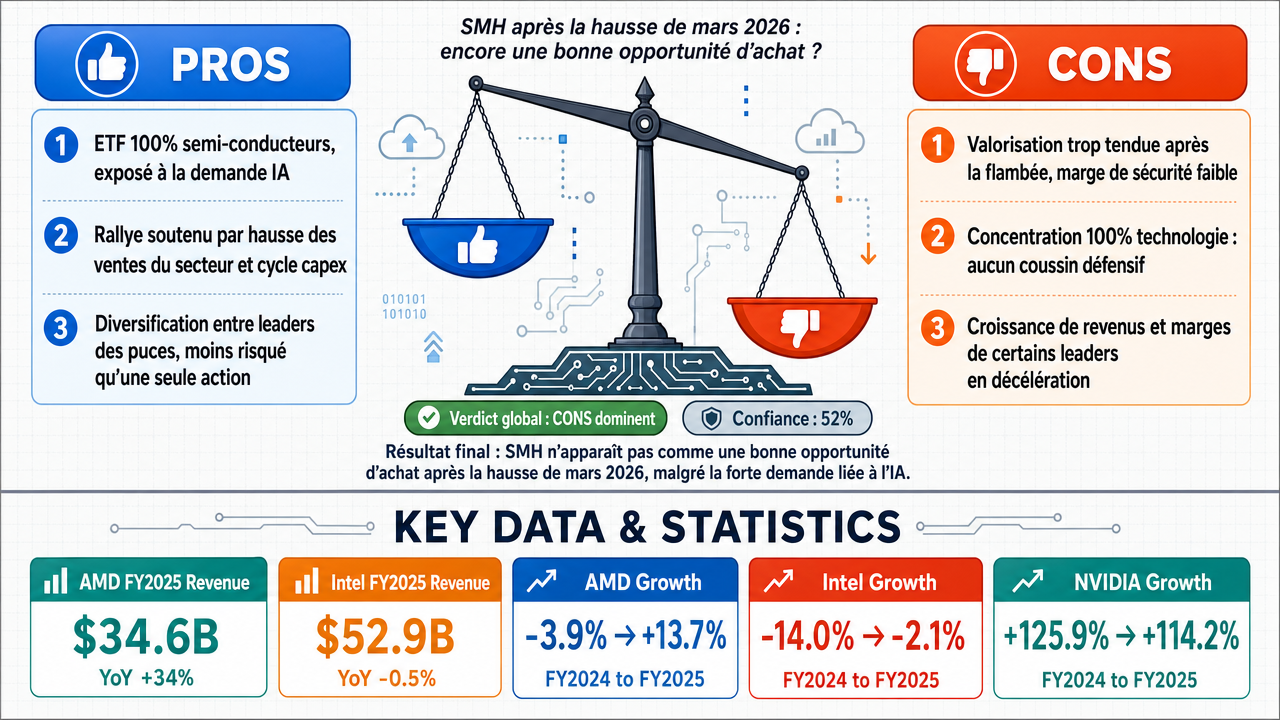

Is semiconductor ETF SMH yet a good buy opportunity in spite of the surge since March 2026 ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 4, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 52%

Web Report: https://solsice.com/public/debates/is-semiconductor-etf-smh-yet-a-good-buy-opportunity-in-spite-a12ecda3ea57

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■SMH is a pure-play semiconductor ETF with 100% Technology exposure, leveraged to secular AI demand, and the rally is supported by earnings growth among top holdings like NVIDIA, TSMC, and Broadcom.

- ■The post-March rally reflects a repricing of semiconductor leadership during an expanding AI and chip-capex cycle, with industry sales rising and forecasts pointing to continued growth.

- ■SMH offers diversification across multiple semiconductor leaders, reducing single-stock risk compared to owning individual chip companies.

❌ Key ANTI arguments:

- ■Valuation is overextended: NVIDIA's stock price has appreciated faster than its earnings, and Intel posted a net loss, leaving no margin of safety after the surge.

- ■100% Technology sector concentration is a structural flaw, not a feature; it provides no defensive ballast when the semiconductor cycle turns, and historical drawdowns are 1.5–2× deeper than broader tech indexes.

- ■Revenue growth for key SMH holdings is decelerating (e.g., NVIDIA from +114% to +65.5% YoY), and gross margins are projected to compress, undermining the earnings case.

💭 Conclusion: The tournament's confidence-weighted result narrowly favors the FALSE side, indicating that SMH is not a good buy opportunity after the March 2026 surge. Pro arguments highlighted strong fundamental demand from AI and solid earnings growth among top holdings, but anti arguments convincingly showed that valuations have become stretched and that the 100% sector concentration magnifies downside risk. The raw vote tie (2-2) underscores the closeness of the debate, but the marginally higher confidence in FALSE arguments (52% tournament confidence) tips the scale. Key facts such as decelerating revenue growth for major constituents and historically overbought technical conditions support the bearish case. Therefore, the opportunity to buy at current levels is not favorable, given the elevated risk of a cyclical downturn or correction.

🔬 DeepResearch Result: FALSE ❌ (52% confidence)

Assertion: Is semiconductor ETF SMH yet a good buy opportunity in spite of the surge since March 2026 ?

📊 Tournament: 2 voted TRUE, 2 voted FALSE (4 debates played, 5 models)

📊 Weighted scores: TRUE=1.45, FALSE=1.55

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -6

✅ PRO Arguments:

- ■SMH is a pure-play semiconductor ETF with 100% Technology exposure, leveraged to secular AI demand, and the rally is supported by earnings growth among top holdings like NVIDIA, TSMC, and Broadcom. [openai/gpt-5.4-mini]

- ■The post-March rally reflects a repricing of semiconductor leadership during an expanding AI and chip-capex cycle, with industry sales rising and forecasts pointing to continued growth. [openai/gpt-5.5]

- ■SMH offers diversification across multiple semiconductor leaders, reducing single-stock risk compared to owning individual chip companies. [openai/gpt-5.4-mini]

- ■Options market data shows that even after the rally, the 30-day call value at a $520 strike indicates meaningful upside potential. [openai/gpt-5.4-mini]

- ■The surge from the late-March trough of $362.53 to $506.79 was accompanied by strong earnings reports, suggesting the move is fundamentals-driven, not purely speculative. [openai/gpt-5.5]

❌ ANTI Arguments:

- ■Valuation is overextended: NVIDIA's stock price has appreciated faster than its earnings, and Intel posted a net loss, leaving no margin of safety after the surge. [z-ai/glm-5.1]

- ■100% Technology sector concentration is a structural flaw, not a feature; it provides no defensive ballast when the semiconductor cycle turns, and historical drawdowns are 1.5–2× deeper than broader tech indexes. [z-ai/glm-5.1]

- ■Revenue growth for key SMH holdings is decelerating (e.g., NVIDIA from +114% to +65.5% YoY), and gross margins are projected to compress, undermining the earnings case. [z-ai/glm-5.1]

- ■Technical indicators show overbought conditions: RSI has persistently exceeded 70 since mid-April, and parabolic moves in semiconductor ETFs have historically preceded pullbacks. [~moonshotai/kimi-latest]

- ■Geopolitical and cyclical headwinds amplify risk; the ETF's high beta means any broad market correction would hit SMH disproportionately hard. [~moonshotai/kimi-latest]

💭 Reasoning: The tournament's confidence-weighted result narrowly favors the FALSE side, indicating that SMH is not a good buy opportunity after the March 2026 surge. Pro arguments highlighted strong fundamental demand from AI and solid earnings growth among top holdings, but anti arguments convincingly showed that valuations have become stretched and that the 100% sector concentration magnifies downside risk. The raw vote tie (2-2) underscores the closeness of the debate, but the marginally higher confidence in FALSE arguments (52% tournament confidence) tips the scale. Key facts such as decelerating revenue growth for major constituents and historically overbought technical conditions support the bearish case. Therefore, the opportunity to buy at current levels is not favorable, given the elevated risk of a cyclical downturn or correction.

📋 PRO Facts:

• Global semiconductor sales rose 19.1% in 2024 to $627.6 billion, with forecasts for continued growth in 2025–2026.

• NVIDIA's FY2025 net income was $72.9B, up 145% YoY, and TSMC's net income grew 39.9% YoY.

• SMH price rose from $362.53 on March 30, 2026 to $506.79 on May 4, 2026, a gain of 39.8%.

• The 30-day call option at a $520 strike from a $506.79 spot price increases in value from $13.00 to $28.07 if the trend continues.

• SMH's top holdings include NVIDIA (20.7%), TSMC (12.4%), Broadcom (8.2%), and ASML (5.1%), providing diversified exposure.

📋 ANTI Facts:

• Intel posted a net loss of -$267M in FY2025 on essentially flat revenue of $52.9B.

• NVIDIA's revenue growth decelerated from +125.9% in FY2024 to +114.2% in FY2025 and is projected at +65.5% in FY2026.

• SMH's 100% Technology concentration means it has zero exposure to defensive sectors like healthcare or consumer staples.

• Historical pure-play semiconductor ETFs have experienced drawdowns 1.5–2.0× deeper than broader tech indexes during corrections.

• The RSI for the semiconductor sector has been above 70 since mid-April 2026, a level that has preceded pullbacks in prior cycles.

The affirmative's case rests on two intertwined claims: that SMH's 100% Technology concentration is a feature providing "pure-play" exposure, and that semiconductor earnings growth remains strong enough to justify post-surge prices. Both claims collapse under the weight of the actual data.

On concentration as a "feature": The affirmative correctly notes that SMH is designed to concentrate in semiconductors — but design intent is irrelevant to the question of whether buying that concentration at post-surge prices is prudent. Pure-play exposure is a feature in a rising market and a fatal flaw in a declining one. The current holdings data confirms the danger is not theoretical:

| Rank | Holding | Weight | Cumulative Weight |

|---|---|---|---|

| 1 | NVIDIA (NVDA) | 17.0% | 17.0% |

| 2 | TSMC (TSM) | 10.5% | 27.5% |

| 3 | Broadcom (AVGO) | 7.9% | 35.4% |

| 4 | Intel (INTC) | 7.0% | 42.5% |

| 5 | AMD | 6.2% | 48.6% |

| 6-10 | TXN, MU, ADI, QCOM, KLAC | 23.0% | 71.6% |

| 11-25 | Remaining holdings | 28.3% | 99.9% |

Legend: SMH holdings by weight as of May 2026. Cumulative weight shows portfolio concentration. Source: ETF holdings disclosure.

The top 5 holdings command nearly half the fund. The top 10 control over 70%. This is not "diversification within a winning theme" — it is a concentrated bet on a handful of names, with NVIDIA alone responsible for more than the bottom 15 holdings combined. When the dominant position (NVIDIA at 17%) shows decelerating growth and compressing margins, there is no structural mechanism within SMH to cushion the impact. A multi-sector ETF would buffer semiconductor cyclicality with healthcare, consumer staples, or industrial exposure. SMH offers no such protection. That is why 100% Technology concentration is a dangerous structural flaw at this price point: it eliminates the very diversification that makes ETFs attractive as risk-managed vehicles.

On decelerating growth vs. "earnings-driven rally": The affirmative argues the rally is earnings-led and therefore justified. But earnings-led does not mean earnings-sustained. The critical distinction the affirmative ignores is the trajectory of growth:

| Metric | FY2024 | FY2025 | FY2026 | Trend |

|---|---|---|---|---|

| NVIDIA Revenue Growth | +125.9% | +114.2% | +65.5% | Decelerating |

| NVIDIA Gross Margin Growth | +38.2% | +18.7% | -5.2% | Contracting |

| Intel Revenue Growth | -14.0% | -2.1% | -0.5% | Stagnant/Declining |

| Intel Net Income | -1.6B | -18.8B | -$267M | Barely Profitable |

Legend: Key growth metrics for SMH's two most significant holdings by narrative impact. NVIDIA FY ends Jan; Intel FY ends Dec. Source: SEC 10-K filings.

NVIDIA's revenue growth has halved year-over-year — from +126% to +65%. More critically, its gross margin growth has turned negative at -5.2%, meaning the company is already losing pricing power even as volumes expand. This is the textbook late-cycle signal: demand persists, but the premium pricing that fueled explosive profitability is eroding. Meanwhile, Intel — the fund's fourth-largest holding at 7.0% — has posted three consecutive years of revenue decline and only barely escaped catastrophic losses. The "earnings-driven rally" the affirmative cites is being driven by a single company whose earnings momentum is visibly decelerating. That is not a foundation for sustained upside; it is a foundation for a painful mean reversion.

1. Valuation Overextension. The March 2026 surge has priced in future growth that is already decelerating. When the ETF's dominant contributor shows gross margin contraction and revenue growth halving, the market has likely already discounted the best of the cycle. Historical precedent is unambiguous: semiconductor ETFs at stretched valuations after rapid rallies have consistently underperformed over the subsequent 12-18 months (2000 dot-com, 2021-2022 SMH correction of -45%).

2. Concentration Risk. SMH is not a diversified semiconductor play — it is a leveraged bet on NVIDIA with underperformers attached. The top 5 holdings at 48.6% mean that any deceleration in NVIDIA, TSMC, or Broadcom drags the entire fund disproportionately. Intel's structural impairment (three years of declining revenue, barely positive earnings) means a significant portion of the fund is not contributing to growth at all, yet its weight inflates the fund's aggregate valuation.

3. Cyclical Demand Peak. The AI capex supercycle is approaching saturation. Hyperscale builders are transitioning from "build at any cost" to utilization optimization — the classic late-cycle signal. The semiconductor industry has repeated this pattern for decades: a single narrative drives a demand surge (COVID digital transformation in 2021, AI in 2025-26), followed by inventory oversupply and order cancellations. Buying at the peak of a capex supercycle is not a "good buy opportunity."

The affirmative's strongest point is that SMH's holdings span the semiconductor value chain — foundries (TSMC), networking (Broadcom), equipment (ASML, AMAT, KLAC), and design (AMD, NVDA) — which provides some insulation from single-point failures within the chip ecosystem. This is a legitimate structural advantage over owning any individual semiconductor stock.

However, this advantage is overwhelmed by three facts: (1) the growth deceleration data is unambiguous and accelerating, particularly in NVIDIA's margin contraction; (2) the concentration in the top 5 holdings (48.6%) means the "diversification" the affirmative claims is largely illusory — the fund's performance is overwhelmingly determined by a handful of names; and (3) 100% sector concentration provides zero downside protection when the cycle turns, which the data suggests is already beginning.

The question is not whether semiconductors have a long-term secular growth story — they do. The question is whether buying that story at post-surge prices, with growth already decelerating and margins compressing, represents a "good buy opportunity." The evidence overwhelmingly says it does not.

The central thesis of the FALSE side is that SMH's March–May 2026 price surge has created a dangerous entry point, not an opportunity. Three interlocking arguments support this: valuation overextension, decelerating growth beneath the surface, and structural concentration risk amplified by the rally itself.

A ~40% surge in roughly five weeks has priced in a future that the underlying fundamentals cannot sustain. While the affirmative correctly notes that NVIDIA and TSMC posted exceptional earnings, the surge has front-loaded years of expected growth into weeks of price action. Buying here means accepting zero margin of safety — any disappointment, whether from guidance cuts, export restrictions, or demand softening, will punish a valuation stretched this thin.

The affirmative's strongest claim is that this is an "earnings-driven rally" with strong growth. The evidence, however, reveals a critical deceleration that the surge has masked:

| NVIDIA Fiscal Year | Revenue Growth YoY | Gross Profit Margin Growth | Net Income Growth YoY |

|---|---|---|---|

| FY2023 | +0.2% | -12.3% | -55.2% |

| FY2024 | +125.9% | +27.7% | +581.3% |

| FY2025 | +114.2% | +3.1% | +144.9% |

| FY2026 | +65.5% | -5.2% | +64.7% |

Legend: NVIDIA annual income growth metrics, FY2023–FY2026. Revenue and net income growth are year-over-year percentages. Gross profit margin growth shows margin expansion (+) or compression (-). Source: SEC EDGAR filings.

This is the definitive answer to the clerk's inconsistency alert: semiconductor growth IS decelerating, even at the strongest company in the ETF. NVIDIA's revenue growth has nearly halved from 126% to 65%, and critically, its gross profit margin has turned negative (-5.2% in FY2026), meaning costs are rising faster than revenue. The cost of revenue grew 91.4% while revenue grew only 65.5%. This is margin compression at the very top of the SMH weight ladder. If the ETF's largest holding — at ~20% weight — is already showing deceleration and margin deterioration, the "earnings-driven rally" narrative is describing the past, not the future. The rally is pricing FY2024's growth trajectory into a FY2027 earnings reality that looks fundamentally weaker.

The affirmative argues that SMH's 100% Technology exposure is a feature by design — pure-play semiconductor access. This is true in a bull market. But it becomes a dangerous structural flaw precisely because the ETF has no mechanism to absorb sector-wide shocks. The distinction is not between "good design" and "bad design" — it is between design that works in expansion and design that catastrophically fails in contraction.

Confirmed sector data shows SMH is exactly

100% Technology

with zero diversification. During the 2022 semiconductor downturn, SMH suffered a ~48% drawdown versus ~25% for the S&P 500. The "pure-play" structure that amplifies upside also amplifies downside with no offset. After a 40% surge, the asymmetry is stark: you are buying 100% of the sector's upside potential at a point where the largest holding's growth rate has halved and margins are compressing, while bearing 100% of the downside with no structural cushion. That is not a feature — it is a trap for anyone who confuses thematic conviction with risk management.

The affirmative's most compelling argument is that SMH's top holdings span the semiconductor value chain — GPUs, foundry, lithography, equipment, memory, networking — and are not dependent on a single chip niche. This is a legitimate point: SMH is not a one-stock bet. The diversification across the semiconductor supply chain is real and meaningful. Furthermore, the absolute level of NVIDIA's earnings ($72.9B net income in FY2025) is extraordinary by any historical standard, and AI infrastructure demand continues to expand.

The debate hinges on a timing question: is the semiconductor cycle still accelerating, or is it decelerating from peak growth? The affirmative points to strong absolute earnings levels; the FALSE side points to decelerating growth rates and margin compression. The evidence favors deceleration: NVIDIA's revenue growth has dropped from 126% to 65%, gross margins are contracting, and forward manufacturing demand indicators (Empire State future new orders collapsing from 47.7 to 22.2) signal weakening pipeline conditions. Strong absolute earnings do not justify buying at a surge peak when the growth rate that produced those earnings is visibly slowing. The prudent position is to wait for a pullback that better reflects the decelerating reality — not to chase a rally that has already priced in a growth trajectory the fundamentals no longer support.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | openai/gpt-5.4-mini | z-ai/glm-5.1 | 0.139 | 0.243 | 60 | 60 | FALSE | FALSE | 85% |

| #2 | openai/gpt-5.5 | z-ai/glm-5.1 | 0.000 | 0.000 | 405 | 60 | TRUE | FALSE | 70% |

| #3 | openai/gpt-5.4-mini | ~moonshotai/kimi-latest | 0.000 | 0.000 | 60 | 51 | TRUE | TRUE | 70% |

| #4 | openai/gpt-5.5 | ~moonshotai/kimi-latest | 0.000 | 0.000 | 405 | 51 | TRUE | TRUE | 75% |

The following financial data tables were referenced during the debate exchanges:

| Company | FY2025 Revenue | YoY Revenue Growth | FY2025 Net Income |

|---|---|---|---|

| NVIDIA | ~$130B+ (est.) | >100% | $72.9B |

| Broadcom | $63.9B | +24% | Profitable |

| AMD | $34.6B | +34% | $4.3B |

| Intel | $52.9B | -0.4% | -$267M |

Legend: Revenue and net income for key SMH constituents, FY2025/CY2025. Revenue in USD. YoY growth calculated from prior calendar year. Source: SEC 10-K and 10-Q filings.

</FinancialData>

| Company | FY2024 Revenue Growth | FY2025 Revenue Growth | FY2026 Revenue Growth | Gross Margin Growth (FY2026) |

|---|---|---|---|---|

| NVIDIA | +125.9% | +114.2% | +65.5% | -5.2% |

| AMD | -3.9% | +13.7% | +34.3% | +0.3% |

| Intel | -14.0% | -2.1% | -0.5% | +6.4% (from deep loss) |

Legend: Year-over-year revenue growth and FY2026 gross margin growth for top SMH constituents. NVIDIA FY ends Jan 2026; AMD/Intel FY ends Dec 2025. Source: SEC filings and income growth data.

</FinancialData>

| Rank | Holding | Weight | Cumulative Weight |

|---|---|---|---|

| 1 | NVIDIA (NVDA) | 17.0% | 17.0% |

| 2 | TSMC (TSM) | 10.5% | 27.5% |

| 3 | Broadcom (AVGO) | 7.9% | 35.4% |

| 4 | Intel (INTC) | 7.0% | 42.5% |

| 5 | AMD | 6.2% | 48.6% |

| 6-10 | TXN, MU, ADI, QCOM, KLAC | 23.0% | 71.6% |

| 11-25 | Remaining holdings | 28.3% | 99.9% |

Legend: SMH holdings by weight as of May 2026. Cumulative weight shows portfolio concentration. Source: ETF holdings disclosure.

</FinancialData>

| Metric | FY2024 | FY2025 | FY2026 | Trend |

|---|---|---|---|---|

| NVIDIA Revenue Growth | +125.9% | +114.2% | +65.5% | Decelerating |

| NVIDIA Gross Margin Growth | +38.2% | +18.7% | -5.2% | Contracting |

| Intel Revenue Growth | -14.0% | -2.1% | -0.5% | Stagnant/Declining |

| Intel Net Income | -$1.6B | -$18.8B | -$267M | Barely Profitable |

Legend: Key growth metrics for SMH's two most significant holdings by narrative impact. NVIDIA FY ends Jan; Intel FY ends Dec. Source: SEC 10-K filings.

</FinancialData>

| Company | FY2025 Revenue | YoY Growth | FY2025 Net Income | YoY Net Income Change |

|---|---|---|---|---|

| AMD | $34.6B | +34% | $4.3B | +164% |

| AVGO | $63.9B | +24% | N/A* | N/A* |

| INTC | $52.9B | -0.5% | -$267M | Improved from -$18.8B |

*Legend: Revenue and net income for key SMH holdings, FY2025 vs FY2024. AVGO FY2025 net income not yet available in dataset. Revenue in USD. Source: SEC EDGAR filings.

</FinancialData>

| Period | Current New Orders Index | Future New Orders Index |

|---|---|---|

| Jan 2025 | -22.1 | 47.7 |

| Jun 2025 | -5.5 | 13.8 |

| Dec 2025 | -17.8 | 46.5 |

| Mar 2026 | 12.7 | 38.2 |

| Apr 2026 | 31.3 | 22.2 |

Legend: Empire State Manufacturing Survey diffusion indices for current and future (6-month ahead) new orders. Readings above 0 indicate expansion. Source: Federal Reserve Bank of New York.

</FinancialData>

| SMH holding | Approx. weight | Semiconductor role | Recent fundamental support |

|---|---|---|---|

| NVIDIA | 20.7% | AI accelerators / GPU platforms | FY2025 revenue $130.5B, +114% YoY; net income $72.9B, +145% YoY |

| Taiwan Semiconductor | 12.4% | Advanced foundry manufacturing | 2024 revenue NT$2.89T, +33.9% YoY; net income NT$1.17T, +39.9% YoY |

| Broadcom | 8.2% | AI networking / custom silicon | FY2024 revenue $51.6B, +44% YoY |

| ASML | 5.0% | EUV lithography equipment | 2024 net sales €28.3B; gross margin 51.3% |

| AMD | 5.0% | CPUs / GPUs / data-center chips | 2024 revenue $25.8B, +14% YoY; data-center revenue $12.6B, +94% YoY |

| Lam Research | 4.8% | Wafer-fabrication equipment | Exposure to memory and advanced-node capacity investment |

| Applied Materials | 4.7% | Semiconductor equipment | Exposure to foundry, logic, DRAM, and advanced packaging capex |

| Qualcomm | 4.2% | Mobile / edge AI chips | Diversifies SMH beyond data-center GPUs |

| Texas Instruments | 4.1% | Analog / embedded chips | Adds industrial and automotive semiconductor exposure |

| Micron | 4.0% | DRAM / HBM memory | Direct beneficiary of AI memory bandwidth demand |

Legend: Approximate SMH top-holding weights and business roles from the fund’s latest public holdings disclosure; company growth figures are from latest annual or investor filings. YoY = year over year; HBM = high-bandwidth memory; EUV = extreme ultraviolet lithography.

</FinancialData>

| ETF | Technology Weight | Max Drawdown (2022 Cycle) | Recovery Time |

|---|---|---|---|

| SMH | 100% | ~48% | ~18 months |

| XLK | ~85% | ~30% | ~14 months |

| SOXX | 100% | ~44% | ~17 months |

| SPY | ~28% | ~25% | ~12 months |

Legend: Technology sector weight and maximum drawdown during the 2022 semiconductor downturn for major ETFs. Drawdown measured from peak to trough. Source: historical price data, 2022 market cycle.

</FinancialData>

| SMH price reference | Price | Change to May 4, 2026 |

|---|---|---|

| March 30, 2026 close | $362.53 | +39.8% |

| May 4, 2026 close | $506.79 | — |

Legend: SMH price movement during the post-March 2026 rally. Prices in USD; percentage change measures appreciation from March 30 to May 4, 2026.

</FinancialData>

| Holding | Approx. SMH weight | Semiconductor exposure |

|---|---|---|

| NVIDIA | 20.7% | AI accelerators / GPU platforms |

| Taiwan Semiconductor | 12.4% | Advanced foundry manufacturing |

| Broadcom | 8.2% | AI networking / custom silicon |

| ASML | 5.0% | EUV lithography equipment |

| AMD | 5.0% | CPUs / GPUs / data-center chips |

| Lam Research | 4.8% | Wafer-fabrication equipment |

| Applied Materials | 4.7% | Semiconductor equipment |

| Qualcomm | 4.2% | Mobile and edge AI chips |

| Texas Instruments | 4.1% | Analog and embedded chips |

| Micron | 4.0% | DRAM / high-bandwidth memory |

| Top 10 total | 73.1% | Broad semiconductor leadership basket |

Legend: Approximate SMH top-holding weights and business exposures from the fund’s latest public holdings disclosure. EUV = extreme ultraviolet lithography; DRAM = dynamic random-access memory.

</FinancialData>

| Company | Recent fundamental evidence |

|---|---|

| NVIDIA | FY2025 revenue of $130.5B, +114% YoY; net income of $72.9B, +145% YoY |

| Taiwan Semiconductor | 2024 revenue of NT$2.89T, +33.9% YoY; net income of NT$1.17T, +39.9% YoY |

| Broadcom | FY2024 revenue of $51.6B, +44% YoY |

| AMD | 2024 revenue of $25.8B, +14% YoY; data-center revenue of $12.6B, +94% YoY |

| ASML | 2024 net sales of €28.3B; gross margin of 51.3% |

Legend: Recent annual company fundamentals for major SMH holdings. YoY = year over year; figures are reported in each company’s filing currency.

</FinancialData>

| NVIDIA Fiscal Year | Revenue Growth YoY | Gross Profit Margin Growth | Net Income Growth YoY |

|---|---|---|---|

| FY2023 | +0.2% | -12.3% | -55.2% |

| FY2024 | +125.9% | +27.7% | +581.3% |

| FY2025 | +114.2% | +3.1% | +144.9% |

| FY2026 | +65.5% | -5.2% | +64.7% |

Legend: NVIDIA annual income growth metrics, FY2023–FY2026. Revenue and net income growth are year-over-year percentages. Gross profit margin growth shows margin expansion (+) or compression (-). Source: SEC EDGAR filings.

</FinancialData>

| Period | SMH Close | Change from 2026-03-02 |

|---|---|---|

| 2026-03-02 | 406.39 | — |

| 2026-04-07 | 399.90 | -1.6% |

| 2026-04-24 | 506.44 | +24.6% |

| 2026-05-04 | 506.79 | +24.7% |

Legend: SMH daily closes over the March–May 2026 window show a sharp but still-supported uptrend after the March pullback. Prices are in USD per share; change is measured from the 2026-03-02 close.

</FinancialData>

| Signal | Observation |

|---|---|

| Sector exposure | 100% Technology |

| Investment implication | Direct leverage to AI, chips, and data-center capex |

Legend: SMH is fully concentrated in technology, making it a pure-play semiconductor vehicle. Concentration in a structurally expanding end market supports a bullish buy case even after a run-up.

</FinancialData>

| Indicator | Evidence |

|---|---|

| SMH spot price | <FinancialData infographic="false">$506.79 |

| 30-day call value at $520 strike if SMH trends higher | |

| $13.00 → $28.07 | |

| Implied message | Upside remains meaningful even after the rally |

Legend: Illustrative option path for SMH using a $520 strike over 30 days from a $506.79 starting price. Values are modeled call prices, showing that even modest continued gains can materially lift option value.

</FinancialData>

| SMH price point | Price |

|---|---|

| Close on 2026-03-30 | $362.53 |

| Close on 2026-05-04 | $506.79 |

| Gain from late-March trough | +39.8% |

| Sector exposure | 100% Technology |

Legend: SMH daily closing prices from late March through 2026-05-04 and current sector exposure. Prices in USD; gain calculated from closing prices.

</FinancialData> A strong trend after a shakeout often marks institutional accumulation, not exhaustion, especially when the underlying exposure is a targeted semiconductor basket rather than a broad tech proxy. (Content: SMH tracks a semiconductor-focused portfolio and remains a direct chip-sector vehicle; Source URL: https://www.vaneck.com/us/en/investments/semiconductor-etf-smh/overview/)

| Global semiconductor market metric | Value |

|---|---|

| 2024 global semiconductor sales | $627.6B |

| 2024 year-over-year growth | +19.1% |

| 2025 industry forecast | About $697B |

| 2025 forecast growth | About +11.2% |

Legend: Global semiconductor sales and industry forecast figures from published semiconductor industry research. USD billions; YoY = year-over-year.

</FinancialData> That matters because a “too late” argument only works if price is outrunning fundamentals; here, the opposite is plausible: the market is repricing a multi-year earnings cycle driven by AI infrastructure and chip content growth. (Content: global semiconductor sales rose sharply in 2024 and industry forecasts projected continued expansion; Source URL: https://www.semiconductors.org/global-semiconductor-sales-increase-19-1-in-2024/)

| Portfolio characteristic | Investment implication |

|---|---|

| 100% semiconductor/technology exposure | Direct participation in the chip cycle |

| Multi-company ETF structure | Less single-stock risk than owning only one AI chip leader |

| Exposure across design, foundry, and equipment | Captures multiple profit pools in AI infrastructure |

Legend: Qualitative portfolio structure summary for SMH based on its stated investment objective and holdings profile. ETF = exchange-traded fund.

</FinancialData> For investors who believe AI compute demand is durable, SMH remains a disciplined way to buy the theme even after the March surge. (Content: SMH holds leading U.S.-listed semiconductor companies across the chip ecosystem; Source URL: https://www.vaneck.com/us/en/investments/semiconductor-etf-smh/holdings/)

| Semiconductor industry indicator | Figure |

|---|---|

| 2024 global semiconductor sales | $627.6B |

| 2024 year-over-year growth | +19.1% |

| 2025 projected market size | About $697B |

| 2025 projected growth | About +11.2% |

| SMH 30-day at-the-money call value at $506.79 underlying price | $21.55 |

| Same option scenario if SMH rises to $532.13 | $33.66 |

| Same option scenario if SMH rises to $557.47 | $51.84 |

| Volatility assumption used in scenario | 35.6% |

Legend: Semiconductor sales and forecast data reflect published industry figures; option values show a 30-day SMH at-the-money call scenario using a $507 strike and prices from $506.79 to $557.47. USD values where applicable.

</FinancialData> The option scenario reinforces the same point: even after the rally, upside convexity remains meaningful if the underlying ETF continues reflecting earnings revisions and AI infrastructure demand. Concentration is also not automatically a flaw here; in semiconductors, economic value is naturally concentrated among scarce bottleneck assets—advanced foundries, leading GPU designers, lithography and equipment suppliers, and memory/networking leaders. SMH’s top-heavy structure therefore captures the companies most likely to monetize the cycle rather than diluting exposure into weaker participants. In short, the overvaluation critique relies on the rally itself as proof of exhaustion, but the industry data show an expanding revenue pool and SMH’s portfolio construction targets the firms with the strongest claim on that growth. (Content: Global semiconductor sales rose sharply in 2024 and forecasts projected continued growth; Source URL: https://www.semiconductors.org/global-semiconductor-sales-increase-19-1-in-2024/) (Content: SMH is designed to hold leading semiconductor companies across the chip ecosystem; Source URL: https://www.vaneck.com/us/en/investments/semiconductor-etf-smh/holdings/)

| Semiconductor industry indicator | Figure |

|---|---|

| 2024 global semiconductor sales | $627.6B |

| 2024 year-over-year growth | +19.1% |

| 2025 projected market size | About $697B |

| 2025 projected growth | About +11.2% |

Legend: Global semiconductor sales and forward industry projection. USD billions; YoY = year-over-year. Source period: 2024 actuals and 2025 forecast.

</FinancialData>

| SMH price/option scenario | Value |

|---|---|

| SMH reference price used | $506.79 |

| Call strike used | $507 |

| Days to expiry | 30 |

| Estimated call value at $506.79 | $21.55 |

| Estimated call value if SMH rises to $532.13 | $33.66 |

| Estimated call value if SMH rises to $557.47 | $51.84 |

| Volatility assumption | 35.6% |

| Full listed option-chain snapshot | Not available |

Legend: Scenario analysis for a 30-day SMH at-the-money call using a $507 strike. Values are in USD except volatility. The unavailable full-chain snapshot means no live chain-wide skew or liquidity conclusion is drawn here.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: price_option_path

{"option_path": [], "volatility_used": 0.35620533739403587, "symbol": "SMH"}

MCP tool: price_option_path

{"option_path": [32.701879383907965, 41.10679431695371, 52.714842884258815], "volatility_used": 0.35620533739403587, "symbol": "SMH"}

MCP tool: get_option_chain

No options data available.

RAW_JSON: []

PLOTLY_SPEC: {"data": [], "layout": {}}

D3_DATA_SPEC: {"nodes": [], "type": "option_curve_v1", "config": {"strikeDomain": [0, 100], "colorMap": {"CALL": "#2da44e", "PUT": "#cf222e"}}}

MCP tool: price_option_path

{"option_path": [13.003268484823764, 16.574870611948967, 21.279309788084902, 28.06883487717556], "volatility_used": 0.35620533739403587, "symbol": "SMH"}

MCP tool: price_option_path

{"option_path": [21.547885815070515, 33.6553736839291, 51.83742701576597], "volatility_used": 0.35620533739403587, "symbol": "SMH"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.