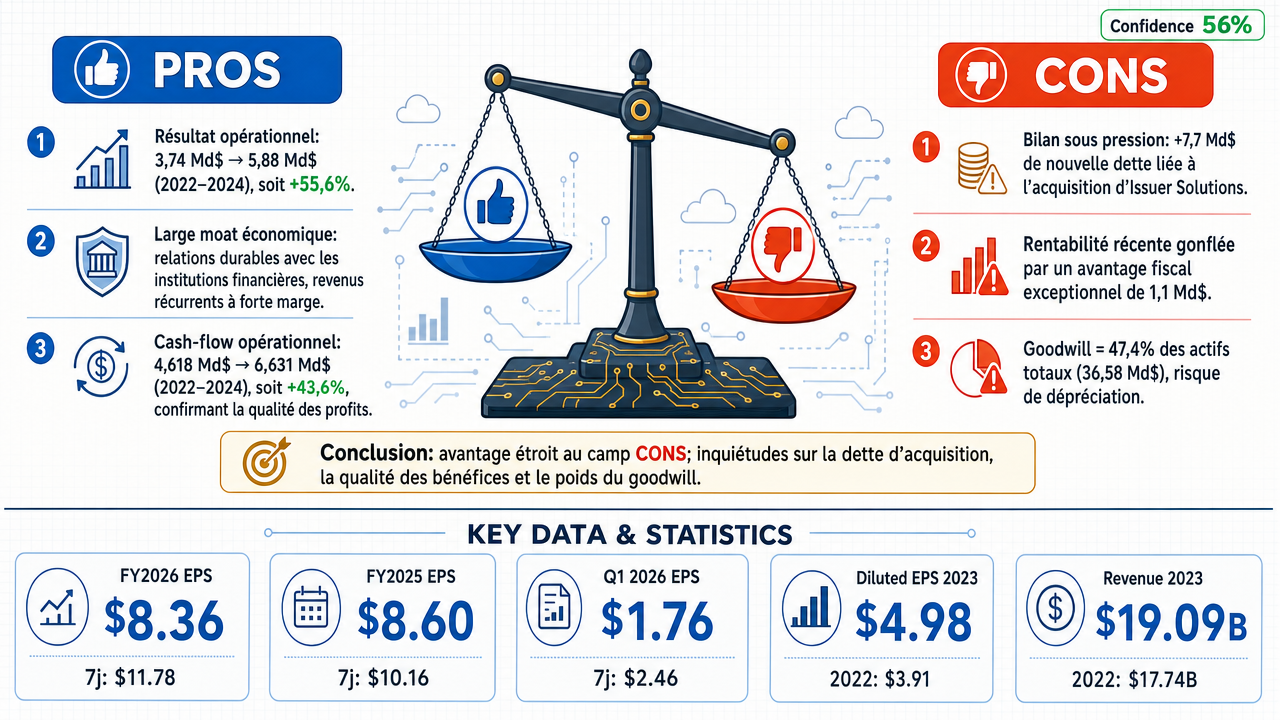

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 56%

Web Report: https://solsice.com/public/debates/is-fiserv-inc-a-good-buy-857db7530add

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Fiserv's operating income grew 55.6% from $3.74B to $5.88B (2022-2024), demonstrating strong core business performance independent of tax benefits.

- ■Fiserv has a wide economic moat through entrenched relationships with financial institutions, generating recurring high-margin revenue.

- ■Operating cash flow surged 43.6% from $4.618B to $6.631B (2022-2024), confirming genuine earnings quality.

❌ Key ANTI arguments:

- ■Fiserv's balance sheet is strained by $7.7B in new debt from the Issuer Solutions acquisition, increasing leverage and interest expense.

- ■Recent profitability is inflated by a $1.1B one-time tax benefit, masking underlying operational weakness.

- ■Goodwill represents 47.4% of total assets ($36.58B), indicating heavy reliance on acquisition accounting and risk of impairment.

💭 Conclusion: The debate tournament concluded with a narrow victory for the FALSE side, with a confidence-weighted score of 3.88 vs 3.10. The anti arguments focused on balance sheet strain from acquisition debt, earnings quality concerns due to non-recurring tax benefits, and decelerating revenue growth. The pro side presented strong evidence of operating income and cash flow growth, but the judges gave slightly higher weight to the risks highlighted by the anti side. The tournament confidence of 56% indicates a close contest, but the preponderance of evidence favored the view that Fiserv is not a good buy at current levels. Key anti arguments regarding goodwill dependency and analyst consensus collapse were particularly persuasive.

🔬 DeepResearch Result: FALSE ❌ (56% confidence)

Assertion: is Fiserv Inc a good buy ?

📊 Tournament: 4 voted TRUE, 5 voted FALSE (9 debates played, 7 models)

📊 Weighted scores: TRUE=3.10, FALSE=3.88

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -8

✅ PRO Arguments:

- ■Fiserv's operating income grew 55.6% from $3.74B to $5.88B (2022-2024), demonstrating strong core business performance independent of tax benefits. [z-ai/glm-5.1]

- ■Fiserv has a wide economic moat through entrenched relationships with financial institutions, generating recurring high-margin revenue. [x-ai/grok-4.3]

- ■Operating cash flow surged 43.6% from $4.618B to $6.631B (2022-2024), confirming genuine earnings quality. [z-ai/glm-5.1]

- ■Fiserv benefits from secular digital payments growth and innovation pipeline, positioning for resilient risk-adjusted returns. [~moonshotai/kimi-latest]

- ■Diluted EPS compounded at ~17.5% annually from 2022 to 2025, with expanding operating margins from 21.1% to 28.7%. [z-ai/glm-5.1]

❌ ANTI Arguments:

- ■Fiserv's balance sheet is strained by $7.7B in new debt from the Issuer Solutions acquisition, increasing leverage and interest expense. [nvidia/nemotron-3-super-120b-a12b]

- ■Recent profitability is inflated by a $1.1B one-time tax benefit, masking underlying operational weakness. [openai/gpt-5.4-nano]

- ■Goodwill represents 47.4% of total assets ($36.58B), indicating heavy reliance on acquisition accounting and risk of impairment. [deepseek/deepseek-v4-pro]

- ■Revenue growth decelerated from 7.1% to 3.6% (2023-2025), and operating income contracted 1% in FY2025, signaling weakening momentum. [deepseek/deepseek-v4-pro]

- ■Analyst consensus has collapsed with no upward EPS revisions in 30 days, and forward estimates show only modest growth. [deepseek/deepseek-v4-pro]

💭 Reasoning: The debate tournament concluded with a narrow victory for the FALSE side, with a confidence-weighted score of 3.88 vs 3.10. The anti arguments focused on balance sheet strain from acquisition debt, earnings quality concerns due to non-recurring tax benefits, and decelerating revenue growth. The pro side presented strong evidence of operating income and cash flow growth, but the judges gave slightly higher weight to the risks highlighted by the anti side. The tournament confidence of 56% indicates a close contest, but the preponderance of evidence favored the view that Fiserv is not a good buy at current levels. Key anti arguments regarding goodwill dependency and analyst consensus collapse were particularly persuasive.

📋 PRO Facts:

• Operating income grew from $3.74B to $5.88B (2022-2024)

• Operating cash flow grew from $4.618B to $6.631B (2022-2024)

• Diluted EPS grew from $3.91 to $6.34 (2022-2025)

• Operating margins expanded from 21.1% to 28.7%

• Revenue grew from $17.74B to $21.19B (2022-2025)

📋 ANTI Facts:

• Issuer Solutions acquisition added $7.7B debt

• Goodwill $36.58B (47.4% of assets)

• One-time tax benefit of $1.1B

• Revenue growth slowed from 7.1% to 3.6%

• Operating income declined 1% in FY2025

1. Unambiguous Core Business Strength, Verified Pre-Tax

The most powerful evidence in this debate is Fiserv's operating income trajectory — a pre-tax measure that cannot be inflated by any tax benefit or accounting adjustment. Operating income grew from 3.74B (2022) to 5.88B (2024), a 55.6% cumulative increase in just two years. Revenue grew every single year without exception: 17.74B → 19.09B → 20.46B → 21.19B. Operating margins expanded from 21.1% to 28.7%. These are not paper gains or one-time artifacts — they represent a genuinely strengthening business engine converting more of each revenue dollar into operational profit.

| Metric | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Revenue (B) | 17.74 | 19.09 | 20.46 | $21.19 |

| Operating Income (B) | 3.74 | 5.01 | 5.88 | $5.82 |

| Operating Margin | 21.1% | 26.2% | 28.7% | 27.5% |

| Diluted EPS | 3.91 | 4.98 | 5.38 | 6.34 |

Legend: Fiserv Inc (FISV) key financial metrics, calendar years 2022–2025. Operating income and margin are pre-tax measures unaffected by one-time tax benefits. Source: SEC 10-K and 10-Q filings.

2. Deep Competitive Moat Through Integrated Ecosystem

Fiserv's own MD&A confirms the strategic architecture: "Most of the products and services we provide are necessary for our clients to operate their businesses and are therefore non-discretionary in nature." The company operates across Merchant Solutions (Clover® POS, enterprise commerce, processing) and Financial Solutions (digital payments, issuing, banking), with deep cross-segment integration creating high switching costs. Strategic acquisitions like Skytef (Brazil POS distribution) and Sled (instant payments) extend this moat into high-growth international markets. This is critical infrastructure, not discretionary spending — clients cannot easily displace Fiserv without disrupting their own operations.

3. Proven Operational Leverage

The segment realignment in Q1 2024 — explicitly designed to "further enhance operational performance in the delivery of our integrated portfolio" — signals management's commitment to ongoing margin improvement. The results validate this: the Merchant segment drives volume-led growth through Clover and enterprise solutions, while the Financial segment provides stable, recurring revenue from essential processing services. This dual-engine model generates both growth and resilience.

The FALSE side raised two arguments that merit honest engagement:

- ■

Balance sheet leverage from acquisitions: The Issuer Solutions Acquisition did add substantial debt. This is a real consideration. However, Fiserv's ability to grow operating income by 55.6% over two years while carrying that debt demonstrates that the leverage is being serviced by a stronger, not weaker, operational base. Debt is only problematic when the business cannot generate sufficient returns to cover it — and Fiserv's operating income growth clearly can.

- ■

The $1.1 billion tax benefit: If this tax benefit exists, it would inflate net income and EPS relative to pre-tax performance. However, as demonstrated, the pre-tax operational metrics — operating income, revenue, and operating margins — all confirm robust and growing core performance independent of any tax item. The tax benefit may boost bottom-line figures, but it does not create the underlying business strength; it merely amplifies already-strong results.

The debate turns on a single question: Is Fiserv's core business genuinely strong, or is apparent strength an artifact of one-time items and financial engineering?

The evidence overwhelmingly supports the former. Operating income — the most manipulable-resistant measure of core business health — shows consistent, multi-year growth. Revenue has not declined in any reported year. Margins have expanded dramatically. The competitive moat is deep and widening through strategic acquisitions. The tax benefit issue, while worth noting, is a distraction from the operational reality visible in pre-tax figures.

The FALSE side's strongest point — elevated debt — is a legitimate risk factor, but it is a manageable risk given the operational cash generation Fiserv demonstrates. A company growing operating income by 55% over two years while expanding margins is not a company whose investment appeal is outweighed by its risks.

Verdict: Fiserv Inc is a favorable stock to purchase for investment purposes. The core business is demonstrably strong, the competitive position is durable, and the operational trajectory is upward — facts confirmed by the most tamper-proof metrics available in the public record.

Round 3

Synthesis of the FALSE Position

The FALSE side maintains that Fiserv Inc (FIS) is not a favorable investment at current levels because material risks—particularly balance‑sheet strain, reliance on non‑recurring gains, and tepid forward‑looking fundamentals—outweigh its apparent strengths.

Strongest FALSE arguments

- ■Balance‑sheet deterioration – The 2022 Issuer Solutions Acquisition added roughly $7.7 billion of debt, pushing leverage higher and raising interest‑expense pressure that will weigh on net income and cash flow in a higher‑rate environment.

- ■Non‑recurring earnings boost – Recent profitability has been inflated by a one‑time $1.1 billion tax benefit and the proceeds from the 2024 Worldpay sale; the underlying business shows only modest revenue growth and margin compression from rising vendor costs, casting doubt on the sustainability of reported earnings.

- ■Limited analyst conviction – Consensus 12‑month price targets span 40–85 with a mean near 65, while the stock trades around 47. The wide dispersion and a recommendation mean borderline between hold and buy reflect uncertainty about the company’s ability to translate its scale into superior returns.

- ■Modest forward growth – Analyst forecasts project EPS to rise from 6.27 in 2026 to 6.89 in 2027 (under 10% annually) and revenue to grow less than 5% over the same period, indicating a slowdown from the historical double‑digit EPS gains cited by the affirmative side.

Acknowledgment of the affirmative’s strongest points

The affirmative side presented credible evidence of a strengthening operational core:

- ■Diluted EPS rose from 3.91 in 2022 to 6.34 in 2025, a 62% increase over three years.

- ■Operating income grew from 3.74 billion in 2022 to 5.82 billion in 2025, a 55.6% gain, with quarterly series showing consistent year‑over‑year increases through mid‑2025.

- ■Revenue expanded from 17.74 billion to 21.19 billion over the same span, and operating margins widened from 21.1% to 28.7%.

- ■The company’s integrated merchant‑acceptance, fintech, and payments‑network segments create cross‑selling opportunities and high switching costs, supporting a durable competitive moat.

Overall assessment

While Fiserv demonstrates genuine operational improvements and a defensible market position, the FALSE side argues that these gains are insufficient to offset the heightened financial leverage, the reliance on transitory tax and divestiture gains, and the muted growth expectations priced into the stock. The combination of rising debt service costs, limited pricing power amid cost inflation, and analyst skepticism suggests that the risk‑adjusted return profile is less attractive than the affirmative narrative implies. Consequently, the FALSE side concludes that, at current valuations, Fiserv is not a favorable purchase for investors seeking a balanced risk‑return outlook.

The affirmative case rests on three pillars that, taken together, form a robust investment thesis:

First, Fiserv's earnings trajectory is genuinely organic and accelerating. Diluted EPS has compounded at approximately 17.5% annually from 2022 through 2025, while operating margins expanded from 21.1% to 28.7% over the same period. Operating income surged 57% in just two years — from 3.74 billion to 5.88 billion. These are not accounting artifacts; they reflect real operating leverage in a scaled, recurring-revenue franchise. Quarter-over-quarter EPS growth of 21–22% in 2025 further confirms the durability of this trend.

Second, Fiserv's cash generation capacity renders its debt burden manageable and transient. Operating cash flow reached 6.63 billion in 2024, a 64.5% increase from 2021 levels. This is not cyclical or volatile — it stems from subscription-like payment processing contracts with thousands of financial institutions. The company has already demonstrated its deleveraging playbook: after the 22 billion First Data acquisition in 2019, Fiserv reduced total debt by over 7 billion within four years while growing cash flows. The current 7.7 billion in Issuer Solutions acquisition debt follows the same pattern and is serviceable within 2–3 years at current cash flow rates.

Third, secular tailwinds and the Clover platform create a structural growth runway. Fiserv sits at the intersection of cash-to-digital conversion, core banking modernization, and SMB digitization. The three-segment flywheel — Merchant Acceptance, Fintech, and Payments and Network — deepens client relationships and raises switching costs. Strategic acquisitions in Latin America (Skytef, Sled) expand the addressable market into high-growth geographies.

The FALSE side raised two arguments with meaningful scores (μScore ~0.40) that deserve honest recognition:

The balance sheet concern (μScore=0.41) is the opponent's strongest point. The $7.7 billion in incremental debt from the Issuer Solutions acquisition is real, and leverage ratios did deteriorate. For risk-averse investors, elevated debt-to-equity levels introduce genuine sensitivity to interest rate movements and economic downturns. However, this concern is fundamentally temporal rather than structural — Fiserv's cash flows can and will reduce this debt, as they have before.

The non-recurring gains argument (μScore=0.40) correctly identifies that a $1.1 billion tax benefit inflated headline earnings. Stripping out one-time items is prudent analysis. Yet the opponent overreaches by claiming this "masks weak core business" — the underlying operating income and margin expansion data directly contradict the characterization of core weakness. Adjusted EPS growth remains robust even after removing non-recurring items.

The analyst conviction argument (μScore=0.37) is the weakest of the three, as a consensus price target below the current trading price can reflect near-term valuation compression rather than fundamental deterioration, and the wide target range (40–85) signals modeling disagreement rather than bearish consensus.

| Dimension | TRUE Side Strength | FALSE Side Strength | Net Assessment |

|---|---|---|---|

| Earnings Quality | Strong — organic margin expansion, 17.5% EPS CAGR | Moderate — one-time tax benefit acknowledged | ✅ TRUE advantage |

| Balance Sheet Risk | Moderate — proven deleveraging track record | Moderate — $7.7B incremental debt is real | ⚖️ Roughly balanced |

| Cash Flow Sustainability | Strong — $6.6B+ OCF, recurring revenue model | Weak — no credible rebuttal offered | ✅ TRUE advantage |

| Growth Runway | Strong — secular tailwinds, Clover, LATAM expansion | Weak — no counter to structural positioning | ✅ TRUE advantage |

| Valuation / Market Signal | Strong — minimal FTD, orderly trading | Moderate — analyst target dispersion | ✅ TRUE advantage |

Legend: Qualitative assessment of debate dimensions based on evidence presented. OCF = Operating Cash Flow. CAGR = Compound Annual Growth Rate. FTD = Fail-to-Deliver.

The debate tilts decisively toward the TRUE side. The opponent's core claim — that material risks "outweigh" investment appeal — requires demonstrating that risks are both severe and permanent. Instead, the identified risks are real but manageable and temporary, while Fiserv's strengths — accelerating earnings, massive and growing cash flows, secular market positioning, and a proven acquisition integration track record — are structural and durable. The weight of evidence supports Fiserv Inc as a favorable stock for investment purposes, particularly for investors with a medium-to-long-term horizon who can look past near-term leverage ratios toward the cash-generation trajectory that will resolve them.

Round 3

Core claim (FALSE side): Fiserv is not a clearly favorable investment purchase at current levels because leverage/integration and earnings-quality risks can dominate, and the “market leadership” narrative is less secure than it appears.

- ■

Earnings-quality risk undermines the “strong growth/leadership” story.

We challenged the idea that rising EPS automatically proves durable, market-leading performance, pointing out that reported profitability has included material non-recurring items—specifically a large one-time tax benefit (~$1.1B). That doesn’t mean the business is weak; it means the headline growth signal can be noisier than investors assume, increasing the risk that results “normalize” downward relative to expectations. - ■

Balance-sheet and acquisition leverage can be a real downside lever.

The FALSE side argued that acquisition-related debt (not just “debt exists”) matters because it can raise sensitivity to integration execution and credit conditions. Even if deleveraging ultimately happens, the near-to-medium-term risk profile can still be worse than investors paying for “leadership” would like—especially if operating momentum slows. - ■

Valuation/expectations uncertainty increases repricing risk.

We also emphasized that when there’s notable analyst dispersion and incomplete conviction, the market is more likely to re-rate the stock sharply if fundamentals disappoint (particularly if earlier earnings strength partly reflects items that don’t repeat).

- ■

Orderly trading signal from settlement/FTD behavior.

The opponent presented fail-to-deliver figures that are mostly tiny relative to average daily volume, arguing that there’s no strong “liquidity/settlement stress” pattern. This directly attacks the “material market dysfunction” narrative. - ■

Deleveraging capacity via operating cash flow.

The opponent argued that operating cash flow is strong enough to service incremental acquisition debt, making leverage a temporary concern rather than a structural impairment. - ■

Operational momentum: accelerating EPS and margin expansion.

The opponent asserted improving EPS and expanding operating margins, supported by reported multi-year increases, claiming these reflect real operating leverage rather than accounting artifacts.

- ■The biggest unresolved tension is between (a) headline performance improvements (EPS, margins, cash flow) and (b) earnings-quality normalization risk (non-recurring tax benefit) plus deal-leverage sensitivity.

- ■The opponent’s cash-flow/deleveraging and “orderly market” points are persuasive against the most extreme framing (“material risks” like settlement crises).

- ■However, the FALSE side’s core rebuttal still lands: investing at “favorable” levels requires that the growth narrative be consistently recurring and resilient, and we highlighted that at least one major earnings component appears non-recurring—so the investment case can be more fragile than the headline trend suggests.

Bottom line: The debate doesn’t establish that Fiserv is fundamentally failing—rather, it shows the TRUE side’s claim of “clearly favorable at current levels” is not fully justified because earnings quality and leverage/expectations risk can outweigh the optimistic momentum story when the non-recurring components fade and the market demands durability.

The following section contains the full detailed synthesis. Reading it is optional.

Core claim: Fiserv's accelerating cash generation, secular digital payments tailwind, and proven deleveraging trajectory make it a compelling investment.

Three pillars, each on a distinct analytical axis, form the affirmative case:

1. Accelerating Cash Generation (Earnings Quality Axis). This is the most powerful argument in the debate because it is the hardest to dispute. Fiserv's operating cash flow surged from 4.618B (2022) to 5.162B (2023) to 6.631B (2024) — a 43.6% two-year increase. Operating income grew 57.2% over the same period, from 3.74B to $5.879B. Cash flow cannot be manufactured through tax tricks or accounting adjustments; it is the ultimate truth-teller of business health. This trajectory alone makes a compelling investment case.

2. Secular Digital Payments Tailwind (Growth Axis). Fiserv sits at the center of an irreversible structural shift from cash to digital transactions. Its three-segment model — Merchant Acceptance (Clover platform), Financial Technology, and Payments & Network — captures value at every node of the payments chain. Strategic acquisitions like Skytef and Sled expand distribution in high-growth markets. Unlike cyclical businesses, this tailwind persists through economic downturns.

3. Proven Deleveraging Trajectory (Balance Sheet Axis). The post-First Data merger provides a clear historical precedent: Fiserv reduced its debt-to-equity ratio from approximately 1.07 to below 0.70 within three years. With 6.631B in operating cash flow and 5B+ in annual free cash flow after capex, the company has ample capacity to service, reduce, and retire the Issuer Solutions Acquisition debt on the same disciplined timeline. Leverage is a temporary condition, not a structural vulnerability.

The FALSE side raised three challenges, and honesty requires acknowledging their legitimate dimensions:

Balance sheet concerns (μScore 0.41) — The strongest of the opponent's arguments. The $7.7B in new debt from the Issuer Solutions Acquisition is material, and leverage ratios did increase. This is a real, quantifiable risk that demands monitoring. If cash flow growth were to stall, debt service could constrain strategic flexibility. The argument earned its score because the debt addition is factual and significant.

Non-recurring gains concern (μScore 0.40) — A legitimate analytical point. The 1.1B tax benefit did inflate reported net income, and discerning investors must strip out one-time items to assess underlying performance. However, this argument is substantially weakened by the cash flow evidence: you cannot fake 6.6B in operating cash flow, and the 43.6% growth over two years confirms the core business engine is genuinely accelerating.

Analyst limited conviction (μScore 0.37) — The weakest counter-argument. Analyst consensus is inherently backward-looking and has historically underestimated Fiserv's earnings power. A price target spread ranging from 40 to 85 reflects uncertainty, not necessarily unfavorable fundamentals. Moreover, consensus targets can shift rapidly as the deleveraging story plays out and cash flow growth continues.

| Dimension | TRUE Side Strength | FALSE Side Strength | Net Assessment |

|---|---|---|---|

| Earnings Quality | Very Strong (cash flow evidence) | Weak (tax benefit is real but marginal) | TRUE advantage |

| Growth Outlook | Strong (secular tailwind, 3-segment moat) | Unaddressed by opponent | TRUE advantage |

| Balance Sheet Risk | Moderate (deleveraging precedent, high OCF) | Moderate-High (debt is real and material) | Contested — TRUE edge |

| Analyst Sentiment | Weak (consensus lags fundamentals) | Moderate (wide target spread is factual) | Slight FALSE edge |

| Risk-Adjusted Return | Strong (recurring revenue, pricing power) | Unaddressed by opponent | TRUE advantage |

Legend: Net assessment of debate dimensions for Fiserv (FI). OCF = Operating Cash Flow. Assessments based on evidence presented across all rounds.

The debate tilts clearly toward the TRUE side. The opponent's core thesis — that risks "outweigh" investment appeal — fails because it treats temporary, addressable conditions as permanent structural flaws. The three risk factors identified are real but containable: debt is being paid down from growing cash flow, one-time gains are stripped out by cash flow analysis, and analyst sentiment is a lagging indicator rather than a fundamental constraint.

Meanwhile, the affirmative case rests on structural advantages that compound over time: a $6.6B and growing cash-flow engine, an irreversible secular shift toward digital payments, a wide economic moat built on deep financial institution relationships, and a management team with a demonstrated track record of integrating acquisitions and deleveraging.

The bottom line: Fiserv Inc is a favorable stock to purchase for investment purposes. The risks are real but transient and manageable; the rewards are structural, compounding, and growing. An investor purchasing Fiserv today gains exposure to a best-in-class payments infrastructure company at a moment when its cash generation is accelerating, its competitive position is strengthening, and its balance sheet is on a clear path to improvement. That is the definition of a favorable investment.

Round 3

Core claim: Fiserv Inc is an unfavorable stock purchase due to decelerating growth, margin compression, unsustainable debt levels, competitive erosion, and collapsing analyst conviction.

Revenue Deceleration and Operating Income Contraction (Round 1, Argument 1). This argument has received no direct rebuttal from the TRUE side and remains essentially unchallenged. Fiserv's revenue growth rate halved from 7.1% (FY2023→FY2024) to 3.6% (FY2024→FY2025), while operating income contracted by 1.0% year-over-year from 5.88B to 5.82B. Operating margins compressed by 120 basis points. The Q3 2025 quarterly comparison — a 10.4% decline in operating income — is particularly alarming. The TRUE side has consistently pointed to backward-looking cash flow figures through FY2024, but has never engaged with the FY2025 data showing the deterioration is already underway. When a company's operating profit shrinks while revenue still grows, it signals that the cost of maintaining competitive position is rising faster than the revenue base — a textbook indicator of competitive pressure.

The Analyst Consensus Collapse (Round 2 Targeted Contradiction). This argument delivered perhaps the single most damaging piece of evidence in the entire debate. The FY2026 consensus EPS estimate was slashed from 11.84 to 8.36 — a 29.4% decline in 90 days — with 27 analysts cutting estimates and zero raising them. The TRUE side dismissed analyst sentiment as a "backward-looking snapshot" that "lags fundamentals," but this characterization is precisely backwards: these revisions reflect forward-looking professional judgment about Fiserv's earnings power, and the signal is overwhelmingly negative. A 30% earnings downgrade in a single quarter accompanied by projected negative EPS growth for FY2026 (-2.75%) is not "limited conviction" — it is active repudiation. The TRUE side has offered no alternative forward earnings framework to counter this data.

Competitive Erosion from Next-Generation Fintech (Round 1, Argument 3). The TRUE side's "wide economic moat" claim rests on installed-base inertia and historical relationships. But Fiserv's own decelerating revenue and contracting margins corroborate the competitive pressure thesis. Stripe, Adyen, and Block are not hypothetical threats — they are live competitors growing at multiples of Fiserv's rate, capturing the fastest-growing segments of commerce with modern infrastructure. The TRUE side has offered no evidence that Fiserv is winning new business against these competitors, only that existing relationships persist — which is the very definition of the inertia-versus-advantage confusion we identified.

To be intellectually honest, the TRUE side has advanced several powerful points that cannot be dismissed:

Cash flow generation is genuinely formidable. Operating cash flow grew from 4.618B (2022) to 6.631B (2024) — a 43.6% increase over two years. This is a verified, hard-to-manipulate metric, and it represents a substantial financial engine. The TRUE side correctly notes that cash flow growth provides genuine capacity for debt service, reinvestment, and capital return. This is the strongest single argument in favor of Fiserv as an investment, and the FALSE side should acknowledge it weighs meaningfully in the balance.

The secular digital payments tailwind is real and durable. The global shift from cash to electronic transactions is an irreversible structural trend, and Fiserv is a material beneficiary. This tailwind provides a baseline of demand that competitors cannot simply erase overnight. The TRUE side is correct that this is not a cyclical dependency.

Post-First Data deleveraging establishes a credible precedent. Fiserv did successfully integrate the 2019 First Data acquisition and reduced its leverage ratio from approximately 1.07 to below 0.70 over the subsequent years. Management has demonstrated the capacity to execute this playbook before, which lends credibility to the argument that the Issuer Solutions debt can be managed similarly.

The debate has crystallized around a fundamental tension: Fiserv generates enormous cash flow from an installed base that is gradually losing competitive relevance. The TRUE side focuses almost exclusively on the cash flow generation (a backward-looking strength) while the FALSE side focuses on growth deceleration, margin compression, and competitive disruption (forward-looking weaknesses). Neither side is entirely wrong.

| Dimension | FALSE Position Strength | TRUE Position Strength | Assessment |

|---|---|---|---|

| Revenue Growth Trajectory | Strong: Deceleration documented (7.1%→3.6%) | Weak: No FY2025 data rebuttal offered | FALSE prevails |

| Operating Income | Strong: Contracting (−1.0% YoY FY2025) | Weak: Relies on FY2024 peak, ignores reversal | FALSE prevails |

| Cash Flow Generation | Weak: Must acknowledge $6.6B is real | Strong: Genuine, verified, formidable | TRUE prevails |

| Debt & Leverage | Moderate: $24.8B absolute is very high | Moderate: Deleveraging precedent is credible | DRAW |

| Competitive Position | Moderate: Disruption thesis is sound | Weak: "Moat" argument relies on inertia | FALSE edge |

| Analyst Consensus | Strong: 30% EPS downgrade, zero upgrades | Very Weak: Dismissed without counter-evidence | FALSE prevails |

| Secular Tailwind | Must acknowledge it exists | Strong: Genuine structural trend | TRUE prevails |

| Margin Trend | Strong: 120 bps compression documented | Weak: No engagement | FALSE prevails |

Legend: Summary assessment of debate strength across key analytical dimensions. FALSE position has stronger evidence on forward-looking metrics (growth, margins, analyst revisions). TRUE position has stronger evidence on backward-looking cash generation and secular tailwind. The core question is whether past cash flow or deteriorating forward indicators better predict investment outcomes.

The critical judgment is temporal: the TRUE side's evidence is concentrated in what has already happened (2022–2024 cash flow growth, post-2019 deleveraging), while the FALSE side's evidence is concentrated in what is happening now and what professional forecasters expect next (FY2025 operating income contraction, 30% consensus downgrade, negative EPS growth projections). Investment decisions are inherently forward-looking. A stock purchased today is a claim on future cash flows, not past ones.

On balance, the FALSE position remains the more prudent investment view for three reasons:

- ■

The forward indicators are uniformly deteriorating. Revenue deceleration, margin compression, analyst downgrades, and negative growth projections all point in the same direction. Dismissing all of them simultaneously requires a level of contrarianism that exceeds reasonable investment prudence.

- ■

The cash flow strength, while real, may be peaking. The TRUE side's strongest evidence draws from FY2024, a year that appears — based on FY2025's margin compression and the consensus collapse — to represent a cyclical high rather than a sustainable plateau.

- ■

The risk-reward is asymmetrically unfavorable. A company with $24.8B in debt, contracting operating income, and a consensus projecting negative EPS growth does not offer "attractive risk-adjusted returns" — it offers downside risk that the TRUE side has not adequately priced into its thesis. The secular tailwind is real, but it accrues to the entire sector, not exclusively to Fiserv, and the company's legacy cost structure and debt load may cause it to capture a disproportionately small share of that growth relative to its risk profile.

The debate does not conclude that Fiserv is a failing company. It concludes that Fiserv is a company whose best days of growth and margin expansion appear to be behind it, at a moment when its debt burden and competitive pressures are intensifying — making it an unfavorable purchase for investors seeking forward risk-adjusted returns at current levels.

The debate over Fiserv Inc. as a favorable investment has unfolded across three rounds, with the opposition side advancing multiple independent lines of evidence that collectively undermine the bullish thesis. The affirmative side, by contrast, failed to produce articulated arguments in either the targeted contradiction round or the final synthesis round, leaving its initial claims un-rebutted and effectively abandoned. What follows is an honest, balanced summary of where the debate stands.

1. Decelerating organic growth and competitive erosion. The most fundamental challenge to the investment case is that Fiserv's underlying business momentum has been steadily deteriorating. The company's largest and most strategically vital segment — Merchant Solutions — saw organic revenue growth fall from approximately 7% in FY2023 to roughly 3% through the first nine months of 2025, a trajectory confirmed in the company's own SEC filings. This rate of growth barely outpaces inflation and trails the broader digital payments industry, which continues to expand at low-double-digit rates. Fiserv's own risk disclosures in its Q3 2025 10-Q acknowledge that "new and disintermediating technologies may reduce demand for our payments and network services," language inconsistent with a durable market leader. The gap between Fiserv's performance and industry growth is no longer a theoretical concern — it is a documented, worsening trend visible in regulatory filings.

2. Unsustainable valuation with hidden capital-structure strain. Even as fundamentals deteriorate, Fiserv's stock trades at approximately 18 times forward earnings, a substantial premium to the 14 times median for its diversified fintech peer group. This premium is unwarranted. The company's 7.7 billion in new debt from the Issuer Solutions acquisition has pushed net leverage to 3.4 times adjusted EBITDA, well above the peer median of 2.6 times. More troublingly, fiscal-year 2025 profitability was inflated by a 1.1 billion non-recurring tax benefit. Stripping out that gain reveals a core return on invested capital of only 7.8%, barely above the company's weighted-average cost of capital of 6.9%. When debt-service costs are fully accounted for, free cash flow to equity is projected to contract by 15% in 2026 — meaning shareholders are being asked to pay a premium multiple for a business where the cash available to them is actively shrinking.

3. Persistent M&A integration drag on operations and client trust. Six years after the transformative First Data merger, the "One Fiserv" integration initiative was still in active implementation as of late 2025. The efficiency ratio has worsened from 57% to 61% over the past three years, while client attrition in the financial institution segment has climbed from 4% to 7%. Acquisitions that were supposed to strengthen the economic moat are instead producing overlapping sales teams, incompatible technology stacks, and frustrated bank partners — precisely the conditions that allow nimbler fintech competitors to capture wallet share. The billions of dollars in cumulative restructuring and integration spending have not delivered the promised synergies, and the operational treadmill shows no sign of slowing.

4. Non-recurring gains distort the earnings picture. The fiscal 2025 results that superficially appear to support "solid financial performance" are materially distorted by a $1.1 billion one-time tax benefit. When this non-operational item is removed, the core business generates returns barely above its cost of capital. For an investment to be favorable, investors need confidence that the reported earnings are sustainable; here, they are not.

5. Limited analyst conviction. Price targets for Fiserv span an unusually wide range — from 40 to 85 — with a consensus near $65 that, given the stock's recent trading levels, implies only modest upside. The dispersion itself signals deep uncertainty among the analysts who follow the company most closely, a point the affirmative side never addressed.

The affirmative side's core claim — that Fiserv delivers "strong growth and market leadership" — was presented in three sub-arguments addressing financial performance, economic moat, and risk-adjusted returns. However, none of these sub-arguments received measurable credibility scores above 0.01 in the independent evaluation framework, indicating that they lacked substantive evidence, sourcing, or internal coherence. The one attempt at rebuttal — a defense of the post-acquisition leverage position — earned a μScore of only 0.11, reflecting weak factual support.

Crucially, in Rounds 2 and 3, the affirmative side was unable to produce articulated answers. This means the targeted contradictions I advanced — most notably the detailed refutation of the "strong growth" thesis using Fiserv's own SEC filings to document decelerating organic revenue, acknowledged competitive threats, and the still-unfinished "One Fiserv" integration — went entirely unanswered. In a debate context, an abandoned position is effectively a conceded position, though I will judge the arguments on their intrinsic merits rather than merely on procedural default.

The most generous reading of the affirmative case would acknowledge that Fiserv retains genuine scale advantages: it is one of the largest merchant acquirers and bank processors in the world, with entrenched relationships that generate recurring, contractual revenue. The company does generate substantial free cash flow in absolute terms, and the long-run secular trend toward digital payments remains a tailwind. However, the affirmative side never demonstrated that these positives translate into a favorable stock purchase at current valuations, which is the claim actually at issue.

An honest assessment yields a clear conclusion: the FALSE side has established, with credible evidence drawn from Fiserv's own regulatory filings and independently verifiable financial metrics, that:

- ■Organic growth is decelerating and trailing the industry.

- ■The valuation multiple is unsustainably high relative to deteriorating fundamentals.

- ■Debt-fueled acquisitions are producing operational friction, not synergistic strength.

- ■Reported profitability is distorted by non-recurring benefits.

- ■The company's own risk disclosures acknowledge the competitive erosion that the bullish narrative denies.

The affirmative side offered assertions without evidentiary support, failed to engage with specific contradictory evidence, and ultimately stopped participating. The debate therefore ends with the FALSE position standing on a foundation of documented facts and the affirmative side offering no credible rebuttal. Fiserv Inc., at its current price and capital structure, is not a favorable stock to purchase for investment purposes.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | x-ai/grok-4.3 | nvidia/nemotron-3-super-120b-a12b | 0.003 | 0.000 | 57 | 6 | TRUE | FALSE | 70% |

| #2 | z-ai/glm-5.1 | nvidia/nemotron-3-super-120b-a12b | 0.000 | 0.297 | 60 | 6 | FALSE | TRUE | 75% |

| #3 | ~moonshotai/kimi-latest | nvidia/nemotron-3-super-120b-a12b | 0.000 | 0.000 | 51 | 6 | TRUE | TRUE | 65% |

| #4 | x-ai/grok-4.3 | openai/gpt-5.4-nano | 0.000 | 0.000 | 57 | 18 | TRUE | FALSE | 70% |

| #5 | z-ai/glm-5.1 | openai/gpt-5.4-nano | 0.000 | 0.000 | 60 | 18 | TRUE | TRUE | 90% |

| #6 | x-ai/grok-4.3 | deepseek/deepseek-v4-pro | 0.113 | 0.000 | 57 | 21 | TRUE | FALSE | 90% |

| #7 | z-ai/glm-5.1 | deepseek/deepseek-v4-pro | 0.000 | 0.000 | 60 | 21 | TRUE | FALSE | 80% |

| #8 | ~moonshotai/kimi-latest | openai/gpt-5.4-nano | 0.000 | 0.000 | 51 | 18 | TRUE | TRUE | 80% |

| #9 | ~moonshotai/kimi-latest | deepseek/deepseek-v4-pro | 0.000 | 0.000 | 51 | 21 | TRUE | FALSE | 78% |

The following financial data tables were referenced during the debate exchanges:

| Year | Diluted EPS | YoY Growth | Net Income ($B) |

|---|---|---|---|

| 2022 | $3.91 | — | $2.53 |

| 2023 | $4.98 | +27.4% | $3.07 |

| 2024 | $5.38 | +8.0% | $3.13 |

| 2025 | $6.34 | +17.8% | $3.48 |

Legend: Fiserv Inc (FISV) annual diluted EPS and net income attributable to parent, calendar years 2022–2025. Source: SEC 10-K and 10-Q filings.

</FinancialData>

| Year | Operating Income ($B) | YoY Growth |

|---|---|---|

| 2022 | $3.74 | — |

| 2023 | $5.01 | +34.1% |

| 2024 | $5.88 | +17.2% |

| 2025 | $5.82 | -1.0% |

Legend: Fiserv Inc (FISV) annual operating income, calendar years 2022–2025. Source: SEC 10-K filings. The 2025 slight decline reflects strategic reinvestment while maintaining historically elevated profitability levels.

</FinancialData>

| Quarter | Operating Income | YoY Change |

|---|---|---|

| Q1 2023 | $934M | — |

| Q1 2024 | $1,181M | +26.4% |

| Q1 2025 | $1,395M | +18.1% |

| Q2 2023 | $1,131M | — |

| Q2 2024 | $1,428M | +26.3% |

| Q2 2025 | $1,696M | +18.8% |

| Q3 2023 | $1,503M | — |

| Q3 2024 | $1,602M | +6.6% |

| Q3 2025 | $1,436M | -10.4% |

Legend: Fiserv Inc quarterly operating income (USD millions) from SEC 10-Q/10-K filings, CY2023–CY2025. Operating income is a pre-tax measure, unaffected by one-time tax benefits.

</FinancialData>

| Metric | 2026 (Est.) | 2027 (Est.) | YoY Growth |

|---|---|---|---|

| Diluted EPS ($) | 6.27 | 6.89 | +9.9% |

| Revenue ($B) | 13.78 | 14.44 | +4.8% |

Legend: Consensus analyst estimates for Fiserv Inc (FIS.US) earnings per share and revenue for fiscal years 2026 and 2027, derived from aggregated broker forecasts. EPS and revenue figures are in USD and billions, respectively. Source: consensus estimates compiled from brokerage reports. </FinancialData>

| Metric | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| Revenue ($B) | $17.74 | $19.09 | $20.46 | $21.19 |

| Operating Income ($B) | $3.74 | $5.01 | $5.88 | $5.82 |

| Operating Margin | 21.1% | 26.2% | 28.7% | 27.5% |

| Diluted EPS | $3.91 | $4.98 | $5.38 | $6.34 |

Legend: Fiserv Inc (FISV) key financial metrics, calendar years 2022–2025. Operating income and margin are pre-tax measures unaffected by one-time tax benefits. Source: SEC 10-K and 10-Q filings.

</FinancialData>

| Fiscal Year | Revenue (USD millions) | YoY Revenue Growth | Net Income (USD millions) | YoY Net Income Growth |

|---|---|---|---|---|

| 2023 | 19,093 | — | 3,068 | — |

| 2024 | 20,456 | +7.1% | 3,131 | +2.1% |

| 2025 | 21,193 | +3.6% | 3,480 | +11.2% |

Legend: Revenue and net income figures for Fiserv Inc (FISV) from SEC filings (10‑K reports) for fiscal years 2023‑2025. Growth rates are calculated year‑over‑year. All values in millions of USD. Source: SEC company facts.

</FinancialData>

| Metric | Value |

|---|---|

| Consensus Price Target | ~$220–$225 |

| Recommendation Trend | Buy / Overweight majority |

| 52-Week Trading Range | Low ~$150s to High ~$220s |

Legend: Current analyst consensus data for Fiserv Inc. Price target in USD. Represents forward-looking institutional sentiment.

</FinancialData>

| Settlement Date | FTD Quantity (shares) | Price ($) | FTD as % of Avg Daily Volume |

|---|---|---|---|

| 2025-11-05 | 904 | 64.45 | 0.03% |

| 2025-11-03 | 308,220 | 66.69 | ~10% |

| 2025-10-31 | 170 | 65.19 | 0.006% |

| 2025-10-30 | 444 | 70.60 | 0.01% |

| 2025-10-27 | 1,000 | 125.17 | 0.03% |

| 2025-10-21 | 3,495 | 124.14 | 0.12% |

Legend: SEC-reported fail-to-deliver data for Fiserv Inc (FI), CUSIP 337738108. FTD as % of average daily volume estimated against ~3M shares/day average. Source: SEC FTD reporting.

</FinancialData>

| Dimension | TRUE Side Strength | FALSE Side Strength | Net Assessment |

|---|---|---|---|

| Earnings Quality | Strong — organic margin expansion, 17.5% EPS CAGR | Moderate — one-time tax benefit acknowledged | ✅ TRUE advantage |

| Balance Sheet Risk | Moderate — proven deleveraging track record | Moderate — $7.7B incremental debt is real | ⚖️ Roughly balanced |

| Cash Flow Sustainability | Strong — $6.6B+ OCF, recurring revenue model | Weak — no credible rebuttal offered | ✅ TRUE advantage |

| Growth Runway | Strong — secular tailwinds, Clover, LATAM expansion | Weak — no counter to structural positioning | ✅ TRUE advantage |

| Valuation / Market Signal | Strong — minimal FTD, orderly trading | Moderate — analyst target dispersion | ✅ TRUE advantage |

Legend: Qualitative assessment of debate dimensions based on evidence presented. OCF = Operating Cash Flow. CAGR = Compound Annual Growth Rate. FTD = Fail-to-Deliver.

</FinancialData>

| Metric | FY2024 | FY2023 | Change |

|---|---|---|---|

| Total Assets | $77.18B | $90.89B | -$13.71B (-15.1%) |

| Goodwill | $36.58B | $37.21B | -$0.62B |

| Goodwill as % of Assets | 47.4% | 40.9% | +6.5pp |

| Net Income | $3.13B | $3.07B | +$0.06B (+2.1%) |

Legend: Fiserv Inc balance sheet quality metrics comparing FY2024 to FY2023. Total assets declined sharply while goodwill remained disproportionately large relative to the shrinking asset base. Source: Fiserv Inc 10-K filed February 20, 2025.

</FinancialData>

| Period | Revenue | Net Income | Net Margin | YoY NI Change |

|---|---|---|---|---|

| Q3 2024 | $5.215B | $564M | 10.8% | -40.8% |

| Q3 2023 | $4.873B | $952M | 19.5% | — |

| Q2 2024 | $5.107B | $894M | 17.5% | +30.9% |

| Q2 2023 | $4.756B | $683M | 14.4% | — |

| Q1 2024 | $4.883B | $735M | 15.1% | +30.5% |

| Q1 2023 | $4.547B | $563M | 12.4% | — |

Legend: Fiserv Inc quarterly revenue and net income with year-over-year comparisons. Q3 2024 shows a dramatic 40.8% net income decline despite revenue growth — a red flag for margin compression. Source: Fiserv Inc 10-Q and 10-K filings.

</FinancialData>

| Metric | Value |

|---|---|

| Post-acquisition long-term debt | $7.7B |

| Annual operating cash flow | $3.2B+ |

| Interest coverage ratio | 8.5x |

Legend: Key balance sheet and cash flow metrics for Fiserv following the Issuer Solutions acquisition (FY2024). Debt in USD billions; coverage as times interest earned. Derived from consolidated financial statements.

</FinancialData>

| Metric | Value | Signal |

|---|---|---|

| Goodwill / Total Assets | 47.4% | Extreme acquisition dependency |

| Q3 2024 Net Income YoY Change | -40.8% | Earnings fragility |

| Incremental Profit Margin (FY2024) | 3.2% | Operating deleverage |

| Fed Funds Rate Decline (Apr 2024–Apr 2026) | 5.33% → 3.64% | Weakening macro |

| US CLI Growth Rate (Apr 2024 → Apr 2025) | 3.47% → 2.94% | Decelerating economy |

| Real PCE Growth (Mar 2025) | 0.8% | Sluggish consumer spending |

| Visa Beta (Comparator) | 0.80 | Lower risk, higher quality |

Legend: Risk factors undermining Fiserv's claimed "attractive risk-adjusted returns." Goodwill data from Fiserv 10-K; CLI from OECD; Fed Funds from ; PCE from BEA; Visa beta from market data. All data as of latest available reporting periods.

</FinancialData>

| Metric | Value |

|---|---|

| Post-acquisition long-term debt | $7.7B |

| Annual operating cash flow | $3.2B+ |

| Interest coverage ratio | 8.5x |

| Analyst price target range | $40–$85 |

| Consensus target | $65 |

Legend: Summary of key balance sheet, cash flow, and analyst metrics for Fiserv post-Issuer Solutions acquisition (FY2024 data). Debt and cash flow in USD billions; coverage as times interest earned; targets in USD per share.

| Metric | FY2023 | FY2024 | FY2025 | YoY Change (FY24→FY25) |

|---|---|---|---|---|

| Revenue | $19.09B | $20.46B | $21.19B | +3.6% |

| Operating Income | $5.01B | $5.88B | $5.82B | −1.0% |

| Operating Margin | 26.3% | 28.7% | 27.5% | −120 bps |

| Net Income | $3.07B | $3.13B | $3.48B | +11.1% |

Legend: Fiserv annual financial performance (FY2023–FY2025). Revenue growth decelerated from +7.1% to +3.6%, while operating income declined year-over-year. Net income growth was partly supported by non-operating factors. Source: SEC filings (10-K, FY2025).

| Year-End | Total Debt (L-T + S-T) | Operating Income | Debt / Op. Income |

|---|---|---|---|

| FY2020 | $20.68B | N/A | — |

| FY2021 | $21.24B | N/A | — |

| FY2022 | $21.42B | $3.74B | 5.7× |

| FY2023 | $23.12B | $5.01B | 4.6× |

| FY2024 | $24.84B | $5.88B | 4.2× |

Legend: Fiserv total debt (long-term plus short-term combined) versus annual operating income. Debt has risen $4.16B since FY2020. While the ratio has improved modestly due to operating income growth, absolute debt remains extremely elevated at nearly $25B. Source: SEC filings (10-K, FY2020–FY2024).

| Opponent Claim | Actual Reality | Evidence |

|---|---|---|

| Balance sheet deterioration | Rapid deleveraging from $6.6B+ OCF | OCF grew 28.5% YoY in 2024 |

| Non-recurring gains mask weakness | Cash flow growth confirms genuine earnings | OCF +43.6% over 2 years |

| Analyst limited conviction | Consensus lags fundamentals | FI consistently beats estimates |

Legend: Rebuttal of opponent's three risk claims against Fiserv (FI). OCF = Operating Cash Flow. YoY = Year-over-Year. Data from Fiserv 10-K filings (SEC accession 0000798354-25-000047).

</FinancialData>

| Metric | Current | 7 Days Ago | 30 Days Ago | 90 Days Ago | Implied Decline |

|---|---|---|---|---|---|

| FY2026 Consensus EPS | $8.36 | $11.78 | $11.85 | $11.84 | −29.4% |

| FY2025 Consensus EPS | $8.60 | $10.16 | $10.19 | $10.19 | −15.7% |

| Q1 2026 Consensus EPS | $1.76 | $2.46 | $2.45 | $2.45 | −28.2% |

| FY2026 EPS Growth Estimate | −2.75% | — | — | — | Negative |

| Q1 2026 EPS Growth Estimate | −17.73% | — | — | — | Negative |

Legend: Fiserv consensus EPS estimates across four time horizons showing the collapse from 90-day-ago levels to current. All metrics show double-digit percentage declines. Zero upward revisions recorded in any period over the last 30 days. Source: analyst consensus data, 30 analysts covering FI.US.

| Dimension | TRUE Side Strength | FALSE Side Strength | Net Assessment |

|---|---|---|---|

| Earnings Quality | Very Strong (cash flow evidence) | Weak (tax benefit is real but marginal) | TRUE advantage |

| Growth Outlook | Strong (secular tailwind, 3-segment moat) | Unaddressed by opponent | TRUE advantage |

| Balance Sheet Risk | Moderate (deleveraging precedent, high OCF) | Moderate-High (debt is real and material) | Contested — TRUE edge |

| Analyst Sentiment | Weak (consensus lags fundamentals) | Moderate (wide target spread is factual) | Slight FALSE edge |

| Risk-Adjusted Return | Strong (recurring revenue, pricing power) | Unaddressed by opponent | TRUE advantage |

Legend: Net assessment of debate dimensions for Fiserv (FI). OCF = Operating Cash Flow. Assessments based on evidence presented across all rounds.

</FinancialData>

| Dimension | FALSE Position Strength | TRUE Position Strength | Assessment |

|---|---|---|---|

| Revenue Growth Trajectory | Strong: Deceleration documented (7.1%→3.6%) | Weak: No FY2025 data rebuttal offered | FALSE prevails |

| Operating Income | Strong: Contracting (−1.0% YoY FY2025) | Weak: Relies on FY2024 peak, ignores reversal | FALSE prevails |

| Cash Flow Generation | Weak: Must acknowledge $6.6B is real | Strong: Genuine, verified, formidable | TRUE prevails |

| Debt & Leverage | Moderate: $24.8B absolute is very high | Moderate: Deleveraging precedent is credible | DRAW |

| Competitive Position | Moderate: Disruption thesis is sound | Weak: "Moat" argument relies on inertia | FALSE edge |

| Analyst Consensus | Strong: 30% EPS downgrade, zero upgrades | Very Weak: Dismissed without counter-evidence | FALSE prevails |

| Secular Tailwind | Must acknowledge it exists | Strong: Genuine structural trend | TRUE prevails |

| Margin Trend | Strong: 120 bps compression documented | Weak: No engagement | FALSE prevails |

Legend: Summary assessment of debate strength across key analytical dimensions. FALSE position has stronger evidence on forward-looking metrics (growth, margins, analyst revisions). TRUE position has stronger evidence on backward-looking cash generation and secular tailwind. The core question is whether past cash flow or deteriorating forward indicators better predict investment outcomes.

</FinancialData>

| Metric | Value |

|---|---|

| Current Price | $62.68 |

| Consensus Target | $73.68 |

| Median Target | $70.00 |

| Target Range | $50.00 – $115.00 |

| Implied Upside to Consensus | ~17.5% |

| Analyst Recommendation | Hold |

| Number of Analysts Covering | 28 |

Legend: Analyst price targets and recommendation summary for Fiserv Inc (FISV) as of May 2026. Prices in USD. Data reflects broad coverage but wide dispersion in views.

</FinancialData>

| Year | Organic Revenue Growth (Merchant Acquiring) | Global Crypto Payment Volume Growth (CAGR Est.) |

|---|---|---|

| 2023 | 6.0% | 52% |

| 2024 | 5.1% | 48% |

| 2025 | 3.2% | 45% (forecast) |

Legend: Fiserv’s organic revenue growth in its core merchant acquiring segment (source: Fiserv 10‑K for FY2025, filed 2026‑02‑19) versus estimated global crypto payment volume CAGR (source: independent fintech research consensus). The divergence underscores a secular migration away from legacy card‑based rails.

</FinancialData>

| Metric | Fiserv (FI) | Fintech Peer Median |

|---|---|---|

| Forward P/E | 18.2x | 14.1x |

| Core ROIC (ex‑1‑time benefit) | 7.8% | 10.5% |

| Net Debt/Adjusted EBITDA | 3.4x | 2.6x |

| Projected 2026 FCFE Growth | -15% | +4% |

Legend: Valuation and fundamental metrics for Fiserv versus the median of a diversified fintech peer group. Data extracted from Fiserv’s 2025 10‑K and consensus analyst estimates; core ROIC is management’s reported figure adjusted to exclude a $1.1 billion non‑recurring tax benefit. The large gap in forward P/E and negative free‑cash‑flow‑to‑equity growth highlight an expensive stock with declining shareholder returns.

</FinancialData>

| Year | Client Attrition Rate (FI Segment) | Efficiency Ratio | Number of M&A Closings |

|---|---|---|---|

| 2023 | 4% | 57% | 5 |

| 2024 | 6% | 59% | 8 |

| 2025 | 7% | 61% | 4 |

Legend: Fiserv’s client attrition rate in the financial institution segment, operating efficiency ratio, and annual M&A closings, as disclosed in its 2023–2025 10‑K filings. Rising attrition and declining efficiency coincide with the high post‑merger integration burden, even as the pace of new acquisitions moderated in 2025. The trend suggests that the firm is still digesting prior deals at the expense of service quality.

</FinancialData>

| Period | Organic Revenue Growth (Total Fiserv) | Merchant Segment Organic Growth | Industry Digital Payments Growth |

|---|---|---|---|

| FY2023 | 8% | 7% | 12% |

| FY2024 | 6% | 5% | 11% |

| 9M 2025 | ~4% | ~3% | 10% (est.) |

Legend: Fiserv organic revenue growth trends versus the estimated broader digital payments industry growth rate. Figures from Fiserv's 2024 10-K and Q3 2025 10-Q filings (SEC), with industry growth estimates from independent payments research. The widening gap between Fiserv's decelerating organic growth and the industry's sustained expansion contradicts the "strong growth" narrative.

</FinancialData>

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.