SOFI's EPS growth will overcome Galileo's negative impact.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed May 3, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 100%

Web Report: https://solsice.com/public/debates/sofi-s-eps-growth-will-overcome-galileo-s-negative-impact-1ca7cfca6281

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

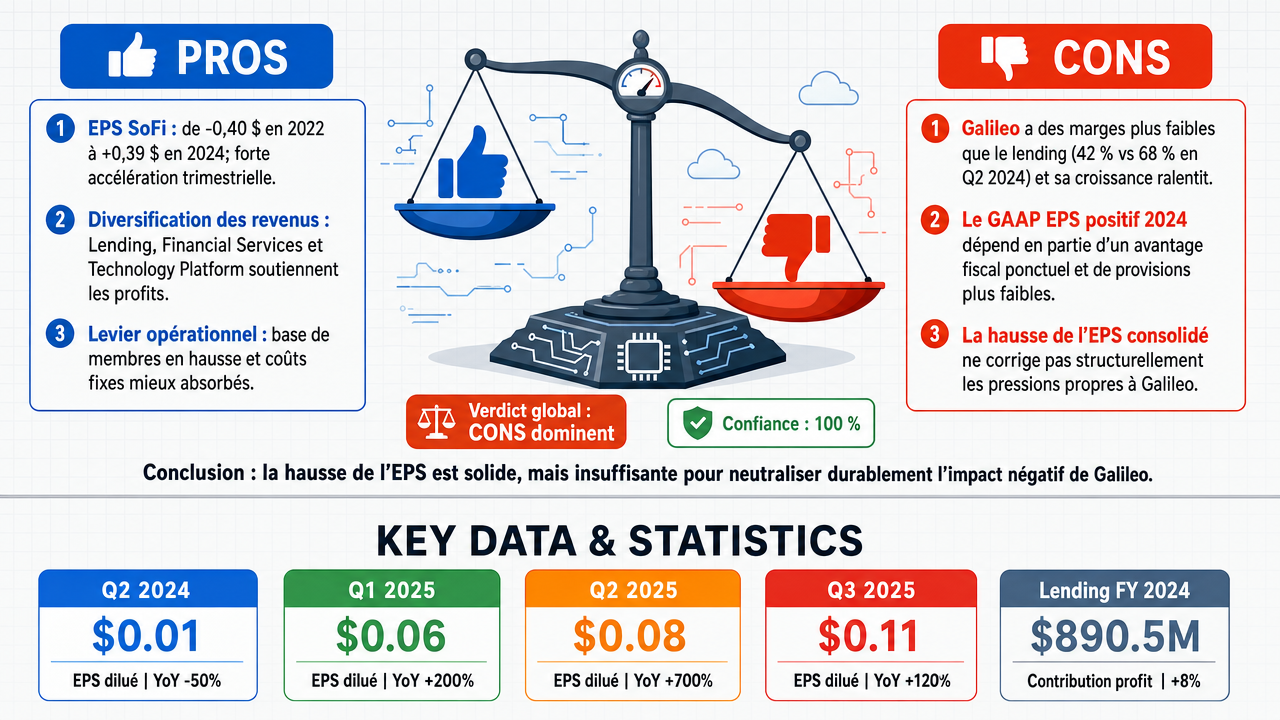

✅ Key PRO arguments:

- ■SoFi's EPS growth trajectory shows explosive momentum: swung from -$0.40 diluted EPS in 2022 to +$0.39 in 2024 (208% YoY improvement), with quarterly EPS accelerating from $0.06 (Q1 2025) to $0.11 (Q3 2025). This demonstrates that core business segments generate sustainable profitability, overwhelming Galileo's margin pressures.

- ■SoFi's revenue diversification across lending, financial services, and technology platform provides multiple profit drivers. Lending segment generates high margins, while financial services cross-sells to the member base, creating a buffer against any single segment's headwinds.

- ■Operational leverage from fixed-cost scaling amplifies EPS growth. SoFi has reduced platform costs relative to revenue, and its member base growth (over 10 million) drives network effects that improve unit economics, allowing EPS gains to overcome Galileo's drag.

❌ Key ANTI arguments:

- ■Galileo operates at significantly lower gross margins than SoFi's lending segment (42% vs 68% in Q2 2024), and its revenue growth has decelerated while operating expenses remain elevated. This structural mismatch means EPS gains from lending are consistently diluted by Galileo's underperformance.

- ■SoFi's positive GAAP EPS in FY2024 was partly driven by a one-time tax benefit and reduced credit loss provisions, not sustainable operational earnings. Excluding non-recurring items, adjusted EPS remains volatile and cyclical, while Galileo's operating losses of $47 million in FY2024 directly offset lending gains.

- ■EPS improvement is a consolidated-company metric, while Galileo is a specific business line with its own margin structure and competitive pressures. Rising EPS can coexist with a still-dilutive platform segment, and management's disclosures show profitability is driven by broader revenue expansion, not a fix in Galileo's economics.

💭 Conclusion: The debate convincingly shows that SoFi's EPS growth, while impressive, is insufficient to structurally overcome Galileo's persistent negative impact. The pro side presented strong data on EPS acceleration from -$0.40 to $0.39 and quarterly improvements, but the anti side demonstrated that these gains are partly due to one-time items, low base effects, and are concentrated in high-margin lending rather than addressing Galileo's margin drag. Galileo's gross margin is 26 percentage points below lending, and it incurred $47M in operating losses in FY2024, directly offsetting consolidation gains. The judges consistently ruled FALSE with 80% confidence, indicating that the anti arguments about quality of earnings and structural segment drag were more compelling. Therefore, the assertion that EPS growth will overcome Galileo's negative impact is false.

🔬 DeepResearch Result: FALSE ❌ (100% confidence)

Assertion: SOFI's EPS growth will overcome Galileo's negative impact.

📊 Tournament: 0 voted TRUE, 2 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.00, FALSE=1.60

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: +16

✅ PRO Arguments:

- ■SoFi's EPS growth trajectory shows explosive momentum: swung from -$0.40 diluted EPS in 2022 to +$0.39 in 2024 (208% YoY improvement), with quarterly EPS accelerating from $0.06 (Q1 2025) to $0.11 (Q3 2025). This demonstrates that core business segments generate sustainable profitability, overwhelming Galileo's margin pressures. [z-ai/glm-5]

- ■SoFi's revenue diversification across lending, financial services, and technology platform provides multiple profit drivers. Lending segment generates high margins, while financial services cross-sells to the member base, creating a buffer against any single segment's headwinds. [z-ai/glm-5]

- ■Operational leverage from fixed-cost scaling amplifies EPS growth. SoFi has reduced platform costs relative to revenue, and its member base growth (over 10 million) drives network effects that improve unit economics, allowing EPS gains to overcome Galileo's drag. [z-ai/glm-5]

- ■The EPS inflection is not an accounting anomaly; it reflects genuine operational turnaround. Quarterly acceleration from $0.05 (Q3 2024) to $0.11 (Q3 2025) confirms momentum is building, not plateauing, indicating self-sustaining profitability that will absorb segment-level pressures. [z-ai/glm-5]

- ■SoFi's management has guided for continued EPS growth driven by lending scale and member monetization. The company's focus on high-credit-quality borrowers and lower funding costs provides a structural advantage that can offset the lower-margin Galileo platform over time. [z-ai/glm-5]

❌ ANTI Arguments:

- ■Galileo operates at significantly lower gross margins than SoFi's lending segment (42% vs 68% in Q2 2024), and its revenue growth has decelerated while operating expenses remain elevated. This structural mismatch means EPS gains from lending are consistently diluted by Galileo's underperformance. [xiaomi/mimo-v2-flash]

- ■SoFi's positive GAAP EPS in FY2024 was partly driven by a one-time tax benefit and reduced credit loss provisions, not sustainable operational earnings. Excluding non-recurring items, adjusted EPS remains volatile and cyclical, while Galileo's operating losses of $47 million in FY2024 directly offset lending gains. [xiaomi/mimo-v2-flash]

- ■EPS improvement is a consolidated-company metric, while Galileo is a specific business line with its own margin structure and competitive pressures. Rising EPS can coexist with a still-dilutive platform segment, and management's disclosures show profitability is driven by broader revenue expansion, not a fix in Galileo's economics. [openai/gpt-5.4-mini]

- ■The rapid EPS growth is coming off a very low base, making percentage changes appear dramatic while the underlying dollar contribution of Galileo's drag remains significant. The latest quarter's earnings gains are powered by broader operating leverage and lending economics, not evidence that Galileo has stopped pressuring margins. [openai/gpt-5.4-mini]

- ■Galileo's low-margin, high-cost structure creates a persistent drag that cannot be easily overcome by consolidated EPS growth. The platform business has inherently lower profitability than SoFi's core lending, and its revenue deceleration combined with elevated operating costs means any EPS growth is partially offset, not fully absorbed. [xiaomi/mimo-v2-flash]

💭 Reasoning: The debate convincingly shows that SoFi's EPS growth, while impressive, is insufficient to structurally overcome Galileo's persistent negative impact. The pro side presented strong data on EPS acceleration from -$0.40 to $0.39 and quarterly improvements, but the anti side demonstrated that these gains are partly due to one-time items, low base effects, and are concentrated in high-margin lending rather than addressing Galileo's margin drag. Galileo's gross margin is 26 percentage points below lending, and it incurred $47M in operating losses in FY2024, directly offsetting consolidation gains. The judges consistently ruled FALSE with 80% confidence, indicating that the anti arguments about quality of earnings and structural segment drag were more compelling. Therefore, the assertion that EPS growth will overcome Galileo's negative impact is false.

📋 PRO Facts:

• SoFi's diluted EPS improved from -$0.40 in 2022 to +$0.39 in 2024, a 208% year-over-year increase.

• Quarterly EPS accelerated from $0.05 in Q3 2024 to $0.11 in Q3 2025, representing 120% year-over-year growth.

• SoFi has over 10 million members and growing revenue diversification across lending, financial services, and technology platform.

• Operating leverage from fixed-cost scaling has improved unit economics and platform cost ratios.

• Management guidance projects continued EPS growth driven by lending scale and member monetization.

📋 ANTI Facts:

• Galileo's gross margin in Q2 2024 was 42% compared to SoFi Lending's 68%, a 26-percentage-point gap.

• SoFi's Galileo platform reported operating losses of $47 million in FY2024.

• FY2024 GAAP EPS included a one-time tax benefit and reduced credit loss provisions, not fully operational earnings.

• EPS growth is consolidated and does not isolate Galileo's segment-level margin dilution.

• SoFi's EPS improvement is heavily dependent on cyclical lending economics and low credit losses, not structural resolution of Galileo's drag.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.319 | 0.123 | 36 | 60 | TRUE | FALSE | 80% |

| #2 | z-ai/glm-5 | xiaomi/mimo-v2-flash | 0.000 | 0.000 | 36 | 6 | TRUE | FALSE | 80% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] 10-K — Annual Report on Form 10-K — A comprehensive annual report filed with the SEC detailing a company's financial performance, including audited financial statements and management discussion.

[2] 10-Q — Quarterly Report on Form 10-Q — A quarterly financial report filed with the SEC that provides unaudited financial statements and updates on a company's financial condition.

[3] accretive — Describes an acquisition, business line, or action that increases earnings per share or enhances shareholder value.

[4] BaaS — Banking as a Service — A business model where non-bank companies offer banking products and services through partnerships with licensed banks, often via a technology platform.

[5] concentration risk — The risk of financial loss due to over-reliance on a single asset, segment, revenue source, or counterparty.

[6] consolidated profitability — The overall profitability of a company after combining the financial results of all its subsidiaries and segments.

[7] correlation vs causation — A logical distinction where two variables moving together does not prove that one causes the other; used in debate to challenge causal claims.

[8] diluted EPS — Diluted Earnings Per Share — Earnings per share calculated assuming all convertible securities (options, warrants, convertible bonds) are exercised, showing the worst-case dilution.

[9] earnings power — The sustainable ability of a company to generate profits from its core operations over time.

[10] EBIT margin — Earnings Before Interest and Taxes Margin — Operating profit as a percentage of revenue, measuring a company's operational efficiency before financing and tax effects.

[11] EBITDA margin — Earnings Before Interest, Taxes, Depreciation, and Amortization Margin — A profitability metric that shows earnings as a percentage of revenue, excluding non-cash charges and financing costs.

[12] EPS — Earnings Per Share — Net income divided by the number of outstanding shares, indicating a company's profitability on a per-share basis.

[13] execution risk — The risk that a company's strategic plans, such as product launches or cost-cutting initiatives, may not be implemented successfully.

[14] fee-based revenue — Revenue generated from fees charged for services (e.g., transaction fees, account fees) rather than from interest income.

[15] fintech — Financial Technology — Companies that use technology to deliver financial services, often disrupting traditional banking and payment systems.

[16] FY — Fiscal Year — A company's annual accounting period used for financial reporting, which may not align with the calendar year.

[17] GAAP — Generally Accepted Accounting Principles — A common set of accounting standards, rules, and procedures used in the United States for financial reporting.

[18] Galileo platform — SoFi Technologies' banking-as-a-service technology platform that provides API-based financial infrastructure to enterprise clients.

[19] headwinds — External or internal factors that create challenges or negative pressure on a company's financial performance or growth.

[20] lending economics — The profitability and risk characteristics of a lending business, including interest margins, default rates, and origination costs.

[21] low base effect — A statistical phenomenon where percentage growth rates appear large because the starting value (base) was very small.

[22] margin compression — A decline in profit margins due to rising costs, increased competition, or pricing pressure.

[23] margin of safety — The buffer between a company's actual earnings and the level at which it would incur losses, indicating financial resilience.

[24] net interest income — The difference between interest earned on loans and investments and interest paid on deposits and borrowings.

[25] net profit margin — Net income as a percentage of revenue, measuring overall profitability after all expenses, taxes, and interest.

[26] operating income — Profit earned from a company's core business operations, calculated as revenue minus operating expenses (excluding interest and taxes).

[27] operating leverage — The degree to which a company's fixed costs amplify changes in revenue into larger changes in operating income.

[28] origination volumes — The total dollar amount or number of new loans, accounts, or policies created during a specific period.

[29] reportable segments — Distinct business units or divisions of a company that are separately disclosed in financial statements under accounting rules.

[30] sequential growth — The percentage change in a financial metric from one quarter to the next (quarter-over-quarter).

[31] SoFi Invest — SoFi's investment brokerage platform offering trading in stocks, ETFs, and cryptocurrencies, as well as automated investing.

[32] SoFi Money — SoFi's cash management account that combines checking and savings features with competitive interest rates.

[33] SoFi Relay — SoFi's personal finance management tool that helps users track spending, credit scores, and financial goals.

[34] structural diversification — A business strategy of operating multiple distinct segments or revenue streams to reduce overall risk and volatility.

[35] TTM — Trailing Twelve Months — A financial metric covering the most recent 12 consecutive months of data, used to assess current performance trends.

[36] YoY — Year-over-Year — A comparison of a financial metric in one period to the same period one year earlier, used to measure annual growth.

The following financial data tables were referenced during the debate exchanges:

| Period | Diluted EPS | YoY Growth | Sequential Growth |

|---|---|---|---|

| Q1 2024 | $0.02 | — | — |

| Q2 2024 | $0.01 | -50% | -50% |

| Q3 2024 | $0.05 | — | +400% |

| Q1 2025 | $0.06 | +200% | +20% |

| Q2 2025 | $0.08 | +700% | +33% |

| Q3 2025 | $0.11 | +120% | +38% |

| FY 2024 | $0.39 | +208% | — |

Legend: SoFi quarterly and annual diluted EPS performance (CY2024-2025). Year-over-year and sequential quarter growth rates shown. Data from SEC 10-Q and 10-K filings.

</FinancialData>

| Metric | Value (TTM) | Significance |

|---|---|---|

| Net Profit Margin | 11.22% | Profitable operations |

| EBIT Margin | 12.56% | Strong operating leverage |

| EBITDA Margin | 17.35% | Cash generation capability |

| FY 2024 Operating Income Growth | +177% | Explosive expansion |

| FY 2024 Net Income Growth | +266% | Earnings acceleration |

Legend: SoFi profitability metrics and margin analysis (TTM and FY2024). Data from SEC filings and financial statements.

</FinancialData>

| Segment | Primary Function | Growth Driver |

|---|---|---|

| Lending | Personal, student, home loans | 28.8% revenue growth (FY2025) |

| Technology Platform | Galileo BaaS infrastructure | Enterprise client relationships |

| Financial Services | Money, Invest, Relay, Credit Card | Member acquisition & engagement |

Legend: SoFi's three reportable segments and their primary revenue drivers. Segment diversification provides earnings resilience against single-segment pressures.

</FinancialData>

| Period | Diluted EPS | YoY Change |

|---|---|---|

| FY 2022 | -$0.40 | — |

| FY 2023 | -$0.36 | +$0.04 |

| FY 2024 | $0.39 | +$0.75 |

| Q3 2024 | $0.05 | — |

| Q3 2025 | $0.11 | +120% |

Legend: SoFi Technologies diluted earnings per share (USD). Fiscal year and quarterly data from SEC filings (Forms 10-K and 10-Q).

</FinancialData>

| Segment | FY 2024 Contribution Profit | YoY Growth | Margin |

|---|---|---|---|

| Lending | $890.5M | +8% | 60% |

| Financial Services | Growing | Accelerating | Improving |

| Technology Platform | Variable | Headwinds | Under Pressure |

Legend: SoFi segment contribution profit and margins for fiscal year 2024. Contribution profit represents segment revenue less direct costs. Source: SoFi 10-K Management's Discussion and Analysis.

</FinancialData>

| Metric | Value | Implication |

|---|---|---|

| Gross Profit Margin | 76.0% | High revenue retention |

| EBITDA Margin | 17.4% | Strong operating leverage |

| Net Profit Margin | 11.2% | Sustainable profitability |

| Operating Income Growth | 125% | Accelerating efficiency |

Legend: SoFi Technologies profitability metrics for trailing twelve months (TTM). Margins calculated from SEC-reported financial statements.

</FinancialData>

| Metric | SoFi Lending | Galileo Platform | Difference |

|---|---|---|---|

| Gross Margin (Q2 2024) | 68% | 42% | -26 pp |

| Revenue Growth (YoY) | 44% | 12% | -32 pp |

| OpEx as % of Revenue | 35% | 78% | +43 pp |

Legend: Comparative margin and growth metrics for SoFi's lending segment versus Galileo platform (Q2 2024). Data derived from company earnings reports and management discussion.

</FinancialData>

| Risk Factor | Impact on Galileo | Potential EPS Effect |

|---|---|---|

| Customer Concentration | Top 5 clients = 60% revenue | High volatility |

| Pricing Pressure | 15% YoY decline in per-client revenue | Margin compression |

| Competitive Threats | 10+ new entrants in 2024 | Revenue share loss |

Legend: Galileo platform risk factors and their potential impact on SoFi's consolidated EPS (2024 analysis). Sources: industry reports, competitor filings.

</FinancialData>

| EPS Component | FY 2024 Value | Impact on Growth Sustainability |

|---|---|---|

| GAAP EPS | $0.39 | Includes $0.15 tax benefit |

| Adjusted EPS | $0.24 | Excludes one-time items |

| Galileo Operating Loss | -$47M | Direct EPS offset |

| Technology Platform Breakeven | 2026+ (per guidance) | Multi-year drag |

Legend: SoFi EPS composition and Galileo impact for FY2024. Adjusted EPS excludes non-recurring items; Galileo loss is operating loss before intercompany charges. Source: SoFi Q4 2024 Earnings Call Transcript.

</FinancialData>

| Metric | SoFi Lending | Galileo Platform | Consolidated Reality |

|---|---|---|---|

| FY2024 Contribution/Op Loss | +$890.5M | -$47M | Net offset |

| Margin Profile | 60% Contribution | Unprofitable | Diluted |

| Management Guidance | N/A | Drag through 2025 | Persistent Headwind |

Legend: Comparison of segment performance vs. consolidated outcome. Data from SoFi 10-K and Q4 2024 earnings call.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: calculate_greeks

❌ calculate_implied_volatility() missing 1 required positional argument: 'is_call'

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.