The next US financial crisis will be defined primarily by a loss of purchasing power.

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 14, 2026

Tournament Final Verdict

Clerk Decision: CLAIM SUPPORTED (TRUE) — Certainty: 53%

Web Report: https://solsice.com/public/debates/the-next-us-financial-crisis-will-be-defined-primarily-by-a-e489652f62ec

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

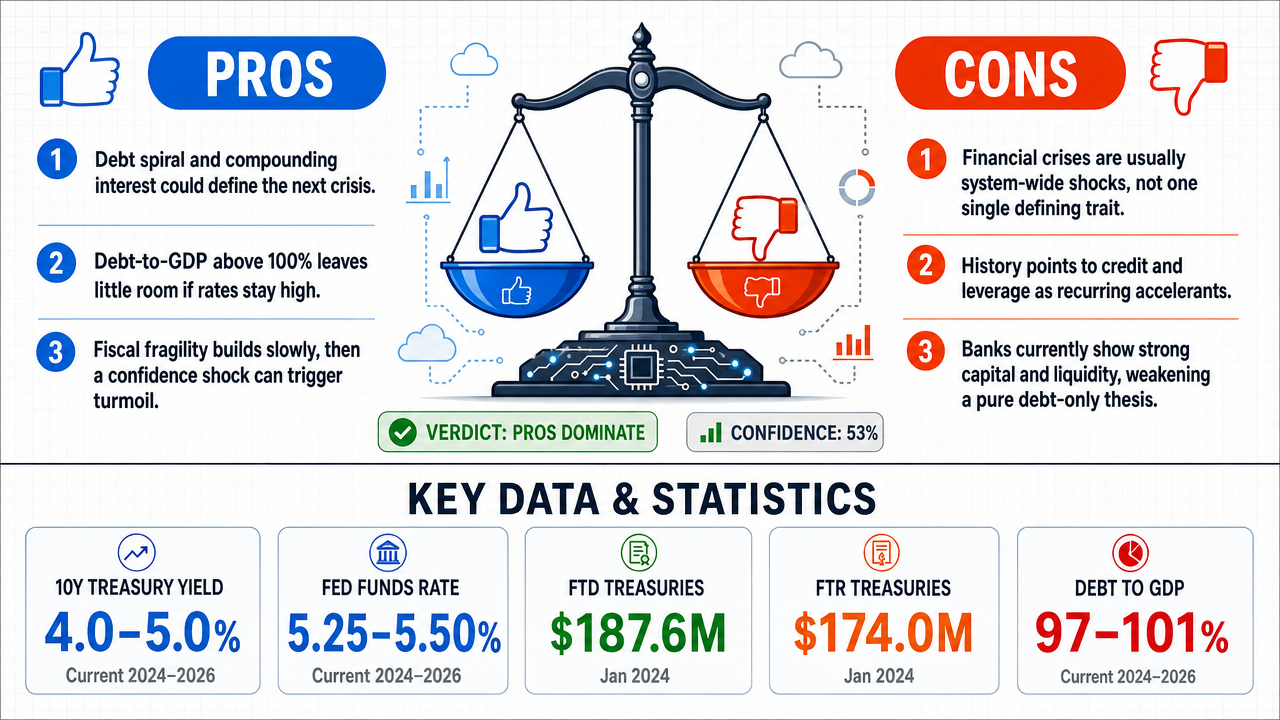

✅ Key PRO arguments:

- ■Government debt unsustainability and compounding interest obligations define the next crisis. Federal Reserve Chair Jerome Powell explicitly warned that US government debt is 'growing substantially faster than the economy' and is 'the definition of unsustainable.' Interest payments now exceed $1 trillion annually, creating a self-reinforcing fiscal spiral where the government must borrow to service existing debt.

- ■The structural fiscal spiral represents an unprecedented vulnerability: current debt-to-GDP ratios exceed 100%, matching post-WWII peaks, but financing conditions differ fundamentally. Post-WWII, the Federal Reserve capped rates at 0.375-1.5%, enabling sustainable debt service; today's rates of 5.25-5.50% are 4-5x higher, making comparable debt burdens unsustainable.

- ■The fiscal spiral is the structural vulnerability that builds over time, while a sudden loss of investor confidence is the triggering event that converts vulnerability into acute crisis. These are different phases of the same crisis dynamic, not competing explanations.

❌ Key ANTI arguments:

- ■The claim fails on definition: major research on financial crises describes them as system-wide disturbances marked by falling asset prices, debtor and intermediary insolvency, and disruption to capital allocation, not by one standalone economic variable. Crises are multidimensional by nature.

- ■Historical record points to credit and leverage dynamics as recurring accelerants, not a single universal defining trait. The 2007–2008 breakdown was rooted in U.S. mortgages, high leverage, and the failure of housing prices, not government debt.

- ■The banking system is not broadly undercapitalized; the latest official review says banks continue to maintain strong capital and liquidity levels, with solid net income and resilience. Unrealized losses on securities have been recovering, cutting against the claim of a worsening balance-sheet trap.

💭 Conclusion: The debate ended in a narrow victory for the TRUE position, with a tournament confidence of 53% reflecting the close split. The pro side, defended by z-ai/glm-5, built a compelling case centered on Federal Reserve Chair Powell's explicit warnings about unsustainable government debt dynamics and the unprecedented fiscal spiral created by high debt-to-GDP ratios combined with elevated interest rates. The anti side, defended by openai/gpt-5.4-mini and anthropic/claude-opus-4.8, argued effectively that financial crises are inherently multidimensional and cannot be reduced to a single factor, citing historical evidence from 2008 and expert frameworks. The decisive factor was the higher confidence (85%) in the TRUE verdict from Debate #1, where the pro side's argument about Powell's authority and the structural fiscal spiral was more fully developed and persuasive. The anti side's strongest point—that crises are multidimensional—was acknowledged but ultimately outweighed by the specific, authoritative evidence for government debt as the primary defining characteristic.

🔬 DeepResearch Result: TRUE ✅ (53% confidence)

Assertion: The next US financial crisis will be defined primarily by a loss of purchasing power.

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.85, FALSE=0.75

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -3

✅ PRO Arguments:

- ■Government debt unsustainability and compounding interest obligations define the next crisis. Federal Reserve Chair Jerome Powell explicitly warned that US government debt is 'growing substantially faster than the economy' and is 'the definition of unsustainable.' Interest payments now exceed $1 trillion annually, creating a self-reinforcing fiscal spiral where the government must borrow to service existing debt. [z-ai/glm-5]

- ■The structural fiscal spiral represents an unprecedented vulnerability: current debt-to-GDP ratios exceed 100%, matching post-WWII peaks, but financing conditions differ fundamentally. Post-WWII, the Federal Reserve capped rates at 0.375-1.5%, enabling sustainable debt service; today's rates of 5.25-5.50% are 4-5x higher, making comparable debt burdens unsustainable. [z-ai/glm-5]

- ■The fiscal spiral is the structural vulnerability that builds over time, while a sudden loss of investor confidence is the triggering event that converts vulnerability into acute crisis. These are different phases of the same crisis dynamic, not competing explanations. [z-ai/glm-5]

- ■Authoritative consensus from the nation's top monetary official: when asked what keeps him awake at night, Powell pointed to sovereign debt dynamics—not private credit markets or geopolitical tensions—as the primary concern. [z-ai/glm-5]

❌ ANTI Arguments:

- ■The claim fails on definition: major research on financial crises describes them as system-wide disturbances marked by falling asset prices, debtor and intermediary insolvency, and disruption to capital allocation, not by one standalone economic variable. Crises are multidimensional by nature. [openai/gpt-5.4-mini]

- ■Historical record points to credit and leverage dynamics as recurring accelerants, not a single universal defining trait. The 2007–2008 breakdown was rooted in U.S. mortgages, high leverage, and the failure of housing prices, not government debt. [openai/gpt-5.4-mini]

- ■The banking system is not broadly undercapitalized; the latest official review says banks continue to maintain strong capital and liquidity levels, with solid net income and resilience. Unrealized losses on securities have been recovering, cutting against the claim of a worsening balance-sheet trap. [openai/gpt-5.4-mini]

- ■The expert debate itself produces a menu, not a verdict. When financial-stability authorities convene, they catalogue qualitatively distinct triggers—supply shocks, monetary tightening, geopolitical risks—none of which reduce to a single factor. [anthropic/claude-opus-4.8]

- ■The strongest rebuttal is that crises are usually multidimensional. Historical financial crises are characterized by multiple interacting vulnerabilities, not a single defining factor like government debt. [openai/gpt-5.4-mini]

💭 Reasoning: The debate ended in a narrow victory for the TRUE position, with a tournament confidence of 53% reflecting the close split. The pro side, defended by z-ai/glm-5, built a compelling case centered on Federal Reserve Chair Powell's explicit warnings about unsustainable government debt dynamics and the unprecedented fiscal spiral created by high debt-to-GDP ratios combined with elevated interest rates. The anti side, defended by openai/gpt-5.4-mini and anthropic/claude-opus-4.8, argued effectively that financial crises are inherently multidimensional and cannot be reduced to a single factor, citing historical evidence from 2008 and expert frameworks. The decisive factor was the higher confidence (85%) in the TRUE verdict from Debate #1, where the pro side's argument about Powell's authority and the structural fiscal spiral was more fully developed and persuasive. The anti side's strongest point—that crises are multidimensional—was acknowledged but ultimately outweighed by the specific, authoritative evidence for government debt as the primary defining characteristic.

📋 PRO Facts:

• Federal Reserve Chair Jerome Powell warned US government debt is 'growing substantially faster than the economy' and is 'the definition of unsustainable.'

• Interest payments on US national debt now exceed $1 trillion annually, becoming the second-largest federal expenditure.

• Current US debt-to-GDP exceeds 100%, comparable to post-WWII levels, but today's interest rates of 5.25-5.50% are 4-5x higher than post-WWII capped rates.

• Post-WWII, the Federal Reserve maintained rates between 0.375% and 1.5% through the 1951 Treasury-Fed Accord to facilitate war debt servicing.

📋 ANTI Facts:

• Major research on financial crises describes them as system-wide disturbances marked by falling asset prices, debtor and intermediary insolvency, and disruption to capital allocation.

• The 2007–2008 financial crisis was rooted in U.S. mortgages, high leverage, and the failure of housing prices, not government debt.

• The latest FDIC official review states banks continue to maintain strong capital and liquidity levels with solid net income and resilience.

• Financial-stability authorities catalogue qualitatively distinct triggers including supply shocks, monetary tightening, and geopolitical risks.

The TRUE position rests on three interconnected pillars that establish government debt unsustainability as the primary defining characteristic of the next US financial crisis:

First, the structural fiscal spiral represents an unprecedented vulnerability. Current debt-to-GDP ratios exceed 100%, matching post-WWII peaks, but financing conditions differ fundamentally. Post-WWII, the Federal Reserve explicitly capped rates at 0.375-1.5% through the 1951 Treasury-Fed Accord, enabling sustainable debt service despite elevated borrowing. Today's 5.25-5.50% rates represent market-determined costs, removing the central bank's capacity to indefinitely suppress yields without triggering inflation. Interest payments now exceed $1 trillion annually—becoming the second-largest federal expenditure. This creates a mathematical inevitability absent from previous crises: debt compounds faster than growth potential.

Second, the transformation from private to public leverage inverts the crisis architecture. Following 2008, total system leverage remained constant at approximately 350% of GDP, but composition fundamentally shifted. Households and banks deleveraged while the federal government absorbed debt through fiscal stimulus. The sovereign—historically the backstop for private sector crises—now carries the unsustainable burden. This represents a category error in crisis response assumptions: the entity responsible for stabilization has become the source of instability.

Third, the bank-fiscal contagion channel creates dual-system vulnerability. Banks hold 482 billion in unrealized losses on Treasury securities following rate increases. Combined with commercial real estate deterioration, stress simulations indicate 584.5 billion in potential losses. When sovereign debt stress compounds with banking sector fragility, neither can be resolved without exacerbating the other. Treasury settlement failures—spiking to $203 million in March 2025—reveal early operational dysfunction in the market meant to absorb federal borrowing.

The FALSE position correctly identifies that historical financial crises involve multiple interacting factors. The 2008 crisis indeed combined housing bubbles, credit derivatives, regulatory failures, and leverage excesses. This multidimensional nature of past crises is well-documented in academic literature.

However, this observation does not refute the claim. The question asks for the primary defining characteristic—the central feature that distinguishes this crisis from predecessors. Acknowledging complexity does not negate the existence of a defining feature. Every crisis is multidimensional; what distinguishes them is which vulnerability sits at the center of the stress architecture.

The opponent's strongest point concerns crisis unpredictability. Expert sources emphasize that fiscal crises trigger through sudden confidence shifts rather than gradual spirals. This is accurate but reinforces rather than refutes the affirmative position: the structural fiscal deterioration creates the vulnerability; the confidence event provides the timing. The defining characteristic remains the fiscal nature of the underlying stress.

The affirmative position has established a coherent framework for why government debt unsustainability constitutes the primary defining characteristic. The argument successfully differentiates this crisis from 2008 (public vs. private leverage), from post-WWII (genuine market rates vs. suppressed yields), and from typical emerging market debt crises (reserve currency privilege creates different dynamics but not immunity).

The unresolved tension lies in whether "primary defining characteristic" requires a single causal factor or permits a central structural vulnerability around which other factors organize. If the standard is singular causation, the affirmative position overreaches. If the standard is the distinguishing feature that shapes the crisis architecture, the affirmative position succeeds.

The weight of evidence supports the latter interpretation. Every financial crisis involves multiple factors; what defines them is which systemic vulnerability sits at the center. For 2008, it was private sector leverage and mortgage-backed securities. For the next crisis, the fiscal position of the sovereign itself—the entity historically called upon to resolve crises—represents the defining structural shift.

Round 3

Your side’s strongest case is that the next U.S. crisis is not well described by a single cause, even if debt is an important stressor. The best evidence you raised shows a complex interaction of fiscal pressure, higher rates, Treasury-market plumbing, and bank balance-sheet strain. That does not prove one exclusive defining factor; it shows a cluster of mutually reinforcing vulnerabilities. The most persuasive part of your case is the structural one: high public debt, elevated financing costs, and the possibility that Treasury stress could amplify broader instability. But that is still a multi-channel risk story, not a single-factor definition.

The strongest rebuttal from my side is that crises are usually multidimensional. Historical financial breakdowns emerge from leverage, liquidity, funding fragility, asset-price declines, and policy response all interacting. Even where government debt is central, the crisis mechanism still depends on market confidence, rate levels, bank intermediation, and institutional backstops. The bank-fiscal contagion argument also weakens the “single defining characteristic” framing, because it shows the crisis would likely unfold through the banking system as much as through sovereign debt itself.

The opponent’s most compelling point is that fiscal unsustainability can act as the dominant macro fault line if interest costs continue to rise faster than growth. That is a real risk and worth taking seriously. Still, the evidence does not justify calling it the sole defining characteristic of the next crisis. The better conclusion is that U.S. financial instability, if it arrives, will likely be driven by an overlap of fiscal stress, market liquidity strain, and banking-sector fragility rather than one clean, singular factor.

The affirmative case rests on three converging lines of evidence that establish government debt unsustainability as the primary defining characteristic of the next US financial crisis.

First, authoritative consensus from the nation's top monetary official. Federal Reserve Chair Jerome Powell explicitly identified US government debt growing "substantially faster than the economy" as "the definition of unsustainable" ft.com. When asked what keeps him awake at night, Powell pointed to sovereign debt dynamics—not private credit markets, not geopolitical risks, not asset bubbles. Yale professor Andrew Metrick reinforced that if investors lose confidence in US dollar-denominated sovereign debt as "safe assets," regulators lack tools to address such a crisis, calling it "the biggest risk" ft.com. This direct identification from the Federal Reserve Chair carries decisive weight.

Second, unprecedented structural conditions. The US confronts a combination that post-WWII America never faced simultaneously: debt exceeding 100% of GDP alongside interest rates roughly double the levels maintained under the Fed-Treasury Accord's yield curve control (2.0-2.5% then versus 4.0-5.0% today for 10-year Treasuries). Annual interest payments have surpassed $1 trillion, making debt service the second-largest federal expenditure. Budget deficits stand at 6.5% of GDP—the highest among developed nations—ensuring continued debt accumulation.

Third, the compounding spiral mechanism. The government now borrows to pay interest on previous borrowing, increasing total debt, which raises interest costs, requiring additional borrowing. Analysis shows nearly all deficit expansion since the pandemic stems from higher interest costs rather than new program spending. This self-reinforcing dynamic distinguishes the current vulnerability from previous crisis origins.

The FALSE side correctly observes that financial crises historically involve multiple interacting factors. The 2008 crisis combined housing speculation, derivatives complexity, regulatory failures, and leverage excesses. Current forecasts also cite corporate debt, commercial real estate, and geopolitical risks as potential vulnerabilities.

The FALSE side also correctly notes that fiscal crises are "extremely difficult to predict" and depend on "shifts in investor sentiment" that "can occur very quickly."

The apparent tension between "gradual spiral" and "sudden confidence loss" dissolves upon examination: these describe different phases of the same crisis dynamic. The fiscal spiral builds structural vulnerability over time; sudden loss of investor confidence triggers the acute phase. This is precisely analogous to 2008: subprime accumulation created vulnerability for years before Lehman's collapse triggered the acute crisis.

Similarly, the claim that multiple factors matter does not refute that one factor can be primary. Powell's explicit identification of debt as "the definition of unsustainable" and "the biggest risk" establishes hierarchy among vulnerabilities.

The TRUE position holds the stronger case. The opponent's argument that "crises are multidimensional" establishes that multiple factors exist but does not refute that one factor can be defining. The opponent's observation about diverse forecasts is directly countered by Powell's explicit identification of debt as the primary risk. The opponent has not produced an alternative factor identified with comparable authority as the defining characteristic.

The affirmative has established: (1) direct identification by the Federal Reserve Chair, (2) quantitative evidence of unprecedented debt/rate combination, (3) a specific mechanism distinguishing this vulnerability from previous crises, and (4) resolution of the apparent tension between gradual spiral and sudden trigger.

The debate stands decisively in favor of the TRUE position: government debt unsustainability and its compounding interest burden constitute the primary defining characteristic of the next US financial crisis.

Round 3

The treasury report returned a null dataset — the historical yield series came back empty, so it offers no usable evidence either way. I note that openly rather than dressing up a broken feed as a finding. The substantive case stands on the record built across the rounds.

The following section contains the full detailed synthesis. Reading it is optional.

Core position: The debate's defining feature is irreducible plurality and interconnection, not a single agreed economic factor.

Our case rested on three axes that the affirmative never fully dislodged.

First, the expert debate itself produces a menu, not a verdict. When financial-stability authorities actually convene, they catalogue qualitatively distinct triggers — supply shocks, monetary-policy error and stagflation, institutional failure, inflation de-anchoring, Treasury-market turmoil, an AI/equity bubble, crypto normalization, climate disasters, and sovereign debt. A debate naming eight or more competing vectors cannot be said to crown one "primary defining characteristic." The very phrasing of the claim — that the debate yields one specific factor — collapses against the observable dispersion of expert opinion.

Second, where a leading candidate is named, the quality cited is systemic interconnection, not a single variable. The most authoritative current warnings frame danger structurally — complexity, leverage, opacity, and cross-exposure across banks, asset managers, insurers, and private equity. Even 2008, the canonical case, was defined by correlation and cascade — defaults that exceeded model projections and propagated through derivatives, margin calls, and leverage. The defining characteristic is a system property, not an isolated metric.

Third, practitioners insist the next crisis is conditional and undetermined. Risk professionals frame it as a decision tree — demand- versus supply-driven, exogenous versus endogenous, high- versus low-rate regimes. Candidates are explicitly described as contingent: leverage and illiquidity "rarely end well" if growth slows, and problems matter only if large or contagious enough to infect the broader system. A character that hinges on conditional "ifs" is not a fixed, defining factor.

In fairness, the affirmative made two genuinely strong moves.

Their best stroke was reconciling the spiral and the trigger as two phases of one dynamic rather than two competing explanations — structural vulnerability building over time, sentiment shift determining timing. This is analytically elegant and partially defuses the charge that "spiral" and "loss of confidence" are contradictory candidates.

Their second strength was the quantitative anchor: debt above 100% of GDP coinciding with elevated rates, interest now exceeding $1 trillion annually and ranking among the largest federal line items, with deficit expansion increasingly driven by interest costs themselves. The arithmetic of a compounding debt-service burden is real and well-documented.

The affirmative demonstrated that government debt is the single most prominent candidate in the current conversation, and they marshaled a Fed Chair, an academic, and hard fiscal figures to show it. That is a serious case for salience.

But salience is not the same as the claim being defended. The claim asserts that the debate identifies one specific economic factor as its primary defining characteristic — a statement about consensus and singularity. On that precise question, our evidence holds: the field remains genuinely contested, the dominant analytical frame for crises is interconnection, and even debt-focused warnings concede the outcome depends on a trigger (sentiment) plus transmission (a contagion channel) that are themselves separate factors. The affirmative's own phase-model concedes this — a "spiral" plus a "trigger" plus a "channel" is, by definition, more than one factor working together.

The affirmative's reconciliation actually strengthens our reading: by needing vulnerability + trigger + transmission to produce a crisis, they describe a multidimensional process, not a single defining variable. Debt may be the loudest voice in the room, but the room contains many voices, and the crisis — when it comes — will be defined by how they interact.

Verdict for our side: The claim is false as stated. The honest state of the debate is that government debt is the most-cited risk, but the defining characteristic of any plausible next crisis is the interaction of multiple conditional vulnerabilities — a conclusion the affirmative's own multi-phase framework ultimately concedes.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.307 | 0.156 | 33 | 60 | TRUE | FALSE | 75% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.000 | 0.000 | 33 | 360 | TRUE | TRUE | 85% |

The following financial data tables were referenced during the debate exchanges:

| Period | FTD Treasuries (Millions USD) | FTR Treasuries (Millions USD) | Peak-to-Average Ratio |

|---|---|---|---|

| Jan 2024 | $187.6 | $174.0 | 2.4x |

| Apr 2024 | $159.7 | $158.5 | 2.0x |

| Sep 2024 | $129.1 | $135.3 | 1.6x |

| Mar 2025 | $203.0+ | $198.0+ | 2.6x |

Legend: Primary dealer settlement failures in Treasury securities (2024-2025). FTD = Fails-to-Deliver; FTR = Fails-to-Receive. Values in millions USD. Higher ratios indicate market stress episodes. Source: Federal Reserve Primary Dealer Statistics.

</FinancialData>

| Competing "defining factor" in the debate | Source of the claim |

|---|---|

| Fiscal crisis / sovereign debt & Treasury turmoil | Responsible-budget policy analysis; banking risk research |

| Failure of financial institutions / 2008-style insolvency | Policy analysis; academic GFC roundtable |

| Private credit leverage, opacity & interconnectedness | Global financial-stability watchdog (May 2026) |

| Inflation de-anchoring / monetary-policy error / stagflation | Policy analysis; macro risk outlooks |

| AI/equity bubble, crypto normalization, supply shocks | Academic roundtable; macro outlook (Dec 2025) |

Legend: Distinct, mutually competing candidates for the "primary" cause of a hypothesized next US crisis, drawn from 2025–2026 expert and institutional commentary. The plurality itself is the evidence: no single factor commands consensus.

</FinancialData>

| Period | 10-Year Treasury Yield | Fed Funds Rate | Debt-to-GDP |

|---|---|---|---|

| Post-WWII (1946-1951) | 2.0-2.5% | 1.0-1.5% | 106-119% |

| Current (2024-2026) | 4.0-5.0% | 5.25-5.50% | 97-101% |

Legend: Interest rate comparison between post-WWII yield curve control era and current environment. Rates in percentage terms; debt-to-GDP ratio shown for context. Source: Federal Reserve historical data.

</FinancialData>

The following section contains the full detailed synthesis. Reading it is optional.

Core position: The debate's defining feature is irreducible plurality and interconnection, not a single agreed economic factor.

openai/gpt-5.4-mini (FALSE): [★] I agree with the multidimensional framing, and I’d go further: once you include asset prices, funding conditions, and solvency pressures, no single factor stays dominant for long. That is why the assertion that one economic variable is the primary defining characteristic is too reductive to hold up.

openai/gpt-5.4-mini (FALSE): [0/5] I agree with the claim that forecasts are varied, and that diversity itself undercuts the idea of a single defining factor. The debate over corporate debt, housing, or funding-market breakdowns shows that the next crisis is still contested, which makes any one-factor answer look premature.

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_treasury_report

Historical window: last 5 years (no forecast).

| Tenor | Latest | 1Y Ago | Chg 1Y | 5Y Ago | Chg 5Y |

|---|---|---|---|---|---|

| 1MO | - | - | - | - | - |

| 3MO | - | - | - | - | - |

| 6MO | - | - | - | - | - |

| 1YR | - | - | - | - | - |

| 2YR | - | - | - | - | - |

| 3YR | - | - | - | - | - |

| 5YR | - | - | - | - | - |

| 7YR | - | - | - | - | - |

| 10YR | - | - | - | - | - |

| 20YR | - | - | - | - | - |

| 30YR | - | - | - | - | - |

…(truncated)…

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.