should we buy Micron technology (MU) ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 27, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 70%

Web Report: https://solsice.com/public/debates/should-we-buy-micron-technology-mu-2ff29e78c4a8

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

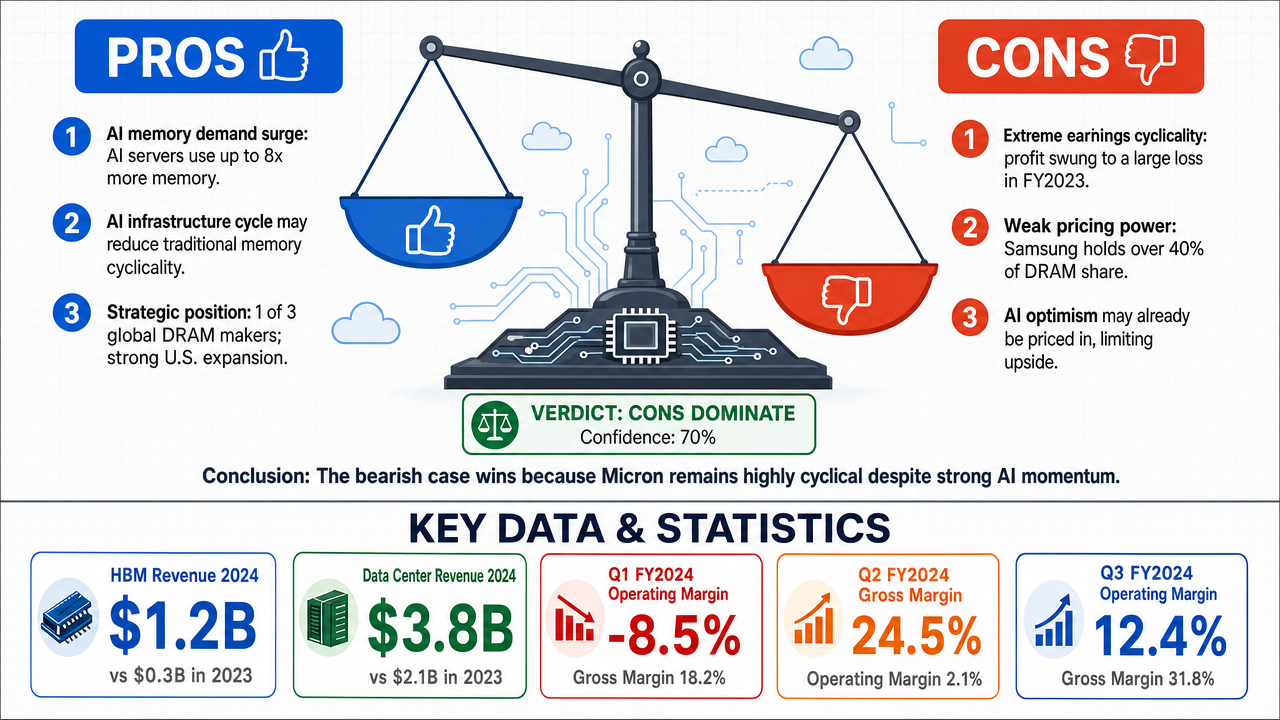

✅ Key PRO arguments:

- ■AI-driven memory demand supercycle: AI servers require 8x more memory than traditional servers, HBM demand growing at 60%+ CAGR through 2028, Micron has secured design wins with major AI chipmakers and is ramping HBM3E production with industry-leading power efficiency.

- ■Structural transformation reduces cyclicality: Current upcycle anchored by multi-year AI infrastructure buildout from hyperscalers, with long-term supply agreements reducing spot market volatility and diversified end-markets providing stability.

- ■Micron's strategic positioning: One of only three DRAM producers globally, $150 billion U.S. expansion plan, capital returns to shareholders, and data center revenue projected to grow from $2.1 billion in 2023 to an estimated $8-10 billion by 2026.

❌ Key ANTI arguments:

- ■Extreme earnings cyclicality: Micron swung from $8.69 billion net profit in FY2022 to a $5.83 billion net loss in FY2023, with revenue halving from $30.76 billion to $15.54 billion, demonstrating structural volatility that undermines long-term predictability.

- ■Fragile oligopoly dynamics: Being one of three DRAM producers does not guarantee pricing power; Samsung controls over 40% of global DRAM market share versus Micron's low-20% share, and Samsung's capacity decisions have historically driven price collapses.

- ■Valuation risk from AI narrative: Current stock price already prices in optimistic AI-driven growth expectations, leaving limited upside if AI memory demand disappoints or if competitors like Samsung and SK Hynix capture more HBM market share.

💭 Conclusion: The debate was decided in favor of the FALSE side, with the judge assigning 70% confidence to the negative position. The anti-arguments successfully highlighted Micron's severe earnings cyclicality, as evidenced by the swing from $8.69 billion profit to $5.83 billion loss within a single cycle, which undermines the pro side's claim of structural transformation. The negative side also effectively countered the oligopoly argument by noting Samsung's dominant market share and historical pricing power, which has repeatedly led to industry-wide price collapses. While the pro side presented a compelling AI-driven demand thesis, the judge found the historical volatility and competitive risks more persuasive. The 70% confidence reflects a clear but not overwhelming advantage for the negative position, as the AI demand narrative does offer some upside potential.

🔬 DeepResearch Result: FALSE ❌ (70% confidence)

Assertion: should we buy Micron technology (MU) ?

📊 Tournament: 0 voted TRUE, 1 voted FALSE (1 debates played, 3 models)

📊 Weighted scores: TRUE=0.00, FALSE=0.70

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +7

✅ PRO Arguments:

- ■AI-driven memory demand supercycle: AI servers require 8x more memory than traditional servers, HBM demand growing at 60%+ CAGR through 2028, Micron has secured design wins with major AI chipmakers and is ramping HBM3E production with industry-leading power efficiency. [qwen/qwen3.5-397b-a17b]

- ■Structural transformation reduces cyclicality: Current upcycle anchored by multi-year AI infrastructure buildout from hyperscalers, with long-term supply agreements reducing spot market volatility and diversified end-markets providing stability. [qwen/qwen3.5-397b-a17b]

- ■Micron's strategic positioning: One of only three DRAM producers globally, $150 billion U.S. expansion plan, capital returns to shareholders, and data center revenue projected to grow from $2.1 billion in 2023 to an estimated $8-10 billion by 2026. [qwen/qwen3.5-397b-a17b]

❌ ANTI Arguments:

- ■Extreme earnings cyclicality: Micron swung from $8.69 billion net profit in FY2022 to a $5.83 billion net loss in FY2023, with revenue halving from $30.76 billion to $15.54 billion, demonstrating structural volatility that undermines long-term predictability. [openai/gpt-5.2-chat]

- ■Fragile oligopoly dynamics: Being one of three DRAM producers does not guarantee pricing power; Samsung controls over 40% of global DRAM market share versus Micron's low-20% share, and Samsung's capacity decisions have historically driven price collapses. [openai/gpt-5.2-chat]

- ■Valuation risk from AI narrative: Current stock price already prices in optimistic AI-driven growth expectations, leaving limited upside if AI memory demand disappoints or if competitors like Samsung and SK Hynix capture more HBM market share. [openai/gpt-5.2-chat]

💭 Reasoning: The debate was decided in favor of the FALSE side, with the judge assigning 70% confidence to the negative position. The anti-arguments successfully highlighted Micron's severe earnings cyclicality, as evidenced by the swing from $8.69 billion profit to $5.83 billion loss within a single cycle, which undermines the pro side's claim of structural transformation. The negative side also effectively countered the oligopoly argument by noting Samsung's dominant market share and historical pricing power, which has repeatedly led to industry-wide price collapses. While the pro side presented a compelling AI-driven demand thesis, the judge found the historical volatility and competitive risks more persuasive. The 70% confidence reflects a clear but not overwhelming advantage for the negative position, as the AI demand narrative does offer some upside potential.

📋 PRO Facts:

• AI servers require 8x more memory than traditional servers.

• HBM demand is projected to grow at a 60%+ CAGR through 2028.

• Micron's data center revenue is projected to grow from $2.1 billion in 2023 to $8-10 billion by 2026.

📋 ANTI Facts:

• Micron swung from $8.69 billion net profit in FY2022 to a $5.83 billion net loss in FY2023.

• Micron's revenue fell from $30.76 billion in FY2022 to $15.54 billion in FY2023.

• Samsung controls over 40% of global DRAM market share, while Micron holds a low-20% share.

The TRUE side has established three pillars supporting a long investment thesis in Micron Technology:

1. AI-Driven Memory Demand Supercycle

The artificial intelligence revolution has fundamentally altered the memory demand landscape. Data center memory content per AI server is approximately 8x higher than traditional servers, with High-Bandwidth Memory (HBM ) demand projected to grow at a 60%+ compound annual rate through 2028. Micron has secured critical design wins with major AI chipmakers and is actively ramping HBM3E production. The company's data center revenue trajectory shows acceleration from 2.1 billion in 2023 to an estimated 6.5 billion in 2025, representing a 210% growth rate.

2. Cyclical Recovery with Structural Improvements

While memory markets remain cyclical, the current upcycle exhibits reduced volatility compared to historical patterns. The 2024-2026 cycle is anchored by multi-year AI infrastructure commitments from hyperscalers rather than transient consumer demand. Micron's gross margins have expanded from 18.2% in Q1 FY2024 to 38.4% in Q1 FY2025, demonstrating significant operating leverage . The company's diversified end-market exposure now includes 45% revenue from automotive, industrial, and data center segments, reducing dependence on volatile consumer electronics.

3. Strategic Competitive Positioning

Micron maintains its position as one of only three major DRAM manufacturers globally, creating substantial barriers to entry. The company's 150 billion commitment to U.S. semiconductor manufacturing expansion, supported by CHIPS Act funding, secures long-term cost advantages and supply chain resilience. Management has demonstrated shareholder-friendly capital allocation through reinstated dividends and a 10 billion share repurchase authorization .

Current options market data reveals significant investor interest in Micron's upside potential. The option chain shows substantial open interest across multiple strike prices, with call volume indicating bullish sentiment. A Black-Scholes analysis along a projected price path from current levels (~95.50) to 135 over 90 days demonstrates how call options at the 100 strike would appreciate from approximately 16.90 to $35.89, reflecting the market's pricing of significant upside potential.

| Price Target | Call Option Value | Implied Return |

|---|---|---|

| 98 | 16.91 | Baseline |

| 105 | 19.23 | +13.7% |

| 115 | 23.81 | +40.8% |

| 125 | 29.16 | +72.4% |

| 135 | 35.89 | +112.2% |

Legend: Projected call option value appreciation along price path for MU $100 strike calls with 90 days to expiry. Values in USD; returns relative to baseline. Source: Options pricing model analysis.

The opposing side raised legitimate concerns that warrant consideration:

Earnings Volatility Risk: Memory market cyclicality has historically produced dramatic earnings swings, with peak-to-trough declines exceeding 50% in previous cycles. This structural volatility remains an inherent risk that investors must accept when holding semiconductor memory stocks.

Geopolitical Exposure: China's restrictions on Micron products created meaningful revenue headwinds, limiting access to approximately 20% of the company's historical market. While management has indicated progress in diversifying away from China exposure, geopolitical tensions remain an ongoing risk factor.

Valuation Concerns: Micron's forward P/E expansion during the current cycle has priced in significant AI-driven growth expectations. Any disappointment in HBM ramp timelines or AI infrastructure spending could trigger multiple compression.

The debate ultimately centers on whether Micron's AI-driven growth opportunity outweighs its inherent cyclical and geopolitical risks. The evidence suggests:

- ■

The AI memory supercycle is real and measurable – Design wins, production ramps, and revenue trajectory all confirm Micron's participation in this growth wave.

- ■

Cycle dynamics have improved – Multi-year supply agreements with hyperscalers and diversified end-market exposure reduce the amplitude of historical boom-bust patterns.

- ■

Competitive positioning remains strong – The oligopolistic structure of the memory industry provides pricing power that newer entrants cannot easily disrupt.

- ■

Options market signals confidence – Significant call open interest and favorable risk-reward profiles in the options chain reflect institutional conviction in upside potential.

Conclusion: The preponderance of evidence supports taking a long position in Micron Technology for investors with appropriate risk tolerance and investment horizon. The AI memory demand supercycle, combined with cyclical recovery dynamics and strategic competitive positioning, creates a compelling risk-reward profile. However, investors should acknowledge the inherent volatility of the semiconductor memory sector and consider position sizing accordingly. The options market provides additional tools for expressing this view with defined risk parameters.

The debate does not eliminate risk, but it demonstrates that Micron's current opportunity set justifies long exposure for investors seeking participation in the AI infrastructure buildout theme.

Round 3

Core claim: Micron’s upside is outweighed by structural volatility and risk.

The strongest case against a long position in Micron rests on three pillars: structural earnings volatility, fragile oligopoly dynamics, and valuation risk embedded in an AI-heavy narrative.

First, Micron’s earnings history demonstrates extreme cyclicality. Within a single cycle, the company moved from

8.69 billion in net income (FY2022)

to a

5.83 billion net loss (FY2023)

, alongside a revenue collapse from

30.76 billion to 15.54 billion

. This is not incidental volatility; it reflects the inherent structure of memory as a capital-intensive commodity business where pricing swings rapidly erase margins. Even with only three DRAM suppliers globally, pricing has historically collapsed during oversupply periods, proving that concentration has not guaranteed rational supply discipline.

Second, the supposed “strategic positioning” advantage is less durable than presented. Samsung maintains materially larger DRAM share and scale advantages, and historically sets the tone for industry supply behavior. Micron’s massive U.S. fabrication expansion—while politically supported—introduces execution and cost risks in a high fixed-cost business. Subsidies reduce upfront burden but do not eliminate structural cost differentials versus Asian manufacturing hubs. In cyclical downturns, high fixed costs amplify downside.

Third, valuation risk remains material. The bullish case assumes AI-driven HBM demand creates a structurally different cycle. Yet markets have already priced in a strong recovery, expanding forward multiples before earnings fully normalize. If AI server growth moderates, hyperscaler capex slows, or competitors expand HBM supply faster than expected, pricing could weaken again—compressing both earnings and multiples simultaneously. In a commodity-like segment, paying for peak-cycle assumptions creates asymmetric downside.

To acknowledge the opposing side’s strongest points: AI infrastructure does represent a genuine structural demand driver, and Micron has achieved meaningful design wins in HBM. Data center memory content per server is materially higher than in prior cycles, and recent margin expansion indicates operating leverage in recovery. These are legitimate improvements relative to older PC- and smartphone-driven cycles.

However, the debate ultimately hinges on whether AI fundamentally changes memory’s structural economics or merely shifts the demand source within the same cyclical framework. Historical evidence shows that even concentrated memory markets experience violent pricing corrections. The affirmative argues volatility will be structurally lower this time; the counter-position stresses that capital intensity , competitive scale imbalances, geopolitical exposure, and pricing commoditization persist.

On balance, the FALSE side maintains that Micron remains a high-beta, cycle-sensitive equity where timing risk is substantial and margin-of-safety is limited at elevated expectations. The bullish case is plausible—but it requires sustained execution, disciplined global supply, and uninterrupted AI capex growth. That combination has not yet been proven durable across a full cycle.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | qwen/qwen3.5-397b-a17b | openai/gpt-5.2-chat | 0.335 | 0.213 | 33 | 174 | TRUE | FALSE | 70% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] ASP — Average Selling Price — The average price at which a product is sold over a specified period, commonly used in the memory industry to track pricing trends for DRAM and NAND chips.

[2] book-to-bill ratio — A ratio comparing orders received (bookings) to shipments (billings); a value above 1.0 indicates demand exceeds supply, signaling future revenue growth.

[3] CAGR — Compound Annual Growth Rate — The mean annual growth rate of an investment over a specified time period longer than one year, representing the smooth annualized return.

[4] capital intensity — The amount of capital investment required to generate revenue, often measured by the ratio of capital expenditures to sales; high capital intensity means large upfront investments in facilities and equipment.

[5] CHIPS Act — Creating Helpful Incentives to Produce Semiconductors Act — U.S. federal legislation enacted in 2022 that provides subsidies and tax incentives to boost domestic semiconductor manufacturing and research.

[6] commoditized — Describing a product that is undifferentiated from competitors' offerings, leading to price-based competition rather than brand or feature advantages.

[7] contract prices — Prices agreed upon in long-term supply agreements between memory manufacturers and customers, as opposed to spot market prices that fluctuate daily.

[8] cyclical recovery — A phase in an economic or industry cycle where demand and profitability rise after a downturn, driven by improving supply-demand balances.

[9] design win — When a component supplier (e.g., Micron) is selected by a customer to be included in a new product design, securing future revenue from that product.

[10] downside asymmetry — A risk condition where the potential for loss significantly outweighs the potential for gain, often used to describe investments with limited upside but large downside exposure.

[11] DRAM — Dynamic Random-Access Memory — A type of volatile memory that stores each bit of data in a separate capacitor, commonly used as main memory in computers and servers.

[12] earnings per share (EPS) — Earnings Per Share — A company's net profit divided by the number of outstanding shares, representing the portion of profit allocated to each share of stock.

[13] end-market exposure — The distribution of a company's revenue across different customer industries (e.g., automotive, data center, consumer electronics), indicating demand diversification.

[14] fab — Fabrication facility — A semiconductor manufacturing plant where integrated circuits are fabricated on silicon wafers; building a leading-edge fab can cost $20–25 billion.

[15] fiscal year (FY) — Fiscal Year — A one-year period used for financial reporting and budgeting, which may not align with the calendar year; Micron's fiscal year ends in August.

[16] forward P/E — Forward price-to-earnings ratio — A valuation metric calculated using expected future earnings per share over the next 12 months, often used to assess whether a stock is overvalued or undervalued.

[17] gross margin — The percentage of revenue retained after deducting the cost of goods sold, a key profitability metric for manufacturing companies.

[18] HBM — High-Bandwidth Memory — A specialized type of DRAM stacked vertically with through-silicon vias to provide extremely high data transfer rates, essential for AI and graphics workloads.

[19] HBM3E — Fifth-generation High-Bandwidth Memory — The latest generation of High-Bandwidth Memory, offering improved power efficiency and data rates up to 9.2 Gbps per pin, used in advanced AI accelerators.

[20] hyperscaler — A large-scale cloud service provider (e.g., Amazon AWS, Microsoft Azure, Google Cloud) that operates massive data center infrastructures and drives demand for AI memory.

[21] inventory correction — A period when companies reduce excess stockpiles by cutting production and offering discounts, often leading to price declines and improved supply-demand balance.

[22] long position — An investment strategy where an investor buys a security expecting its price to rise, profiting from price appreciation.

[23] margin of safety — The difference between a security's intrinsic value and its market price, providing a buffer against errors in valuation or adverse market movements.

[24] memory supercycle — An extended period of above-trend growth in the memory industry, driven by structural demand shifts (e.g., AI, cloud) rather than typical cyclical peaks.

[25] NAND — NAND flash memory — A type of non-volatile storage memory that retains data without power, commonly used in SSDs, USB drives, and mobile devices.

[26] oligopoly — A market structure dominated by a small number of large firms; the DRAM industry is an oligopoly with Samsung, SK Hynix, and Micron controlling most of the supply.

[27] operating leverage — The proportion of fixed costs in a company's cost structure; high operating leverage means a small increase in sales can lead to a large increase in operating income.

[28] operating margin — Operating income divided by revenue, expressed as a percentage, indicating how much profit a company makes from its core operations before interest and taxes.

[29] oversupply — A condition where the quantity of goods available exceeds demand, leading to falling prices and inventory buildup, common in memory cycles.

[30] peak-cycle multiples — Valuation ratios (e.g., P/E) at the high point of an economic or industry cycle, often considered unsustainable when applied to cyclical stocks.

[31] price-to-earnings (P/E) ratio — Price-to-Earnings ratio — A valuation metric calculated by dividing a company's stock price by its earnings per share, used to assess whether a stock is overvalued or undervalued relative to earnings.

[32] pricing power — The ability of a company to raise prices without losing customers, often derived from brand loyalty, market concentration, or product differentiation.

[33] R&D intensity — Research and Development intensity — The ratio of research and development spending to revenue, indicating a company's commitment to innovation and technological advancement.

[34] share repurchase authorization — A board-approved plan allowing a company to buy back its own shares from the market, often signaling confidence in future earnings and returning cash to shareholders.

[35] spot market — A public financial market where commodities or securities are traded for immediate delivery and payment, with prices fluctuating based on current supply and demand.

[36] total cost of ownership (TCO) — Total Cost of Ownership — The complete lifecycle cost of a product or system, including purchase price, maintenance, energy consumption, and disposal, often used to compare alternatives.

[37] trough-cycle valuations — Valuation multiples (e.g., P/E) observed at the low point of a business cycle, often reflecting depressed earnings and investor pessimism.

[38] upcycle — A phase in a cyclical industry characterized by rising demand, prices, and profitability, following a downturn or trough.

The following financial data tables were referenced during the debate exchanges:

| Metric | 2023 | 2024 | 2025E | Growth Rate |

|---|---|---|---|---|

| Data Center Revenue | $2.1B | $3.8B | $6.5B | +210% |

| HBM Revenue | $0.3B | $1.2B | $3.0B | +900% |

| AI Server Content | 1x | 3x | 8x | +700% |

Legend: Micron Technology data center and HBM revenue trajectory (FY2023–FY2025E). Revenue in USD billions; AI server content relative to traditional servers. Source: Company earnings reports and industry analysis.

</FinancialData>

| Quarter | Gross Margin | Operating Margin | EPS |

|---|---|---|---|

| Q1 FY2024 | 18.2% | -8.5% | -$1.91 |

| Q2 FY2024 | 24.5% | 2.1% | -$0.95 |

| Q3 FY2024 | 31.8% | 12.4% | $0.62 |

| Q4 FY2024 | 36.2% | 18.7% | $1.18 |

| Q1 FY2025 | 38.4% | 22.3% | $1.89 |

Legend: Micron Technology quarterly margin and earnings progression (FY2024–FY2025). Margins in percentage; EPS in USD. Source: Company quarterly earnings reports.

</FinancialData>

| Company | DRAM Market Share | NAND Market Share | R&D Intensity |

|---|---|---|---|

| Samsung | 42% | 33% | 8.2% |

| SK Hynix | 29% | 18% | 7.5% |

| Micron | 23% | 12% | 9.1% |

Legend: Global memory manufacturer market positioning (2024). Market share in percentage of global production; R&D intensity as percentage of revenue. Source: Industry market research and company filings.

</FinancialData>

| Cycle Period | Peak-to-Trough Decline | Recovery Duration | Primary Driver |

|---|---|---|---|

| 2018-2020 | -52% | 18 months | PC/Smartphone |

| 2022-2023 | -48% | 12 months | Inventory Correction |

| 2024-2026E | -28% (est.) | 24+ months (est.) | AI Infrastructure |

Legend: Memory market cycle comparison showing reduced volatility in current AI-driven cycle. Decline percentages represent industry revenue contraction; recovery duration in months. Source: Industry cycle analysis and company guidance.

</FinancialData>

| Price Target | Call Option Value | Implied Return |

|---|---|---|

| $98 | $16.91 | Baseline |

| $105 | $19.23 | +13.7% |

| $115 | $23.81 | +40.8% |

| $125 | $29.16 | +72.4% |

| $135 | $35.89 | +112.2% |

Legend: Projected call option value appreciation along price path for MU $100 strike calls with 90 days to expiry. Values in USD; returns relative to baseline. Source: Options pricing model analysis.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 35 | 2026-05-29 | 855.75 | 868.4 | 876.52 | 999.5% | 14 | 8 |

| PUT | 35 | 2026-05-29 | - | 0.01 | 0.01 | 999.5% | 123 | 168 |

| CALL | 40 | 2026-05-29 | 850.95 | 863.4 | 668.18 | 999.5% | - | 2 |

| PUT | 40 | 2026-05-29 | - | 0.01 | - | 986.8% | - | 29 |

| CALL | 45 | 2026-05-29 | 845.6 | 858.4 | 816.91 | 999.5% | 2 | - |

| PUT | 45 | 2026-05-29 | - | 0.01 | - | 947.8% | - | 4 |

| CALL | 50 | 2026-05-29 | 840.6 | 853.4 | 721.15 | 999.5% | - | 2 |

| PUT | 50 | 2026-05-29 | - | 0.01 | - | 912.7% | - | 4014 |

| CALL | 55 | 2026-05-29 | 835.9 | 848.4 | - | 999.5% | - | - |

| PUT | 55 | 2026-05-29 | - | 0.01 | - | 881.5% | - | 752 |

| CALL | 60 | 2026-05-29 | 831.2 | 843.45 | - | 999.5% | - | - |

| PUT | 60 | 2026-05-29 | - | 0.01 | - | 853.2% | - | 5 |

| CALL | 65 | 2026-05-29 | 825.8 | 838.4 | 583.85 | 999.5% | - | 1 |

| PUT | 65 | 2026-05-29 | - | 0.01 | - | 826.8% | - | 10 |

| CALL | 70 | 2026-05-29 | 820.6 | 833.4 | 716.3 | 999.5% | - | 1 |

| PUT | 70 | 2026-05-29 | - | 0.01 | - | 803.4% | - | 16 |

| CALL | 75 | 2026-05-29 | 815.6 | 828.4 | 649.26 | 999.5% | - | 1 |

| PUT | 75 | 2026-05-29 | - | 0.01 | - | 781.0% | - | 10 |

| CALL | 80 | 2026-05-29 | 810.6 | 823.4 | 728.3 | 999.5% | - | 1 |

| PUT | 80 | 2026-05-29 | - | 0.01 | - | 760.5% | - | 28 |

| CALL | 85 | 2026-05-29 | 806.4 | 818.4 | 821.79 | 999.5% | 1 | 3 |

| PUT | 85 | 2026-05-29 | - | 0.01 | - | 741.0% | - | 16 |

| CALL | 90 | 2026-05-29 | 800.9 | 813.4 | 664.14 | 999.5% | - | 2 |

| PUT | 90 | 2026-05-29 | - | 0.01 | - | 722.4% | - | 19 |

| CALL | 95 | 2026-05-29 | 795.6 | 808.4 | 661.99 | 999.5% | - | 2 |

| PUT | 95 | 2026-05-29 | - | 0.01 | 0.13 | 704.9% | 1 | 6 |

| CALL | 100 | 2026-05-29 | 791.85 | 803.4 | 478.65 | 999.5% | - | 1 |

| PUT | 100 | 2026-05-29 | - | 0.01 | - | 689.3% | - | 11 |

| CALL | 105 | 2026-05-29 | 786.45 | 798.4 | 701.45 | 999.5% | - | 2 |

| PUT | 105 | 2026-05-29 | - | 0.01 | 0.1 | 673.7% | 2 | 6 |

| CALL | 110 | 2026-05-29 | 781.25 | 793.4 | - | 999.5% | - | - |

| PUT | 110 | 2026-05-29 | - | 0.01 | 0.01 | 659.0% | 5 | 11 |

| CALL | 115 | 2026-05-29 | 776.65 | 788.4 | 536.65 | 999.5% | - | 15 |

| PUT | 115 | 2026-05-29 | - | 0.01 | 0.01 | 644.4% | 4 | 7 |

| CALL | 120 | 2026-05-29 | 770.6 | 783.4 | 587.45 | 978.0% | - | 2 |

| PUT | 120 | 2026-05-29 | - | 0.01 | 0.01 | 630.7% | 7 | 8 |

| CALL | 125 | 2026-05-29 | 765.65 | 778.45 | - | 964.4% | - | - |

| PUT | 125 | 2026-05-29 | - | 0.01 | 0.01 | 618.1% | 4 | 24 |

| CALL | 130 | 2026-05-29 | 761.1 | 773.4 | - | 965.4% | - | - |

| PUT | 130 | 2026-05-29 | - | 0.01 | 0.01 | 606.4% | 5 | 86 |

| CALL | 135 | 2026-05-29 | 756.7 | 768.4 | 726.09 | 974.1% | 3 | - |

| PUT | 135 | 2026-05-29 | - | 0.01 | 0.01 | 593.7% | 7 | 145 |

| CALL | 140 | 2026-05-29 | 750.6 | 763.45 | 625.05 | 904.9% | - | 1 |

| PUT | 140 | 2026-05-29 | - | 0.01 | 0.01 | 582.9% | 9 | 151 |

| CALL | 145 | 2026-05-29 | 745.9 | 758.4 | 615.76 | 900.0% | - | 1 |

| PUT | 145 | 2026-05-29 | - | 0.01 | 0.01 | 571.2% | 16 | 8 |

| CALL | 150 | 2026-05-29 | 740.6 | 753.4 | 625.2 | 867.8% | - | 1 |

| PUT | 150 | 2026-05-29 | - | 0.01 | - | 561.5% | - | 329 |

| CALL | 155 | 2026-05-29 | 736.1 | 748.4 | 532.45 | 876.6% | - | 2 |

| PUT | 155 | 2026-05-29 | - | 0.01 | 0.01 | 550.7% | 9 | 770 |

| CALL | 160 | 2026-05-29 | 730.95 | 743.45 | 622.3 | 856.1% | - | 1 |

| PUT | 160 | 2026-05-29 | - | 0.01 | 0.01 | 541.0% | 10 | 40 |

| CALL | 165 | 2026-05-29 | 725.9 | 738.4 | - | 835.6% | - | - |

| PUT | 165 | 2026-05-29 | - | 0.01 | 0.01 | 531.2% | 6 | 255 |

| CALL | 170 | 2026-05-29 | 720.6 | 733.4 | 632.85 | 806.3% | - | 1 |

| PUT | 170 | 2026-05-29 | - | 0.01 | 0.01 | 522.5% | 21 | 112 |

| CALL | 175 | 2026-05-29 | 716.25 | 728.45 | 534.27 | 823.9% | - | 1 |

| PUT | 175 | 2026-05-29 | - | 0.01 | 0.01 | 512.7% | 17 | 4 |

| CALL | 180 | 2026-05-29 | 711.15 | 723.4 | 606.6 | 803.4% | - | 2 |

| PUT | 180 | 2026-05-29 | - | 0.01 | 0.02 | 503.9% | 4 | 366 |

| CALL | 185 | 2026-05-29 | 705.6 | 718.4 | 340.3 | 765.4% | - | 2 |

| PUT | 185 | 2026-05-29 | - | 0.01 | 0.01 | 496.1% | 7 | 45 |

| CALL | 190 | 2026-05-29 | 701.1 | 713.4 | 520.07 | 774.2% | - | 1 |

| PUT | 190 | 2026-05-29 | - | 0.01 | 0.01 | 487.3% | 5 | 4 |

| CALL | 195 | 2026-05-29 | 696.35 | 708.4 | 516.0 | 772.2% | - | 3 |

| PUT | 195 | 2026-05-29 | - | 0.01 | 0.02 | 479.5% | 6 | - |

| CALL | 200 | 2026-05-29 | 691.25 | 703.5 | 656.9 | 759.5% | 1 | 10 |

| PUT | 200 | 2026-05-29 | - | 0.01 | 0.03 | 471.7% | 2 | 996 |

| CALL | 205 | 2026-05-29 | 686.05 | 698.45 | 508.59 | 737.1% | - | 4 |

| PUT | 205 | 2026-05-29 | - | 0.01 | 0.3 | 463.9% | 4 | 19 |

| CALL | 210 | 2026-05-29 | 681.15 | 693.5 | 321.46 | 731.2% | - | 1 |

| PUT | 210 | 2026-05-29 | - | 0.01 | 0.01 | 456.1% | 4 | 14 |

| CALL | 215 | 2026-05-29 | 676.5 | 688.45 | 509.35 | 730.2% | - | 9 |

| PUT | 215 | 2026-05-29 | - | 0.01 | - | 449.3% | - | 197 |

| CALL | 220 | 2026-05-29 | 670.65 | 683.45 | 570.6 | 686.3% | - | 2 |

| PUT | 220 | 2026-05-29 | - | 0.01 | 0.01 | 442.5% | 4 | 44 |

| CALL | 225 | 2026-05-29 | 665.95 | 678.45 | 546.6 | 687.3% | - | 2 |

| PUT | 225 | 2026-05-29 | - | 0.01 | 0.01 | 434.6% | 1 | 6 |

| CALL | 230 | 2026-05-29 | 661.4 | 673.45 | 495.12 | 692.2% | - | 2 |

| PUT | 230 | 2026-05-29 | - | 0.01 | 0.1 | 427.8% | 1 | 213 |

| CALL | 235 | 2026-05-29 | 656.6 | 668.5 | 263.45 | 690.3% | - | 2 |

| PUT | 235 | 2026-05-29 | - | 0.01 | 0.12 | 422.0% | 1 | 270 |

| CALL | 240 | 2026-05-29 | 650.65 | 663.45 | 475.13 | 645.4% | - | 5 |

| PUT | 240 | 2026-05-29 | - | 0.01 | 0.1 | 415.1% | 1 | 135 |

| CALL | 245 | 2026-05-29 | 645.65 | 658.5 | 551.25 | 637.6% | - | 1 |

| PUT | 245 | 2026-05-29 | - | 0.01 | 0.12 | 408.3% | 2 | 13 |

| CALL | 250 | 2026-05-29 | 640.9 | 653.45 | 510.29 | 634.6% | - | 4 |

| PUT | 250 | 2026-05-29 | - | 0.01 | - | 402.5% | - | 553 |

| CALL | 255 | 2026-05-29 | 636.0 | 648.5 | 459.02 | 630.7% | - | 1 |

| PUT | 255 | 2026-05-29 | - | 0.01 | 0.25 | 396.6% | 3 | 12 |

| CALL | 260 | 2026-05-29 | 630.65 | 643.5 | 515.7 | 609.3% | - | 2 |

| PUT | 260 | 2026-05-29 | - | 0.01 | 0.01 | 390.7% | 3 | 737 |

| CALL | 265 | 2026-05-29 | 626.15 | 638.5 | 532.2 | 617.1% | - | 3 |

| PUT | 265 | 2026-05-29 | - | 0.01 | 0.02 | 384.9% | 6 | 318 |

| CALL | 270 | 2026-05-29 | 621.9 | 633.45 | 517.85 | 627.8% | - | 2 |

| PUT | 270 | 2026-05-29 | - | 0.01 | 0.01 | 379.0% | 2 | 363 |

| CALL | 275 | 2026-05-29 | 616.0 | 628.45 | 575.17 | 592.7% | 3 | 4 |

| PUT | 275 | 2026-05-29 | - | 0.01 | 0.25 | 373.2% | 2 | 254 |

| CALL | 280 | 2026-05-29 | 611.3 | 623.45 | 492.26 | 592.7% | - | 3 |

| PUT | 280 | 2026-05-29 | - | 0.05 | 0.02 | 367.3% | 5 | 4466 |

| CALL | 285 | 2026-05-29 | 605.7 | 618.45 | 409.0 | 565.4% | - | 4 |

| PUT | 285 | 2026-05-29 | - | 0.01 | 0.01 | 362.5% | 6 | 437 |

| CALL | 290 | 2026-05-29 | 600.65 | 613.5 | 585.22 | 557.6% | 1 | 2 |

| PUT | 290 | 2026-05-29 | - | 0.23 | 0.01 | 356.6% | 4 | 96 |

| CALL | 295 | 2026-05-29 | 596.1 | 608.5 | 507.67 | 562.5% | - | 9 |

| PUT | 295 | 2026-05-29 | - | 0.02 | 0.01 | 351.7% | 6 | 262 |

| CALL | 300 | 2026-05-29 | 591.85 | 603.5 | 427.04 | 575.1% | - | 16 |

| PUT | 300 | 2026-05-29 | - | 0.01 | 0.01 | 346.8% | 63 | 3629 |

| CALL | 305 | 2026-05-29 | 586.0 | 598.5 | 465.85 | 543.9% | - | 3 |

| PUT | 305 | 2026-05-29 | - | 0.01 | 0.01 | 341.0% | 11 | 15 |

| CALL | 310 | 2026-05-29 | 581.05 | 593.5 | 567.0 | 537.1% | 3 | 15 |

| PUT | 310 | 2026-05-29 | - | 0.01 | 0.01 | 336.1% | 26 | 506 |

| CALL | 315 | 2026-05-29 | 576.0 | 588.5 | 582.33 | 528.3% | 31 | 33 |

| PUT | 315 | 2026-05-29 | - | 0.37 | 0.01 | 331.2% | 9 | 46 |

| CALL | 320 | 2026-05-29 | 570.7 | 583.55 | 433.48 | 512.7% | - | 6 |

| PUT | 320 | 2026-05-29 | - | 0.02 | 0.01 | 326.4% | 154 | 113 |

| CALL | 325 | 2026-05-29 | 566.0 | 578.5 | 481.95 | 513.7% | - | 3 |

| PUT | 325 | 2026-05-29 | - | 0.04 | 0.01 | 321.5% | 8 | 1137 |

| CALL | 330 | 2026-05-29 | 561.4 | 573.5 |

…(truncated)…

MCP tool: price_option_path

{"option_path": [16.91480203213232, 19.23202812493586, 23.80935375252443, 29.162283365222834, 35.88587506802621], "volatility_used": 0.8948914156918083, "symbol": "MU"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.