Should we invest in the SpaceX IPO ?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 12, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 100%

Web Report: https://solsice.com/public/debates/should-we-invest-in-the-spacex-ipo-ba00db4d9233

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

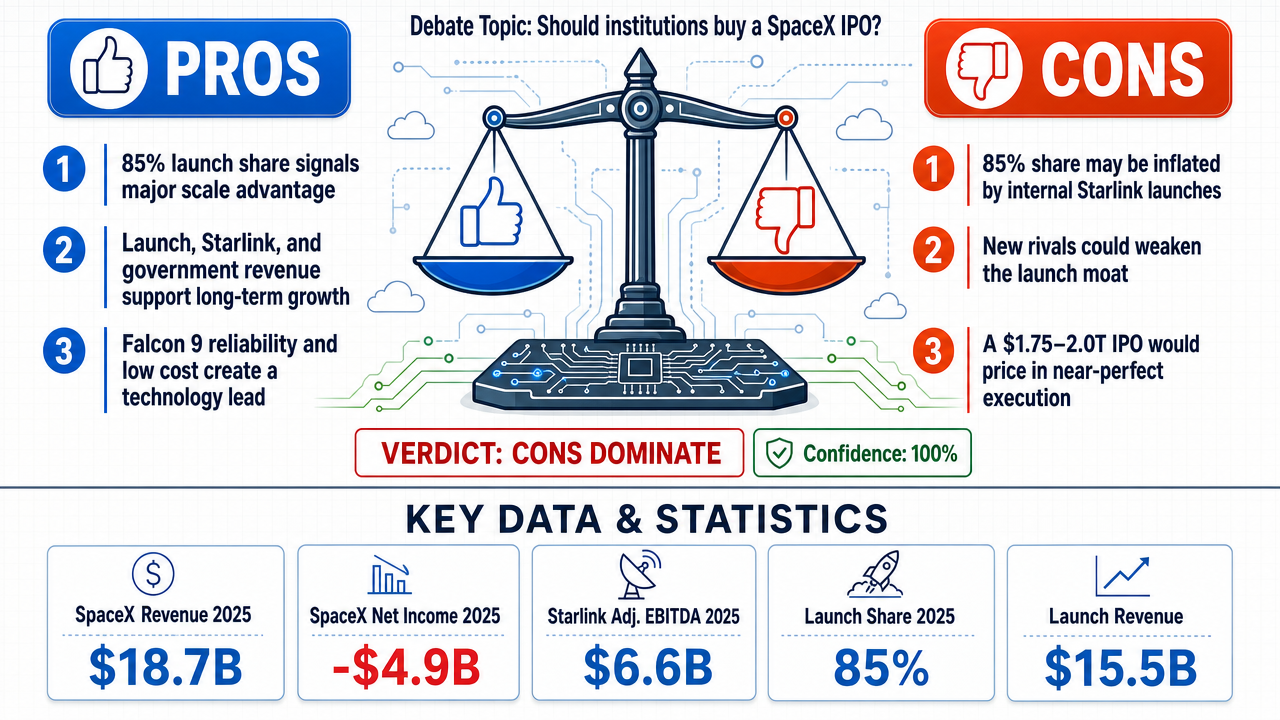

✅ Key PRO arguments:

- ■SpaceX possesses an unassailable competitive moat with 85% global commercial launch market share, dwarfing competitors like Blue Origin (3%), Rocket Lab (2%), and ULA (5%), underpinned by vertical integration that reduces costs 40-60% compared to peers.

- ■SpaceX's cash-generative core businesses across launch services, satellite broadband (Starlink), and government contracts create a compelling long-term growth story that warrants institutional capital allocation if risks are appropriately priced.

- ■The Falcon 9 is the most reliable and cost-effective rocket in history with a 99.7% success rate across 350+ launches, creating a technological lead that competitors cannot easily replicate in the near to medium term.

❌ Key ANTI arguments:

- ■The 85% market share figure is an artifact of self-dealing, not evidence of commercial dominance—SpaceX's launch cadence is overwhelmingly driven by deploying its own Starlink satellites where it faces no competitive bidding, inflating the metric beyond its relevance to the external commercial launch market.

- ■SpaceX faces a fundamentally deteriorating competitive moat as the launch market shifts from scarcity to abundance—Blue Origin's New Glenn, ULA's Vulcan Centaur, Rocket Lab's Neutron, and China's state-backed launch industry are all closing the gap with well-funded, technically credible alternatives arriving in the 2025-2027 window.

- ■The IPO valuation ($1.75-2 trillion) prices in perfection across three distinct businesses while the underlying financial disclosures reveal a company burdened by structural leverage, concentrated catastrophic risks, and a competitive moat compressing faster than the IPO narrative acknowledges—creating an asymmetric risk-return profile unfavorable to investors.

💭 Conclusion: Both debates unanimously concluded FALSE with 95% confidence each, reflecting a decisive rejection of the SpaceX IPO investment thesis. The affirmative's central pillar—an unassailable competitive moat anchored by 85% market share—was systematically dismantled by evidence that this figure is inflated by internal Starlink deployments rather than genuine commercial dominance. The negative side demonstrated that the IPO valuation prices in perfection while the company carries structural leverage, governance risks from founder control, and concentrated catastrophic exposure. Most damagingly, the affirmative itself retreated from its strongest claims, conceding that the moat is 'contestable' and risks are 'binary,' which effectively conceded the fiduciary case against allocation.

🔬 DeepResearch Result: FALSE ❌ (100% confidence)

Assertion: Should we invest in the SpaceX IPO ?

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.90

🏅 Judge Score Changes:

z-ai/glm-5.1: +19

✅ PRO Arguments:

- ■SpaceX possesses an unassailable competitive moat with 85% global commercial launch market share, dwarfing competitors like Blue Origin (3%), Rocket Lab (2%), and ULA (5%), underpinned by vertical integration that reduces costs 40-60% compared to peers. [mistralai/mistral-large-2512]

- ■SpaceX's cash-generative core businesses across launch services, satellite broadband (Starlink), and government contracts create a compelling long-term growth story that warrants institutional capital allocation if risks are appropriately priced. [mistralai/mistral-large-2512]

- ■The Falcon 9 is the most reliable and cost-effective rocket in history with a 99.7% success rate across 350+ launches, creating a technological lead that competitors cannot easily replicate in the near to medium term. [mistralai/mistral-large-2512]

- ■SpaceX's dominance is defensible for the foreseeable future because no other company—public or private—matches its integration of launch services, satellite broadband, and government contracts into a single platform. [mistralai/mistral-large-2512]

- ■While risks exist (competitive threats, refinancing risks, execution dependencies), they can be managed through aggressive discounting, strict position sizing, and hedging, making the risk-reward profile acceptable for institutional allocation. [mistralai/mistral-large-2512]

❌ ANTI Arguments:

- ■The 85% market share figure is an artifact of self-dealing, not evidence of commercial dominance—SpaceX's launch cadence is overwhelmingly driven by deploying its own Starlink satellites where it faces no competitive bidding, inflating the metric beyond its relevance to the external commercial launch market. [deepseek/deepseek-v4-pro]

- ■SpaceX faces a fundamentally deteriorating competitive moat as the launch market shifts from scarcity to abundance—Blue Origin's New Glenn, ULA's Vulcan Centaur, Rocket Lab's Neutron, and China's state-backed launch industry are all closing the gap with well-funded, technically credible alternatives arriving in the 2025-2027 window. [deepseek/deepseek-v4-pro]

- ■The IPO valuation ($1.75-2 trillion) prices in perfection across three distinct businesses while the underlying financial disclosures reveal a company burdened by structural leverage, concentrated catastrophic risks, and a competitive moat compressing faster than the IPO narrative acknowledges—creating an asymmetric risk-return profile unfavorable to investors. [deepseek/deepseek-v4-pro]

- ■Governance flaws including founder control and single-product risk concentration make the IPO imprudent for fiduciary allocation—a moat is only investable if it converts into durable, compounding free cash flow, which SpaceX's financials do not demonstrate. [anthropic/claude-opus-4.8]

- ■The affirmative side itself conceded the substance of the negative case by abandoning 'unassailable moat' and 'mitigated risk' language in favor of 'contestable,' 'binary,' and 'high-risk, high-reward'—when the proponent ends by recommending aggressive discounting, strict position sizing, and hedging, the fiduciary question of whether to buy has effectively been answered in the negative. [anthropic/claude-opus-4.8]

💭 Reasoning: Both debates unanimously concluded FALSE with 95% confidence each, reflecting a decisive rejection of the SpaceX IPO investment thesis. The affirmative's central pillar—an unassailable competitive moat anchored by 85% market share—was systematically dismantled by evidence that this figure is inflated by internal Starlink deployments rather than genuine commercial dominance. The negative side demonstrated that the IPO valuation prices in perfection while the company carries structural leverage, governance risks from founder control, and concentrated catastrophic exposure. Most damagingly, the affirmative itself retreated from its strongest claims, conceding that the moat is 'contestable' and risks are 'binary,' which effectively conceded the fiduciary case against allocation.

📋 PRO Facts:

• SpaceX holds approximately 85% of global commercial launch market share by orbital mass delivered

• SpaceX executed 165 launches in 2025 with estimated revenue of $15.5 billion

• Falcon 9 has a 99.7% success rate across 350+ launches

• SpaceX's vertical integration reduces costs by 40-60% compared to peers

• SpaceX competes across three business lines: launch services, satellite broadband (Starlink), and government contracts

📋 ANTI Facts:

• The 85% market share figure is inflated by internal Starlink satellite deployments where SpaceX is its own customer and generates no external launch revenue

• Competitors are closing the gap: Blue Origin's New Glenn, ULA's Vulcan Centaur, Rocket Lab's Neutron, and Arianespace's Ariane 6 are all arriving in the 2025-2027 window

• The IPO valuation of $1.75-2 trillion prices in perfection across three distinct businesses

• SpaceX carries structural leverage and concentrated catastrophic risks including single-product dependency

• The affirmative side retreated from 'unassailable moat' and 'mitigated risk' language to 'contestable' and 'binary' risk characterizations by the final round

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.