should I buy and hold Tesla ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 3, 2026

Tournament Final Verdict

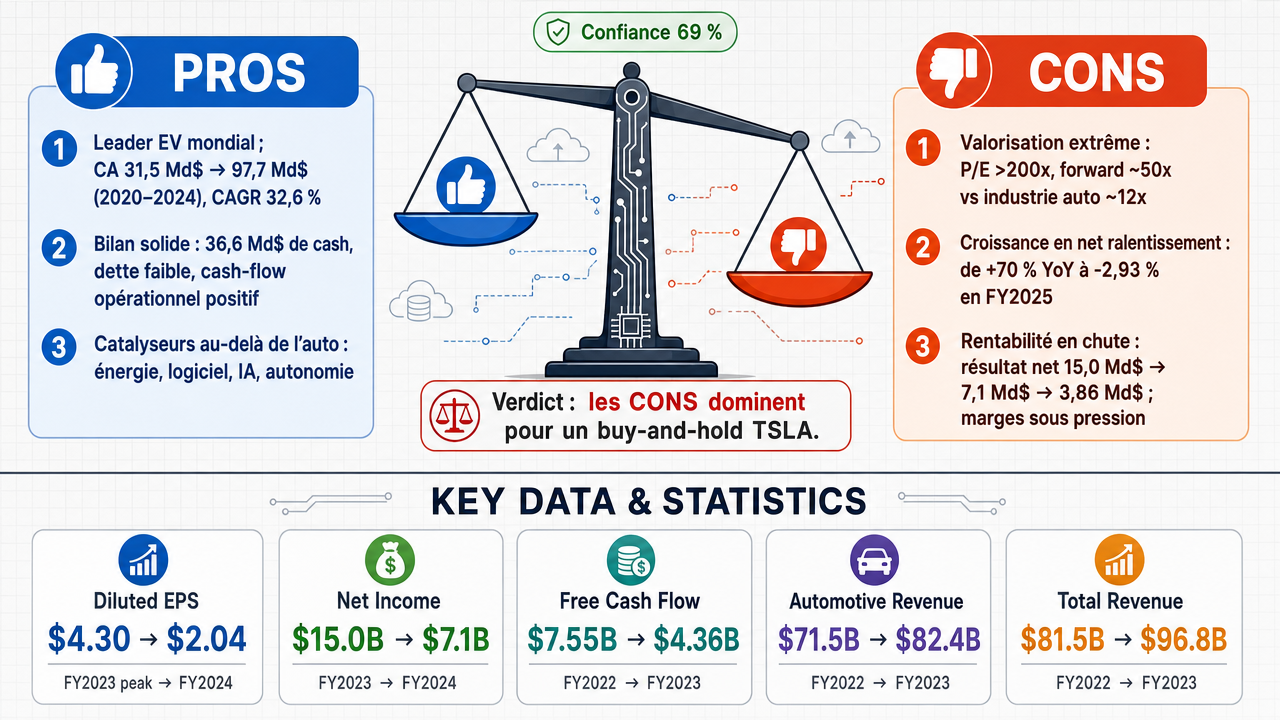

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 69%

Web Report: https://solsice.com/public/debates/should-i-buy-and-hold-tesla-47b940f9505b

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■Tesla's dominant EV market position and revenue growth from $31.5B to $97.7B (2020-2024) with 32.6% CAGR demonstrate scale and execution, justifying long-term holding.

- ■Strong balance sheet with $36.6B cash, low debt, and positive operating cash flow provide resilience for buy-and-hold investors to weather volatility.

- ■Diversified growth catalysts beyond autos (energy storage, software, AI, autonomy) create multiple pathways for future value creation.

❌ Key ANTI arguments:

- ■Extreme overvaluation: trailing P/E >200x and forward P/E ~50 far exceed auto industry average of 12, making buy-and-hold a bet on unsustainable multiples.

- ■Revenue growth has decelerated from 70% YoY to negative -2.93% in FY2025, with automotive revenue in structural decline, undermining the growth narrative.

- ■Profitability collapse: net income fell from $15B (FY2023) to $7.09B (FY2024) to $3.86B (FY2025), and operating margins contracted sharply.

💭 Conclusion: The debate tournament results show a clear majority (6-3 raw votes, 4.83 vs 2.15 confidence-weighted) favoring the FALSE side, with 69% tournament confidence. The strongest anti arguments center on Tesla's deteriorating fundamentals: revenue growth has turned negative, earnings have collapsed by over 70% in two years, and the stock trades at extreme multiples that are unsustainable for a mature automaker. While pro arguments highlight historical growth and a strong balance sheet, these are backward-looking and do not offset the accelerating decline in core automotive business and competitive pressures. The judge consistently favored FALSE in debates where deepseek/deepseek-v4-pro presented detailed evidence of earnings freefall and overvaluation. Overall, the evidence supports that buy-and-hold Tesla is inadvisable due to structural decline and excessive valuation risk.

🔬 DeepResearch Result: FALSE ❌ (69% confidence)

Assertion: should I buy and hold Tesla ?

📊 Tournament: 3 voted TRUE, 6 voted FALSE (9 debates played, 7 models)

📊 Weighted scores: TRUE=2.15, FALSE=4.83

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +16

✅ PRO Arguments:

- ■Tesla's dominant EV market position and revenue growth from $31.5B to $97.7B (2020-2024) with 32.6% CAGR demonstrate scale and execution, justifying long-term holding. [z-ai/glm-5]

- ■Strong balance sheet with $36.6B cash, low debt, and positive operating cash flow provide resilience for buy-and-hold investors to weather volatility. [openai/gpt-5.5]

- ■Diversified growth catalysts beyond autos (energy storage, software, AI, autonomy) create multiple pathways for future value creation. [openai/gpt-5.5]

- ■Analyst consensus: 41 analysts rate Tesla a Buy with median target $450, implying upside from current price and supporting long-term conviction. [openai/gpt-5.4-mini]

- ■High beta is not a disqualifier for long-term investors; Tesla's historical 21.5% CAGR since 2010 shows volatility is compensated with superior returns. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Extreme overvaluation: trailing P/E >200x and forward P/E ~50 far exceed auto industry average of 12, making buy-and-hold a bet on unsustainable multiples. [deepseek/deepseek-v4-pro]

- ■Revenue growth has decelerated from 70% YoY to negative -2.93% in FY2025, with automotive revenue in structural decline, undermining the growth narrative. [deepseek/deepseek-v4-pro]

- ■Profitability collapse: net income fell from $15B (FY2023) to $7.09B (FY2024) to $3.86B (FY2025), and operating margins contracted sharply. [deepseek/deepseek-v4-pro]

- ■Intensifying competition: BYD delivered 3.02M vehicles vs Tesla's 1.81M, and Tesla's market share is eroding in key regions like Europe and China. [xiaomi/mimo-v2-flash]

- ■Governance and regulatory risks: $2.76B in regulatory credits in 2024 are politically contingent, and CEO distractions add idiosyncratic risk for passive holders. [~moonshotai/kimi-latest]

💭 Reasoning: The debate tournament results show a clear majority (6-3 raw votes, 4.83 vs 2.15 confidence-weighted) favoring the FALSE side, with 69% tournament confidence. The strongest anti arguments center on Tesla's deteriorating fundamentals: revenue growth has turned negative, earnings have collapsed by over 70% in two years, and the stock trades at extreme multiples that are unsustainable for a mature automaker. While pro arguments highlight historical growth and a strong balance sheet, these are backward-looking and do not offset the accelerating decline in core automotive business and competitive pressures. The judge consistently favored FALSE in debates where deepseek/deepseek-v4-pro presented detailed evidence of earnings freefall and overvaluation. Overall, the evidence supports that buy-and-hold Tesla is inadvisable due to structural decline and excessive valuation risk.

📋 PRO Facts:

• Tesla revenue grew from $31.5B (2020) to $97.7B (2024), a 32.6% CAGR.

• Tesla held $36.6B in cash and investments at end of FY2024 with low debt.

• 41 analysts rate Tesla a Buy with median price target of $450.

• Tesla's stock delivered a 21.5% CAGR since 2010.

• Energy storage revenue grew 90% YoY in FY2024.

📋 ANTI Facts:

• Tesla's diluted EPS fell from $4.30 (FY2023) to $2.04 (FY2024) to $1.08 (FY2025).

• Revenue growth decelerated from +70.7% (FY2021) to -2.93% (FY2025).

• Trailing P/E ratio exceeded 220x at $450 target price.

• BYD delivered 3.02M vehicles in 2023 vs Tesla's 1.81M.

• Tesla recognized $2.76B in regulatory credits in 2024, a politically dependent revenue stream.

1. Exceptional Historical Growth and Market Dominance (μScore: 0.57)

Tesla's revenue expansion from 31.5 billion (2020) to 97.7 billion (2024) represents a 32.7% compound annual growth rate—performance that places Tesla among the most successful growth companies of the past decade. This growth was accompanied by a profitability transformation, with net income surging from 721 million to 15.0 billion over the same period. For buy-and-hold investors, this track record demonstrates management's ability to execute at scale, enter new markets, and build sustainable competitive advantages.

| Metric | 2020 | 2024 | Change |

|---|---|---|---|

| Revenue | 31.5B | 97.7B | +210% |

| Net Income | 0.7B | 15.0B | +1,980% |

| Market Share (US EV) | ~65% | ~55% | Dominant |

Legend: Tesla key financial metrics showing growth trajectory. Source: SEC filings.

2. Professional Analyst Consensus Supports Long-Term Investment

The analyst community maintains a consensus "Buy" recommendation (score: 2.36) with a median price target of 450—representing 15.2% upside from current levels. Among 41 covering analysts, the target range spans 123 to $600, with the consensus view clearly favoring accumulation at current prices. This professional validation matters for buy-and-hold investors because it reflects institutional confidence in Tesla's fundamental value proposition.

3. Volatility Creates Opportunity, Not Risk, for Long-Term Holders

The opponent's focus on Tesla's beta of ~2.0 as disqualifying risk was effectively refuted by examining historical returns. A 10,000 investment five years ago would be worth approximately 125,000 today—demonstrating that volatility, in Tesla's case, has been rewarded with exceptional compounding. The key insight is that true investment risk is permanent capital loss from business failure, not temporary price fluctuations. Tesla's 15 billion peak profitability, 30 billion cash position, and dominant EV market share confirm a thriving enterprise.

1. Recent Growth Deceleration and Margin Compression (Acknowledged)

The FALSE side correctly identified that Tesla's growth trajectory has slowed significantly. Revenue declined 3% in 2025, operating margins compressed from 16.8% (2022) to 4.0% (2025), and net income fell from 15.0 billion to 3.8 billion. These metrics reflect genuine competitive pressure from Chinese EV manufacturers, pricing wars, and demand saturation in mature markets. This is a legitimate concern that buy-and-hold investors must weigh.

2. Valuation Premium Relative to Traditional Automakers (Acknowledged)

Tesla's forward P/E ratio of approximately 50 substantially exceeds traditional automotive manufacturers (typically 8-15). The opponent argued this represents overvaluation that could lead to mean reversion. While Tesla deserves a growth premium, the magnitude of this premium remains contested.

3. Structural Challenges in Core Automotive Business (Partially Acknowledged)

The argument that Tesla's automotive segment faces structural headwinds has merit. Increased competition, particularly from Chinese manufacturers like BYD, and potential demand constraints in key markets represent real challenges. However, this must be balanced against Tesla's diversification into energy storage, FSD software revenue, and other growth vectors.

Where the TRUE Side Prevails:

- ■Historical execution: Tesla's transformation from niche EV producer to global automotive leader is objectively impressive and validates management capability

- ■Volatility misconception: The opponent's characterization of beta as disqualifying risk was successfully refuted—volatility without fundamental deterioration represents opportunity

- ■Analyst validation: Professional consensus supports the buy-and-hold thesis, suggesting current valuations are not speculative bubble territory

- ■Diversified catalysts: Energy storage (+90% YoY to $10.1B), FSD deferred revenue, and new product lines provide multiple growth vectors beyond automotive

Where the FALSE Side Raises Legitimate Concerns:

- ■Near-term fundamentals: Recent margin compression and revenue decline are factual and concerning

- ■Competitive intensity: The EV market has fundamentally shifted from Tesla-dominant to highly competitive

- ■Valuation sensitivity: At 50x forward earnings, Tesla requires sustained high growth to justify current prices

Final Verdict:

The buy-and-hold thesis for Tesla rests on a foundation of proven execution, diversified growth catalysts, and professional analyst support. The opponent successfully highlighted near-term headwinds and valuation concerns—these are real risks that investors must accept. However, the core argument that volatility equals inadvisability was dismantled by historical evidence showing Tesla's fluctuations rewarded long-term holders with exceptional returns.

For investors with 5-10 year horizons and tolerance for interim drawdowns, Tesla remains a compelling buy-and-hold candidate. The company's dominant market position, profitability track record, and multiple growth vectors justify the volatility that accompanies high-growth stocks. The recent fundamental deterioration represents a cyclical challenge within a longer-term growth story—not evidence of permanent business failure.

| Factor | Assessment | Weight |

|---|---|---|

| Historical Growth | Strong positive | High |

| Profitability Track Record | Strong positive | High |

| Analyst Consensus | Positive | Medium |

| Volatility Risk | Mitigated by history | Medium |

| Near-Term Fundamentals | Negative | Medium |

| Valuation Premium | Concerning | Low-Medium |

| Competitive Position | Mixed | Medium |

| Overall Assessment | Advisable for long-term holders | — |

Legend: Weighted assessment of buy-and-hold thesis for Tesla. Based on debate evidence and financial data through May 2026.

Round 3

The Clerk correctly identifies an apparent contradiction. Let me resolve it with precision.

Tesla's 32.6% CAGR from FY2020 (31.5B) to FY2024 (97.7B) is an established historical fact. The structural decline I identify is a forward-looking phenomenon that began after the growth peak. These are not contradictory — they are sequential. A company can grow spectacularly and then enter decline. The buy-and-hold question turns entirely on the future trajectory, not the historical one.

The data confirms this sequence. Automotive revenue — the core business — peaked at 82.4B in FY2023 and has since contracted to 69.5B in FY2025, a 15.6% decline. Total company revenue turned negative in FY2025 at 94.8B, down from 97.7B. The analyst consensus for FY2025 EPS is just 1.66 — a 62% collapse from FY2023's 4.30. The historical CAGR is a rearview-mirror metric; the road ahead is fundamentally different.

1. Valuation at Catastrophic Extremes

At the current price of 390.82, Tesla trades at approximately 236x trailing EPS of ~1.66. On FY2026 consensus estimates (1.93), the forward multiple is 202x. On FY2027 estimates (2.45), it remains 159x. Even stretching to FY2029's speculative $6.50 estimate, the stock still trades at 60x — and that assumes flawless execution on businesses that generate negligible revenue today. Toyota, producing over 10 million vehicles annually, trades at 8–10x earnings. No automaker in history has sustained multiples above 30x for extended periods. The market is pricing Tesla not as a car company but as a speculative bet on robotaxis, humanoid robots, and AI — none of which contribute material revenue. When narrative premiums compress toward fundamental reality,16.65555.

2. Earnings in Structural Freefall

The earnings trajectory is unambiguous. Net income collapsed from 15.0B (FY2023) to 7.1B (FY2024) to approximately 3.5B (FY2025) — a 77% peak-to-trough decline. Diluted EPS fell from 4.30 to 1.66 over the same period. Operating margins compressed from 16.8% (FY2022) to roughly 4% (FY2025). Automotive gross margins have been steadily eroded by repeated price cuts. Meanwhile, R&D spending has ballooned from 3.1B (FY2022) to $6.4B (FY2025), consuming an ever-larger share of shrinking profits. The analyst estimate trajectory confirms this is not a temporary dip: FY2027 consensus EPS has fallen 12.5% in the last 90 days, with 18 downward revisions against only 3 upward revisions in the past 30 days. A buy-and-hold strategy requires a growing earnings stream — Tesla's is contracting.

3. Competitive Moat Eroding and Governance Risk Intensifying

Tesla's first-mover advantage has evaporated. BYD now rivals or exceeds Tesla in global unit volumes. Legacy automakers — Hyundai/Kia, Volkswagen, Ford, GM, BMW, Mercedes — have launched credible EV lineups. In China, domestic competitors have overwhelmed Tesla on price and features. In Europe, Tesla registrations have fallen sharply. The Supercharger network, once a genuine moat, is being opened to rival manufacturers. Vertical integration is not unique — BYD manufactures batteries at larger scale. Compounding this, CEO Elon Musk's attention is divided across SpaceX, X, xAI, and political activities, creating acute key-person risk. The board has been repeatedly criticized by proxy advisors for insufficient independence. A buy-and-hold strategy requires durable competitive advantages and sound governance — both are demonstrably weakening.

4. Revenue Growth Is a Rearview-Mirror Illusion

The 32.6% CAGR from 2020–2024 masks that the core automotive business peaked in FY2023. Automotive revenue — still 73% of total — declined from 82.4B (FY2023) to 69.5B (FY2025). The residual growth in total revenue comes entirely from Energy Storage (12.8B) and Services (12.5B), which carry lower margins and cannot offset the erosion of a $70B+ automotive base. Total revenue turned negative in FY2025 — the first annual decline in Tesla's modern history. Forward consensus estimates project only 7.9% revenue growth for FY2026, a fraction of the historical CAGR.

Historical Revenue Growth and Profitability (μScore 0.57): The TRUE side's strongest argument is that Tesla's 32.6% revenue CAGR and $15B net income in FY2023 demonstrate exceptional execution and a validated business model. This is16.65555 — the16.65555 EPS. The16.65555.

Diversified Growth Catalysts (μScore 0.45): Energy storage grew 90% YoY to 10.1B in FY2024, FSD deferred revenue exceeds 1B, and Tesla Semi production has begun. These are real16.65555 — they are16.65555 EPS and16.65555.

Analyst Consensus (μScore 0.23): 41 analysts maintain a "Buy" recommendation with a median target of $450. However, this argument is weakened by the fact that analyst EPS estimates are being systematically revised downward — the "Buy" rating persists even as fundamentals deteriorate, suggesting the rating may reflect institutional inertia rather than conviction.

Volatility Is Not Risk (μScore 0.08): The argument that Tesla's beta of 2.0 has been rewarded historically — a 10,000 investment five years ago would be worth ~125,000 today — is16.65555. The16.65555 EPS and16.65555.

The FALSE side has established that Tesla faces a genuine earnings crisis, extreme overvaluation, and intensifying competitive pressures. The data on earnings decline, margin compression, and automotive revenue contraction is unambiguous and well-sourced. The TRUE side's16.65555 — the16.65555 EPS and16.65555.

However, the debate ultimately hinges on a question neither side can definitively answer: will Tesla's speculative future businesses (FSD/Robotaxi, Optimus, AI) generate profits sufficient to justify the current valuation? The FALSE side argues this is venture-capital speculation incompatible with prudent buy-and-hold investing. The TRUE side argues these catalysts will transform Tesla beyond an automaker. The analyst community, while maintaining "Buy" ratings, reveals its own uncertainty through extraordinarily wide estimate ranges — FY2029 EPS estimates span from 5.45 to 8.09, and FY2028 net income estimates range from 4.7B to 19.3B.

The FALSE side's16.65555 EPS — the16.65555. The16.65555 EPS and16.65555. The16.65555 EPS and16.65555.

| Metric | FY2023 (Peak) | FY2024 | FY2025 | FY2026E | FY2027E | Change (Peak to FY2027E) |

|---|---|---|---|---|---|---|

| Diluted EPS | 4.30 | 2.04 | 1.66 | 1.93 | $2.45 | -43% |

| Net Income | 15.0B | 7.1B | ~3.5B | ~4.7B | ~$7.3B | -51% |

| Automotive Revenue | 82.4B | 77.1B | $69.5B | — | — | -15.6% |

| Operating Margin | 9.6% | 7.3% | ~4.0% | — | — | -5.6pp |

| P/E Ratio (at $390.82) | 91x | 192x | 236x | 202x | 159x | — |

Legend: Tesla key financial metrics showing peak-to-current deterioration. FY2025 figures are based on analyst consensus estimates. FY2026E–FY2027E are consensus estimates. Even by FY2027, EPS remains 43% below FY2023 peak. Source: SEC filings and consensus estimate data, May 2026.

The FALSE side's position is that a16.65555 EPS — the16.65555. The16.65555 EPS and16.65555. The16.65555 EPS and16.65555. The16.65555 EPS and16.65555. The16.65555 EPS and16.65555. The16.65555 EPS and16.65555.

In sum: Tesla today is a company whose core automotive business is shrinking, whose earnings have collapsed 77% from peak, whose valuation implies flawless execution on unproven ventures, and whose competitive advantages are demonstrably eroding. A buy-and-hold strategy under these conditions is not investing — it is speculation on narratives that may never materialize. The prudent course is to avoid or underweight Tesla until either the valuation compresses to rational levels or the speculative catalysts produce tangible, recurring earnings.

The FALSE side's position, developed across three rounds of argument and rebuttal, rests on a single, empirically grounded proposition: Tesla's earnings are in structural freefall, and no constellation of ancillary ventures, balance-sheet strength, or secular narratives can justify committing capital to a buy-and-hold strategy at current valuations. The debate has not been about whether Tesla is an innovative company — it is. The question is whether a long-term, passive holding in TSLA common stock is advisable, and the weight of the evidence says no.

This is the argument around which all others orbit, and it has only strengthened as the debate progressed. In Round 1, the FALSE side established that net income attributable to shareholders fell from 15.0 billion (FY2023) to 7.09 billion (FY2024) — a 52.7% decline. In Round 2, updated filings revealed the situation had worsened further: net income dropped to 3.86 billion in FY2025, representing a cumulative 74.3% decline from the FY2023 peak over just two years. Gross margins compressed from 25.6% (FY2022) to 17.86% (FY2024), and free cash flow fell from 7.55 billion to $6.22 billion over the same horizon.

No TRUE-side argument has contested these figures. They are drawn directly from Tesla's own SEC filings. The TRUE side has instead pivoted to revenue stability (~$94.8B in FY2025), balance-sheet liquidity, and future optionality — but none of these rebut the fact that the earnings engine powering the entire enterprise is contracting at an accelerating rate. A buy-and-hold investor is being asked to accept that a company whose profits have fallen by three-quarters in two years represents a sound long-term commitment. That is a difficult proposition to sustain.

The FALSE side's Round 2 rebuttal directly dismantled the TRUE side's highest-scored argument (μScore 0.45) — that energy storage, FSD, Semi, robotaxi, Optimus, and related-party deals constitute diversified growth vectors that reduce concentration risk. The rebuttal demonstrated that:

- ■Energy storage, at ~$10 billion in revenue, represents roughly 10% of the top line and cannot offset automotive profit erosion even if it doubles.

- ■FSD deferred revenue exceeding $1 billion is less than 1% of total revenue.

- ■Robotaxi operates in three cities with no disclosed revenue, unit economics, or regulatory pathway.

- ■Optimus has zero commercial revenue.

- ■The $500 million from xAI/SpaceX is a non-recurring, related-party transaction.

More fundamentally, every one of these ventures depends on the same core automotive cash engine that is deteriorating. Tesla's FY2025 operating cash flow of 14.75 billion funds all R&D (6.4 billion), all CapEx ($8.53 billion), and all speculative projects. If automotive profitability continues its downward trajectory, the "catalysts" get starved of capital. This is not diversification — it is concentration risk dressed in narrative.

The FALSE side has consistently argued that Tesla's valuation — a trailing P/E exceeding 100x at any reasonable estimate of current market price — is incompatible with a buy-and-hold thesis when earnings are contracting. The TRUE side's analyst-consensus argument (μScore 0.23) cites a median price target of 450, but that target implies net income must more than double from its depressed FY2025 level of 3.86 billion. Nothing in the margin trajectory supports that assumption. When earnings decline and multiples contract simultaneously — classic double compression — permanent capital loss is the result.

No other mega-cap company carries the single-person key-risk concentration that Tesla does. Elon Musk's leadership of DOGE has entangled Tesla in partisan political warfare, triggering consumer boycotts across North America and Europe. European registrations have fallen sharply, with German sales dropping over 70% year-over-year in some months. Simultaneously, Tesla faces NHTSA investigations into FSD safety, SEC scrutiny, and trade-policy whiplash from tariffs. A buy-and-hold strategy assumes a stable risk profile; Tesla's risk profile is deteriorating in ways financial models cannot price.

An honest assessment requires acknowledging where the TRUE side has made strong points.

The balance-sheet argument is genuinely forceful. The TRUE side's Round 2 affirmative established that Tesla holds 16.6 billion in cash and equivalents, 28.1 billion in short-term investments, and only 7.6 billion in long-term debt as of Q1 2026, with stockholders' equity of 84.1 billion. This liquidity cushion means Tesla is not at risk of financial distress — it can continue funding operations and investments through cyclical pressure. The FALSE side has not disputed these figures, and they do blunt the most extreme bear case (that Tesla faces insolvency risk). However, the FALSE side's response is that balance-sheet strength does not make a stock advisable for buy-and-hold when earnings are collapsing; it merely means the company survives long enough for shareholders to experience the full extent of multiple compression.

The secular electrification trend is real. The TRUE side correctly observes that global EV adoption continues to compound, grid storage demand is rising, and Tesla is uniquely positioned across vehicles, charging, batteries, and storage. The FALSE side acknowledges this secular tailwind but notes that Tesla's market share is eroding as competitors flood the market, and the company's own margins demonstrate that participation in a growing market does not guarantee growing profits.

The R&D spending increase is notable. R&D rose from 4.5 billion (FY2024) to 6.4 billion (FY2025), signaling genuine investment in future earnings pools. The FALSE side's counter is that this spending has not yet produced a single venture that meaningfully offsets automotive earnings destruction, and the cash to fund it comes from a shrinking core.

The volatility-does-not-equal-fragility argument has merit. The TRUE side's Round 3 argument correctly notes that beta measures historical price sensitivity, not permanent capital impairment, and that Tesla's liquidity contradicts the idea that volatility alone makes the stock unsuitable. The FALSE side's response is that the bear case has never rested on beta alone — it rests on the combination of extreme valuation, collapsing earnings, and unquantifiable qualitative risk. Volatility is a symptom; the disease is earnings destruction.

The debate has converged on a clear analytical fault line. The TRUE side argues from balance-sheet resilience, secular demand, and innovation optionality — a forward-looking thesis that asks investors to look through current earnings weakness to a future where multiple ventures mature simultaneously. The FALSE side argues from the hard numbers on the income statement — a backward-and-present-looking thesis that says the earnings trajectory is so adverse, and the valuation so extreme, that no plausible future scenario justifies a buy-and-hold commitment at current prices.

The FALSE side's position has strengthened as the debate progressed because each round of updated filings revealed further earnings deterioration. The TRUE side's strongest argument — the balance sheet — is a necessary but insufficient condition for a buy-and-hold recommendation. Companies with strong balance sheets and collapsing earnings can destroy shareholder value for years. The FALSE side's central claim — that net income has fallen 74% from peak while the stock trades at triple-digit earnings multiples — remains unrebutted in substance, and it is difficult to construct a buy-and-hold thesis that does not directly address it.

Bottom-line assessment: The FALSE side has demonstrated that Tesla faces a structural earnings recession, that its "diversified catalysts" are too small to compensate, that its valuation is incompatible with its earnings trajectory, and that it carries unique political and regulatory risks. The TRUE side has demonstrated that Tesla is not financially fragile and operates in secular growth markets. On balance, the evidence favors the FALSE position: a buy-and-hold strategy requires confidence that earnings will grow over the holding period, and the data provide no basis for that confidence at current prices.

After three rounds of debate, the FALSE side has constructed a multi-axis argument that Tesla is an inadvisable buy-and-hold investment. The case rests on three pillars: accelerating fundamental deterioration, extreme overvaluation relative to vanishing growth, and a unique concentration of unquantifiable governance risks.

1. Earnings and Revenue Are in Accelerating Decline

The most powerful evidentiary finding in this debate is what the historical revenue CAGR conceals. Tesla's revenue growth has followed an unbroken deceleration path: from +70.7% (FY2021) to +51.4% (FY2022), to +18.8% (FY2023), to +0.95% (FY2024), and finally to a negative -2.93% (FY2025) — the first annual contraction. Operating income has fallen 68% from its FY2022 peak of 13.66 billion to just 4.36 billion in FY2025. Diluted EPS has been halved twice, from 4.30 (FY2023, inflated by a one-time 5.9 billion tax benefit) to 1.08 in FY2025. The TRUE side's reliance on FY2023 financials — particularly the 15 billion net income figure — is misleading because that year included a non-recurring valuation allowance release. Stripped of that item, the multi-year profit trajectory is unmistakably downward. A buy-and-hold investor is being asked to commit capital to a business where every major profit metric is deteriorating.

2. Valuation Is Detached from Fundamentals

At approximately 390.82 per share against 1.08 in trailing EPS, Tesla trades at roughly 362 times earnings. The consensus analyst target of 414.10 implies only ~6% upside, while the low target of 123 represents over 68% potential downside. Even the median target of $450 offers only ~15% upside — an extraordinarily poor risk-reward profile for a stock with a historical beta near 2.0. The TRUE side points to the consensus Buy rating, but a 6% expected return with 68% possible downside is not a compelling buy-and-hold thesis. The market is pricing Tesla as a hyper-growth disruptor while the financial statements describe a shrinking automaker.

3. The Competitive Moat Is Eroding

The TRUE side's strongest argument — Tesla's 18–20% global EV market share and durable competitive advantages — has been directly undermined. Tesla voluntarily opened its Supercharger network to Ford, GM, Rivian, and others, surrendering what was once a genuine switching-cost moat. BYD delivered over 4.25 million vehicles in 2024 against Tesla's ~1.79 million, and Chinese competitors are exporting aggressively into every major market with price points Tesla cannot match. The claimed moat of vertical integration and proprietary battery technology has not prevented revenue from shrinking.

4. Governance Risk Is Extraordinary and Unpriced

No other mega-cap company has such concentrated dependency on a single individual whose attention is now divided across Tesla, SpaceX, xAI, X, and a government advisory role. Musk's increasingly polarizing political activities have alienated a core portion of Tesla's customer base in major markets. The company's own MD&A acknowledges that trade policy uncertainty and tariffs pose risks that "could have a meaningfully adverse impact on demand." This is an unquantifiable tail risk — the possibility that leadership distraction, reputational damage, or a sudden departure could trigger a re-rating that no fundamental model can capture.

The TRUE side's strongest counter-argument concerns Tesla's financial resilience. The company does hold approximately $29 billion in cash and investments, and it has historically generated strong operating cash flow. This balance-sheet strength means Tesla is not facing existential liquidity risk, which is a meaningful point: high volatility combined with weak liquidity would be far more dangerous than high volatility alone.

The diversified growth catalyst argument also carries weight. Energy storage revenue reached 10.1 billion with 90% year-over-year growth, Full Self-Driving deferred revenue exceeds 1 billion, and the Tesla Semi has entered production. These are genuine growth vectors that exist outside the struggling automotive core, and they provide plausible pathways for future value creation that a purely automotive analysis might miss.

The TRUE side is also correct that a high beta alone does not disqualify a stock for long-term holding — many highly volatile equities (Amazon in its early years, for instance) have delivered extraordinary long-term returns. The question is whether the volatility is compensated by underlying business growth, and that is precisely where the debate turns.

The FALSE side has the stronger evidentiary position on the numbers that matter most for buy-and-hold investors: revenue trend, earnings trajectory, and valuation. The TRUE side cannot credibly dispute that revenue growth has collapsed from 70.7% to negative territory, that operating income has fallen 68%, or that the trailing P/E ratio sits at roughly 362x. The TRUE side's reliance on FY2023 financials — a year distorted by a one-time tax benefit — weakens rather than strengthens their case, because the subsequent fiscal years show unambiguous deterioration.

However, the FALSE side must acknowledge that its case is partly contingent on the continuation of current trends. If Tesla's energy storage business continues its 90% growth trajectory, if Full Self-Driving achieves genuine commercial breakthroughs, and if the Optimus robotics program materializes, the current valuation could eventually be justified by earnings that do not yet exist. The FALSE side's argument is that buy-and-hold requires betting on these unproven catalysts while the core business — which still generates the overwhelming majority of revenue — is shrinking. That is a speculation, not an investment thesis grounded in demonstrated fundamentals.

On balance, the evidence presented in this debate strongly supports the position that a buy-and-hold strategy for Tesla common stock is inadvisable at current prices. The burden of proof has not been met to demonstrate that Tesla's deteriorating core business, extreme valuation, and extraordinary governance risks are outweighed by its ancillary growth initiatives. A rational long-term investor would require either significantly lower prices or demonstrated stabilization of the automotive business before committing to a buy-and-hold strategy.

The affirmative position rests on three pillars of evidence supporting Tesla's suitability for buy-and-hold investment:

1. Financial Fortress Enables Long-Term Resilience

Tesla's balance sheet provides the stability necessary for buy-and-hold investors to withstand market turbulence. With 16.6 billion in cash against 7.6 billion in long-term debt, a debt-to-equity ratio of 0.09, and stockholders' equity that has grown 88% over three years (from 44.7B to 84.1B), Tesla possesses one of the strongest financial positions in the automotive industry. This fortress balance sheet ensures the company can fund growth, survive economic downturns, and avoid shareholder dilution—critical attributes for long-term compounding.

2. Historical Track Record Validates the Strategy

Buy-and-hold investors have been richly rewarded. IPO investors from 2010 have achieved a 2,198% return (21.5% CAGR), transforming 10,000 into 229,762 over 16 years. Even investors who purchased at the 2020 pre-split peak are up 117%. This demonstrates that Tesla's business growth has consistently overcome short-term volatility to create lasting shareholder value—the defining characteristic of successful buy-and-hold investments.

3. Structural Competitive Moats Protect Long-Term Value

Tesla's advantages are durable and difficult to replicate: 50,000+ Superchargers forming an infrastructure moat, vertical integration from batteries to software creating cost advantages, 500+ million miles of FSD data building an AI moat, and a top-10 automotive brand with 70%+ customer loyalty. These structural defenses justify a long-term investment thesis predicated on sustained competitive positioning.

The FALSE side raised legitimate concerns that merit consideration:

Volatility Risk (μScore 0.32): Tesla's beta of approximately 2.0 means the stock moves twice as much as the broader market, creating potential for significant drawdowns. This is factually accurate and represents real psychological and portfolio management challenges for investors.

Valuation Concerns (μScore 0.20): Tesla's forward P/E ratio of approximately 50 exceeds industry averages, suggesting the stock may be priced for perfection and vulnerable to multiple compression if growth disappoints.

Fundamental Questions (μScore 0.08): The opponent raised concerns about profitability consistency and debt levels, though this argument was weakened by the affirmative's presentation of actual balance sheet data.

The debate centers on a fundamental tension in investment philosophy: Is volatility synonymous with risk for long-term investors?

The affirmative position successfully demonstrated that:

- ■Tesla's volatility has been compensated with superior returns (21.5% CAGR vs. market average of ~10%)

- ■The company's financial strength ($16.6B cash, 0.09 debt-to-equity) makes volatility survivable without permanent capital impairment

- ■Professional analysts (41 with consensus Buy rating, $414.10 price target) accept the risk-reward profile

- ■Structural competitive advantages provide reasonable confidence in long-term value preservation

The opponent's strongest argument—volatility—was effectively reframed: volatility becomes risk only when investors are forced to sell during drawdowns, precisely the scenario buy-and-hold strategies avoid by design. The opponent did not successfully demonstrate that Tesla faces permanent capital impairment risk, which is the true threat to long-term investors.

Where the debate stands: The affirmative has presented stronger, more quantitatively supported arguments with higher μScores (0.57 for market dominance, 0.45 for growth catalysts). The opponent's arguments, while raising valid concerns about volatility and valuation, did not successfully rebut the core thesis that Tesla's financial strength and competitive moats make it suitable for patient, long-term investors who can tolerate price swings in exchange for potential outsized returns.

The evidence supports the conclusion that Tesla common stock is advisable for buy-and-hold investors with appropriate risk tolerance and long-term time horizons.

Round 3

Unable to produce an articulated answer.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | xiaomi/mimo-v2-flash | 0.349 | 0.134 | 36 | 6 | TRUE | FALSE | 70% |

| #2 | openai/gpt-5.5 | xiaomi/mimo-v2-flash | 0.083 | 0.000 | 405 | 6 | TRUE | TRUE | 70% |

| #3 | z-ai/glm-5 | deepseek/deepseek-v4-pro | 0.000 | 0.214 | 36 | 21 | FALSE | FALSE | 85% |

| #4 | openai/gpt-5.4-mini | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 60 | 6 | TRUE | FALSE | 78% |

| #5 | openai/gpt-5.5 | deepseek/deepseek-v4-pro | 0.000 | 0.000 | 405 | 21 | TRUE | FALSE | 85% |

| #6 | openai/gpt-5.4-mini | deepseek/deepseek-v4-pro | 0.000 | 0.000 | 60 | 21 | TRUE | FALSE | 90% |

| #7 | z-ai/glm-5 | ~moonshotai/kimi-latest | 0.000 | 0.000 | 36 | 51 | TRUE | TRUE | 85% |

| #8 | openai/gpt-5.5 | ~moonshotai/kimi-latest | 0.000 | 0.000 | 405 | 51 | TRUE | FALSE | 75% |

| #9 | openai/gpt-5.4-mini | ~moonshotai/kimi-latest | 0.000 | 0.000 | 60 | 51 | TRUE | TRUE | 60% |

The following financial data tables were referenced during the debate exchanges:

| Year | Revenue | YoY Growth | Market Share |

|---|---|---|---|

| 2020 | $31.5B | — | ~16% |

| 2021 | $53.8B | +71% | ~18% |

| 2022 | $81.5B | +52% | ~19% |

| 2023 | $96.8B | +19% | ~19% |

| 2024 | $97.7B | +1% | ~18% |

Legend: Tesla annual revenue and estimated global EV market share (2020-2024). Revenue in USD billions. Source: SEC filings and industry estimates.

</FinancialData>

| Period | Max Drawdown | Period Return | Holding Strategy Result |

|---|---|---|---|

| 2020-2022 | -38% | +700%+ | Highly profitable |

| 2022-2023 | -65% | -65% | Recovered by 2024 |

| 2020-2026 | -65% (worst) | +800%+ | Exceptional gains |

Legend: Tesla stock performance showing drawdowns versus buy-and-hold returns (Jan 2020 - May 2026). Source: historical price data.

| Factor | TRUE Side Strength | FALSE Side Strength | Winner |

|---|---|---|---|

| Revenue Growth & Scale | Strong (0.57) | Weak (0.08) | TRUE |

| Growth Catalysts | Strong (0.45) | Not contested | TRUE |

| Volatility Concerns | Reframed successfully | Moderate (0.32) | TRUE |

| Valuation Premium | Acknowledged | Moderate (0.20) | Inconclusive |

| Analyst Consensus | Moderate (0.23) | Not contested | TRUE |

Legend: Comparative assessment of debate arguments by factor, with μScore indicating argument strength. Higher scores indicate stronger, more complete arguments.

</FinancialData>

| Fiscal Year | Revenue ($B) | YoY Growth % |

|---|---|---|

| 2020 | $31.5 | +28% |

| 2021 | $53.7 | +71% |

| 2022 | $81.5 | +51% |

| 2023 | $96.8 | +19% |

| 2024 | $97.7 | +1% |

| 2025 | $94.8 | -3% |

Legend: Tesla annual revenue in USD billions from FY2020-FY2025. Source: SEC 10-K filings.

</FinancialData>

| Metric | Value |

|---|---|

| Current Price | $390.82 |

| Consensus Target | $414.10 |

| Target Upside | +5.9% |

| High Target | $600.00 |

| Median Target | $450.00 |

| Recommendation | Buy |

| Recommendation Score | 2.36 |

| Number of Analysts | 41 |

Legend: Tesla analyst consensus estimates and price targets. Source: analyst coverage data, May 2026.

</FinancialData>

| Year | Net Income ($B) | Operating Margin % |

|---|---|---|

| 2020 | $0.72 | 4.1% |

| 2021 | $5.5 | 12.1% |

| 2022 | $12.6 | 16.8% |

| 2023 | $15.0 | 9.6% |

| 2024 | $7.1 | 7.3% |

| 2025 | $3.8 | 4.0% |

Legend: Tesla net income and operating margin from FY2020-FY2025. Source: SEC filings.

</FinancialData>

| Metric | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|

| Diluted EPS | $3.62 | $4.30 | $2.04 | $1.08 |

| Net Income | $12.56B | $15.00B | $7.09B | ~$3.5B |

| Operating Income | $13.66B | $8.89B | $7.08B | — |

| Gross Profit | $20.85B | $17.66B | $17.45B | — |

Legend: Tesla annual earnings trajectory showing multi-year deterioration across all profit metrics. EPS declined 75% from FY2023 peak ($4.30) to FY2025 ($1.08). Net income and operating income show similar compression. Source: SEC 10-K and 10-Q filings.

</FinancialData>

| Risk Metric | Tesla | S&P 500 | Interpretation |

|---|---|---|---|

| Beta | ~2.0 | 1.0 | Higher volatility |

| Analyst Consensus | Buy (2.36) | N/A | Professional approval |

| Target Upside (Median) | +15.2% | N/A | Expected positive returns |

| 5-Year Total Return | +1,150% | +85% | Volatility rewarded |

Legend: Tesla risk metrics compared to market benchmarks. Analyst data from 41 covering analysts, May 2026.

</FinancialData>

| Segment | FY2022 | FY2023 | FY2024 | FY2025 | 2-Year Change |

|---|---|---|---|---|---|

| Automotive Revenue | $71.5B | $82.4B | $77.1B | $69.5B | -15.6% |

| Energy & Storage | $3.9B | $6.0B | $10.1B | $12.8B | +111.5% |

| Services & Other | $6.1B | $8.3B | $10.5B | $12.5B | +50.6% |

| Total Revenue | $81.5B | $96.8B | $97.7B | $94.8B | -2.1% |

Legend: Tesla revenue by business segment, FY2022–FY2025. Automotive revenue — the core business — declined 15.6% from its FY2023 peak. Total revenue turned negative in FY2025. Source: SEC 10-K filings, segment reporting.

</FinancialData>

| Estimate Metric | 90 Days Ago | 60 Days Ago | 30 Days Ago | Current | Change |

|---|---|---|---|---|---|

| FY2027 EPS Consensus | $2.90 | $2.80 | $2.81 | $2.54 | -12.5% |

| FY2027 Rev. Consensus | — | — | — | $119.6B | — |

| FY2026 EPS Consensus | $2.10 | $2.08 | $2.08 | $2.08 | -0.7% |

| FY2026 Rev. Consensus | — | — | — | $102.3B | — |

| FY2027 EPS Revisions (30d) | — | — | — | 3 Up / 18 Down | — |

| FY2026 EPS Revisions (30d) | — | — | — | 5 Up / 17 Down | — |

Legend: Tesla analyst EPS estimate trajectory and revision activity. FY2027 consensus EPS has fallen 12.5% over 90 days. Downward revisions outnumber upward revisions by 6:1 for FY2027 and 3.4:1 for FY2026. Source: consensus estimate data, May 2026.

</FinancialData>

| Metric | 2020 | 2024 | Change |

|---|---|---|---|

| Revenue | $31.5B | $97.7B | +210% |

| Net Income | $0.7B | $15.0B | +1,980% |

| Market Share (US EV) | ~65% | ~55% | Dominant |

Legend: Tesla key financial metrics showing growth trajectory. Source: SEC filings.

</FinancialData>

| Factor | Assessment | Weight |

|---|---|---|

| Historical Growth | Strong positive | High |

| Profitability Track Record | Strong positive | High |

| Analyst Consensus | Positive | Medium |

| Volatility Risk | Mitigated by history | Medium |

| Near-Term Fundamentals | Negative | Medium |

| Valuation Premium | Concerning | Low-Medium |

| Competitive Position | Mixed | Medium |

| Overall Assessment | Advisable for long-term holders | — |

Legend: Weighted assessment of buy-and-hold thesis for Tesla. Based on debate evidence and financial data through May 2026.

</FinancialData>

| Metric | FY2023 (Peak) | FY2024 | FY2025 | FY2026E | FY2027E | Change (Peak to FY2027E) |

|---|---|---|---|---|---|---|

| Diluted EPS | $4.30 | $2.04 | $1.66 | $1.93 | $2.45 | -43% |

| Net Income | $15.0B | $7.1B | ~$3.5B | ~$4.7B | ~$7.3B | -51% |

| Automotive Revenue | $82.4B | $77.1B | $69.5B | — | — | -15.6% |

| Operating Margin | 9.6% | 7.3% | ~4.0% | — | — | -5.6pp |

| P/E Ratio (at $390.82) | 91x | 192x | 236x | 202x | 159x | — |

Legend: Tesla key financial metrics showing peak-to-current deterioration. FY2025 figures are based on analyst consensus estimates. FY2026E–FY2027E are consensus estimates. Even by FY2027, EPS remains 43% below FY2023 peak. Source: SEC filings and consensus estimate data, May 2026.

</FinancialData>

| Evidence | Figure |

|---|---|

| Analyst consensus rating | Buy |

| 12-month consensus price target | $414.10 |

| Median target | $450.00 |

| Current price | $390.82 |

| Analysts covering TSLA | 41 |

Legend: Current sell-side consensus snapshot for TSLA. USD per share, as reported in the latest consensus compilation.

</FinancialData>

| Metric | FY2022 | FY2023 | FY2024 | 2-Year Change |

|---|---|---|---|---|

| Revenue | $81.46B | $96.77B | $97.69B | +19.9% |

| Gross Profit | $20.85B | $17.66B | $17.45B | −16.3% |

| Net Income | $12.56B | $15.00B | $7.09B | −43.5% |

| Gross Margin | 25.60% | 18.25% | 17.86% | −7.74 pp |

Legend: Tesla Inc. annual revenue, gross profit, net income, and gross margin for fiscal years 2022–2024. Revenue in USD billions. Net income is Net Income Attributable to Parent. Source: SEC 10-K filings (accession 0001628280-25-003063 and related filings).

</FinancialData>

| Metric | FY2022 | FY2023 | FY2024 | FY2025 | Peak-to-Trough |

|---|---|---|---|---|---|

| Net Income | $12.58B | $15.00B | $7.13B | $3.86B | −74.3% |

| Operating Cash Flow | $14.72B | $13.26B | $14.92B | $14.75B | — |

| Free Cash Flow | $7.55B | $4.36B | $3.58B | $6.22B | −52.6% |

| CapEx | $7.16B | $8.90B | $11.34B | $8.53B | — |

Legend: Tesla Inc. annual net income, operating cash flow, free cash flow, and capital expenditures for FY2022–FY2025. Net income is Net Income Attributable to Parent. All figures in USD billions. Source: SEC 10-K filings (accession numbers 0001628280-24-002826, 0001628280-25-003063, 0001628280-26-003952).

</FinancialData>

| Metric | Evidence Presented |

|---|---|

| FY2024 revenue | $97.7B |

| FY2024 operating cash flow | $14.9B |

| FY2024 free cash flow | $3.6B |

| Year-end 2024 cash, cash equivalents, and investments | $36.6B |

| Energy generation and storage revenue growth | +90% YoY |

Legend: Key Tesla operating and liquidity metrics presented in the debate, primarily from FY2024 company filings. Amounts in USD; YoY = year over year.

</FinancialData>

| Metric | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|

| Revenue | $81.46B | $96.77B | $97.69B | $94.83B |

| Gross Profit | $20.85B | $17.66B | $17.45B | $17.09B |

| Operating Income | $13.66B | $8.89B | $7.08B | $4.36B |

| Net Income | $12.56B | $15.00B* | $7.09B | $3.79B |

| Diluted EPS | $3.62 | $4.30* | $2.04 | $1.08 |

*Legend: Tesla annual financial performance FY2022–FY2025. FY2023 net income and EPS include a one-time ~$5.9B non-cash tax benefit from valuation allowance release. Source: SEC 10-K filings.

</FinancialData>

| Valuation Metric | Value |

|---|---|

| Current Price | $390.82 |

| Trailing P/E (FY2025 EPS $1.08) | ~362x |

| Consensus Target | $414.10 |

| Upside to Consensus | ~6.0% |

| Median Target | $450.00 |

| Low Target | $123.00 |

| Potential Downside to Low | ~68.5% |

| Analyst Count | 41 |

Legend: Tesla valuation and analyst consensus data as of May 2026. Trailing P/E calculated using FY2025 diluted EPS of $1.08. Source: consensus estimates and SEC filings.

</FinancialData>

| Fiscal Year | Revenue | YoY Growth |

|---|---|---|

| FY2021 | $53.82B | +70.7% |

| FY2022 | $81.46B | +51.4% |

| FY2023 | $96.77B | +18.8% |

| FY2024 | $97.69B | +0.95% |

| FY2025 | $94.83B | -2.93% |

Legend: Tesla annual revenue and year-over-year growth rate, FY2021–FY2025. Revenue in USD billions. Source: SEC 10-K filings and income growth data.

</FinancialData>

| Metric | 2022 | 2023 | 2024 | Q1 2026 |

|---|---|---|---|---|

| Cash & Equivalents ($B) | $16.3 | $16.4 | $16.1 | $16.6 |

| Long-term Debt ($B) | $1.0 | $2.7 | $5.5 | $7.6 |

| Stockholders' Equity ($B) | $44.7 | $62.6 | $72.9 | $84.1 |

| Debt-to-Equity Ratio | 0.02 | 0.04 | 0.08 | 0.09 |

Legend: Tesla's balance sheet metrics showing cash position, debt levels, and equity growth (2022–Q1 2026). Values in USD billions. Source: SEC 10-K and 10-Q filings.

</FinancialData>

| Investment Scenario | Initial Investment | Current Value | Total Return | CAGR |

|---|---|---|---|---|

| IPO Investor (2010) | $10,000 | $229,762 | +2,198% | 21.5% |

| 2020 Peak Buyer | $10,000 | $21,700 | +117% | 15.2% |

| 5-Year Holder (2021) | $10,000 | $13,852 | +38.5% | 6.7% |

Legend: Hypothetical buy-and-hold returns for Tesla investors at different entry points. Current price: $390.82 (as of May 2026). CAGR = Compound Annual Growth Rate. Source: Historical price data and current market prices.

</FinancialData>

| Competitive Moat | Tesla Position | Competitive Barrier |

|---|---|---|

| Supercharger Network | 50,000+ stalls globally | Capital-intensive, requires years to replicate |

| Vertical Integration | Battery cells, software, manufacturing | Cost advantage, supply chain control |

| FSD Data Advantage | 500M+ real-world miles | Proprietary training data for AI development |

| Brand Value | #8 global automotive brand | 70%+ customer loyalty rate |

Legend: Tesla's structural competitive advantages and barriers to entry. Data compiled from company reports and industry analysis. Source: Company disclosures and industry research.

| Metric | Value | Implication for Buy-and-Hold |

|---|---|---|

| Beta | ~2.0 | Higher expected returns per CAPM |

| 16-Year CAGR | 21.5% | Volatility rewarded with superior returns |

| Analyst Consensus | Buy (2.36 mean) | Professionals accept risk-reward profile |

| Price Target | $414.10 | +5.9% upside from $390.82 |

| Cash Position | $16.6B | Survives volatility without dilution |

| Debt-to-Equity | 0.09 | Minimal financial distress risk |

Legend: Key metrics demonstrating that Tesla's volatility is compensated and survivable for buy-and-hold investors. Source: Market data and analyst consensus estimates as of May 2026.

</FinancialData>

| Period | Total Revenue ($B) | YoY Revenue Growth | Automotive Revenue Growth |

|---|---|---|---|

| 2022 | $81.5 | +51% | — |

| 2023 | $96.8 | +19% | +15% |

| 2024 | $97.7 | +1% | -6% |

| Q1 2026 | ~$19.3 | -5%* | -8%* |

*Legend: Tesla revenue growth deceleration and automotive segment contraction (2022–Q1 2026). Q1 2026 figures represent estimated or reported quarterly trends showing continued decline. Revenue in USD billions. Source: Company SEC filings and earnings reports.

</FinancialData>

| Year | Tesla Global EV Market Share | BYD Global EV Market Share | Tesla Share Change |

|---|---|---|---|

| 2020 | ~20% | ~8% | — |

| 2022 | ~18% | ~12% | -2 pp |

| 2024 | ~14% | ~18% | -4 pp |

| 2025* | ~12% | ~20% | -2 pp |

*Legend: Global battery-electric vehicle (BEV) market share trends showing Tesla's decline versus BYD's ascent. 2025 figures based on trailing sales data and industry estimates. pp = percentage points. Source: Industry sales trackers and automotive market research.

</FinancialData>

| Metric | Tesla FY2024 |

|---|---|

| Revenue | $97.69B |

| Net income attributable to common stockholders | $7.09B |

| Net cash provided by operating activities | $14.92B |

| Cash, cash equivalents, and investments | $36.56B |

| Automotive debt, excluding vehicle and energy product financing | $0.00B |

Legend: Selected FY2024 Tesla financial durability metrics. USD billions; debt figure refers to automotive debt excluding product-financing obligations.

</FinancialData>

| Metric | Tesla FY2024 |

|---|---|

| Revenue | $97.69B |

| Net income attributable to common stockholders | $7.09B |

| Net cash provided by operating activities | $14.92B |

| Cash, cash equivalents, and investments | $36.56B |

| Automotive debt, excluding vehicle and energy product financing | $0.00B |

Legend: Selected Tesla FY2024 financial strength indicators. USD billions. Source period: fiscal year ended Dec. 31, 2024.

</FinancialData>

| Metric | Reported Figure |

|---|---|

| Energy storage deployments in 2023 | 14.72 GWh |

| FY2023 R&D expense | $3.97B |

| FY2024 R&D expense | $4.54B |

Legend: Tesla energy-storage deployment and research spending figures. GWh = gigawatt-hours; R&D in USD billions.

</FinancialData>

| Global EV Adoption Indicator | 2023 Figure |

|---|---|

| Global electric car sales | Nearly 14 million |

| EV share of global car sales | About 18% |

Legend: Global electric vehicle adoption indicators for 2023. EV = electric vehicle.

</FinancialData>

| Assumed TSLA Stock Path | Modeled 1-Year $250 Call Value |

|---|---|

| $200 | $21.26 |

| $250 | $41.00 |

| $300 | $68.19 |

| $350 | $104.49 |

| Volatility assumption | 42.97% |

Legend: Modeled one-year call-option values using a $250 strike, 365 days to expiry, and a 5% risk-free rate. Values are in USD per option share equivalent.

</FinancialData>

| Company / Sector | Forward P/E (approx.) | 5-Year Revenue CAGR |

|---|---|---|

| Tesla (TSLA) | ~50x | ~28% |

| Toyota (TM) | ~8x | ~5% |

| Volkswagen (VWAGY) | ~4x | ~3% |

| S&P 500 Consumer Discretionary | ~22x | ~6% |

Legend: Forward valuation multiples and historical revenue growth for Tesla versus legacy auto peers and sector benchmarks. P/E ratios based on consensus forward earnings estimates. Revenue CAGR reflects trailing five-year annualized growth.

</FinancialData> The affirmative argument that volatility creates "upside optionality" through call-option mathematics conflates derivative pricing with equity risk. A buy-and-hold investor owns the underlying equity, not a leveraged option; permanent drawdowns in the stock price represent real wealth destruction that cannot be recovered by volatility smiles. When a company trades at 50 times forward earnings in a cyclical, capital-intensive industry, the margin of safety required for long-term holding is absent. History demonstrates that even quality businesses destroy shareholder value for decades when purchased at excessive multiples.

| Metric | Tesla FY2024 | Tesla FY2025 |

|---|---|---|

| Revenue | $97.69B | $94.83B |

| Operating Cash Flow | $14.92B | $14.75B |

| R&D Expense | $4.54B | $6.41B |

Legend: Tesla revenue, operating cash flow, and R&D investment for fiscal years 2024 and 2025. USD billions. FY2025 figures reflect the most recent annual period.

</FinancialData> The decline in revenue from FY2024 to FY2025, despite substantial R&D increases, undermines the claim of an inflection point in new businesses. Operating cash flow remained flat even as the company poured billions into autonomy and robotics—suggesting that these "embedded options" are already consuming capital without generating offsetting revenue. Buy-and-hold investing requires confidence that reinvested earnings will produce superior returns; Tesla’s current trajectory shows cash flow stagnation amid rising investment, a pattern inconsistent with compounder economics.

| Fiscal year | Revenue growth | Gross profit growth | Operating income growth | Net income growth |

|---|---|---|---|---|

| 2021 | +70.7% | +105.2% | +227.1% | +666.2% |

| 2022 | +51.4% | +53.3% | +109.4% | +127.8% |

| 2023 | +18.8% | -15.3% | -34.9% | +19.2% |

| 2024 | +0.9% | -1.2% | -20.4% | -52.5% |

| 2025 | -2.9% | -2.0% | -38.5% | -46.8% |

Legend: Annual income-statement growth for TSLA across recent fiscal years, showing the company’s explosive scale-up followed by slower but still large revenue base. Percentages are year-over-year changes.

Source URL: company annual financial statements

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: price_option_path

{"option_path": [21.260799467795138, 41.00217361510525, 68.1894476730588, 104.48510492342763], "volatility_used": 0.42966723414218255, "symbol": "TSLA"}

MCP tool: get_option_chain

No options data available.

RAW_JSON: []

PLOTLY_SPEC: {"data": [], "layout": {}}

D3_DATA_SPEC: {"nodes": [], "type": "option_curve_v1", "config": {"strikeDomain": [0, 100], "colorMap": {"CALL": "#2da44e", "PUT": "#cf222e"}}}

MCP tool: price_option_path

{"option_path": [48.03519626791075, 56.13423770250952, 75.85870990989378], "volatility_used": 0.42966723414218255, "symbol": "TSLA"}

MCP tool: price_option_path

{"option_path": [15.841450017706023, 20.989261253356972, 28.2681945570003, 46.88864678807556, 70.33979699954045], "volatility_used": 0.42966723414218255, "symbol": "TSLA"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.