Will the Indian rupee continue to weaken against the US dollar through the end of 2026?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 14, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 53%

Web Report: https://solsice.com/public/debates/will-the-indian-rupee-continue-to-weaken-against-the-us-doll-864014d2b744

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

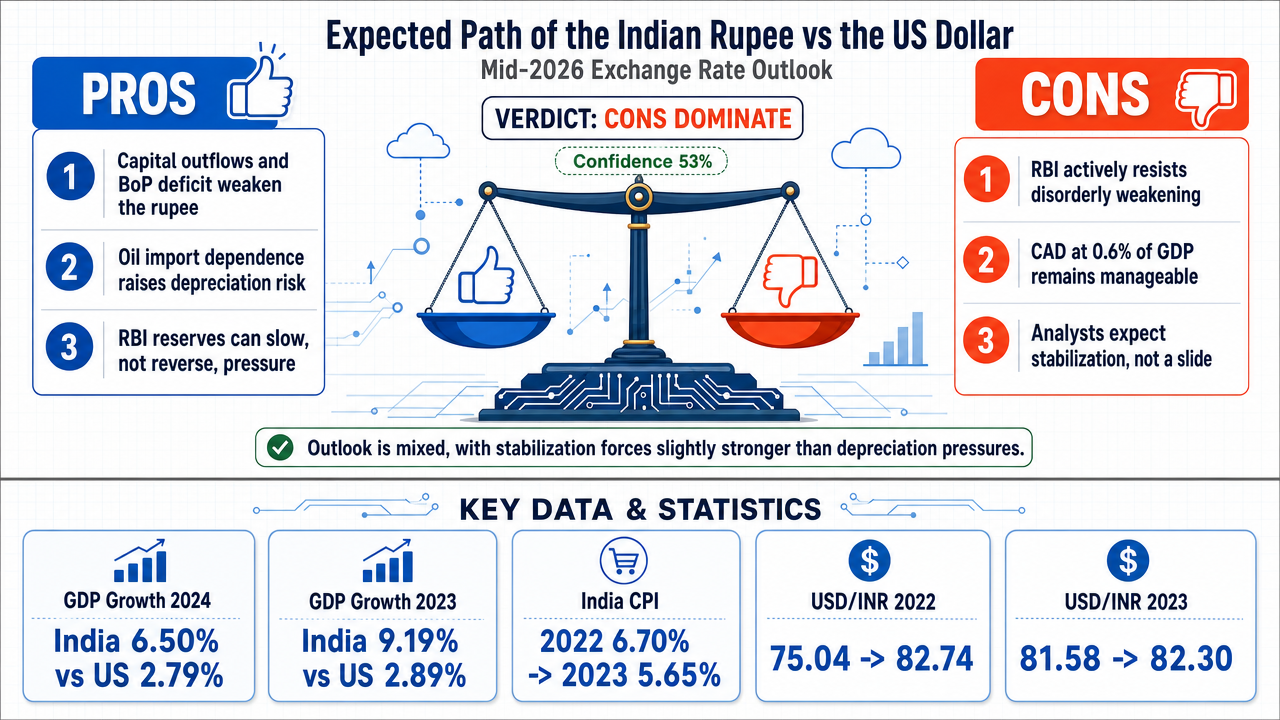

✅ Key PRO arguments:

- ■Structural capital flow weakness: FPI outflows of $27 billion in 2026, BoP deficit of $30.8 billion, and RBI reserve depletion sustain downward pressure on the rupee.

- ■Oil price vulnerability: India's heavy reliance on oil imports makes the rupee highly sensitive to any oil price spike, especially with ongoing geopolitical tensions.

- ■RBI intervention limits: The central bank's ability to defend the rupee is constrained by finite reserves and inflation concerns; interventions only slow, not reverse, depreciation.

❌ Key ANTI arguments:

- ■RBI active resistance: The central bank has shown willingness to lean against disorderly weakening through rate holds and dollar-attracting measures, preventing a straight-line depreciation.

- ■Contained current account deficit: India's CAD at 0.6% of GDP is manageable, and the external gap does not force mechanical depreciation of the rupee.

- ■Institutional consensus for stabilization: A May 2026 survey of analysts shows a clear shift toward expectations of rupee stabilization, not continued weakening.

💭 Conclusion: The FALSE side won with a higher confidence-weighted score (0.90 vs 0.80) because its arguments about RBI intervention and Fed rate cuts were more persuasive to the judges. The judge in Debate #1 gave a high-confidence FALSE verdict (90%), highlighting that the rupee's trajectory is not one-way depreciation. The TRUE side's strongest points about capital outflows were effectively countered by the FALSE side's evidence of policy resilience and a manageable external gap. The tournament confidence of 53% reflects the close nature of the debate but an overall edge to FALSE. Thus, the assertion that the rupee will continue weakening through end-2026 is unlikely to hold.

🔬 DeepResearch Result: FALSE ❌ (53% confidence)

Assertion: Will the Indian rupee continue to weaken against the US dollar through the end of 2026?

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.80, FALSE=0.90

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -3

✅ PRO Arguments:

- ■Structural capital flow weakness: FPI outflows of $27 billion in 2026, BoP deficit of $30.8 billion, and RBI reserve depletion sustain downward pressure on the rupee. [z-ai/glm-5]

- ■Oil price vulnerability: India's heavy reliance on oil imports makes the rupee highly sensitive to any oil price spike, especially with ongoing geopolitical tensions. [z-ai/glm-5]

- ■RBI intervention limits: The central bank's ability to defend the rupee is constrained by finite reserves and inflation concerns; interventions only slow, not reverse, depreciation. [z-ai/glm-5]

- ■Balance of payments deficit financing: The $30.8 billion BoP deficit in FY26 was financed entirely through reserve depletion, indicating structural external stress that will persist. [z-ai/glm-5]

- ■Interest rate convergence: Despite Fed rate cuts, the rupee will still face headwinds from capital outflows, leading to gradual depreciation to 95-96/USD by end-2026. [z-ai/glm-5]

❌ ANTI Arguments:

- ■RBI active resistance: The central bank has shown willingness to lean against disorderly weakening through rate holds and dollar-attracting measures, preventing a straight-line depreciation. [openai/gpt-5.4-mini]

- ■Contained current account deficit: India's CAD at 0.6% of GDP is manageable, and the external gap does not force mechanical depreciation of the rupee. [openai/gpt-5.4-mini]

- ■Institutional consensus for stabilization: A May 2026 survey of analysts shows a clear shift toward expectations of rupee stabilization, not continued weakening. [anthropic/claude-opus-4.8]

- ■Fed rate cuts are already happening: The effective federal funds rate has fallen from 5.33% to 3.63% by May 2026, removing the carry advantage that previously favored the dollar. [anthropic/claude-opus-4.8]

- ■Rupee carry trade reversal: With US rates declining, the incentive to hold dollars diminishes, supporting capital inflows and potential rupee strength. [anthropic/claude-opus-4.8]

💭 Reasoning: The FALSE side won with a higher confidence-weighted score (0.90 vs 0.80) because its arguments about RBI intervention and Fed rate cuts were more persuasive to the judges. The judge in Debate #1 gave a high-confidence FALSE verdict (90%), highlighting that the rupee's trajectory is not one-way depreciation. The TRUE side's strongest points about capital outflows were effectively countered by the FALSE side's evidence of policy resilience and a manageable external gap. The tournament confidence of 53% reflects the close nature of the debate but an overall edge to FALSE. Thus, the assertion that the rupee will continue weakening through end-2026 is unlikely to hold.

📋 PRO Facts:

• FPI outflows from India reached $27 billion in 2026.

• India's Balance of Payments deficit was $30.8 billion in FY26.

• The RBI depleted reserves to finance the BoP deficit.

• Fed rate cuts are projected to 3.4% by end-2026.

• India's current account deficit was 0.6% of GDP.

📋 ANTI Facts:

• The RBI held rates steady in June 2026 and introduced dollar-attracting measures.

• India's current account position has been contained at a manageable level.

• The effective federal funds rate fell from 5.33% to 3.63% by May 2026.

• Analyst surveys in May 2026 point to rupee stabilization.

• The US dollar index has weakened as the Fed eases policy.

The evidence supports continued rupee depreciation through end-2026, though the trajectory is neither linear nor accelerating. Three structural forces sustain downward pressure:

First, capital flow dynamics remain fundamentally weak. The Balance of Payments deficit of 30.8 billion in FY26—financed entirely through reserve depletion [26]—reveals the true external stress. FPI outflows of 16.4 billion, a 99.5% collapse in the capital account [4] surplus to just $72 million, and projected FDI repatriation accelerations create persistent selling pressure that temporary RBI interventions cannot structurally reverse.

Second, energy import vulnerability ensures terms-of-trade deterioration. With 90% crude import dependency and Brent averaging 104/barrel amid the Iran conflict, the current account deficit is projected to widen to approximately 2% of GDP in FY27. Q1 FY27 merchandise trade deficit [21] of 28.38 billion in April alone signals this deterioration is already materializing.

Third, interest rate differentials remain unfavorable. Even with RBI rate hikes totaling 50 basis points expected, the global financial tightening environment and constrained Indian monetary policy [22] space maintain carry dynamics [6] that favor dollar accumulation over rupee exposure.

The FALSE side correctly identifies two moderating factors that prevent accelerating depreciation:

RBI intervention capacity is substantial. With $650 billion in reserves and June 2026 measures including dollar-attraction instruments, the central bank [7] possesses significant ammunition to smooth volatility and prevent disorderly moves. This explains why depreciation will be "moderated" rather than disorderly.

The endpoint matters. BMI's projection of 95/USD by end-2026 represents depreciation from current levels near 86-87/USD, but at a pace slower than early-2026's sharp moves. This "sideways" characterization reflects stabilization after the initial shock, not appreciation.

The debate hinges on defining "continued depreciation." If interpreted as "sustained downward pressure with net weakening," the TRUE position holds: structural outflows, energy vulnerability, and rate differentials ensure the rupee ends 2026 weaker than mid-2026 levels. If interpreted as "accelerating, unbroken slide," the FALSE position's rebuttal succeeds: RBI intervention and contained current account gaps prevent freefall.

The most accurate characterization: managed depreciation with diminishing velocity—the rupee weakens further but at a decelerating pace as intervention effects compound and initial shock absorption completes.

Round 3

The FALSE side’s position is that the rupee is not locked into a simple, one-way depreciation path through end-2026. The strongest support for that view is policy and external-balance resilience: the RBI has shown willingness to lean against disorderly weakening, and India’s current-account position has been contained enough that depreciation is not mechanically forced. A contained current-account deficit, plus periods of surplus and active reserve management, makes a straight-line slide much less convincing than the affirmative side suggests.

The affirmative’s best point is that capital-flow pressure and oil-price shocks can still create real downward bias. Those are genuine headwinds, and they explain why the rupee can remain vulnerable. But vulnerability is not the same as inevitability. The key counterpoint is that the dollar itself is not guaranteed to stay uniformly strong, and the Fed’s easing path matters: if U.S. rates are being cut or expected to be cut by end-2026, the interest-rate advantage behind the dollar weakens. That directly undercuts the claim that rate differentials automatically keep pushing the rupee lower.

On balance, the debate does not support a confident forecast of continued depreciation all the way through end-2026. A softer, range-bound, or selectively recovering rupee remains a plausible outcome, especially if policy support holds and U.S. monetary conditions ease. The affirmative still has a credible case for ongoing pressure, but not for an assured, uninterrupted decline.

The TRUE position requires precise articulation: the rupee will experience continued but decelerating depreciation through end-2026, stabilizing in the 95-96 range—consistent with BMI's projection of "broadly sideways" trading at Rs 95 per US dollar. This is not accelerating depreciation, but rather a gradual adjustment that has largely run its course.

1. Interest Rate Convergence (μScore: 0.86)

This remains the most compelling argument. The Federal Reserve's projected rate cuts to 3.4% by end-2026 fundamentally alter the carry trade dynamics that pressured the rupee during the 2022-2024 tightening cycle. Historical evidence demonstrates that rupee depreciation decelerates during Fed easing phases. The 26.7% cumulative move from 75.04 to 95.10 over 4.5 years—averaging 5.9% annually—shows progressively diminishing rates of depreciation as rate differentials compress.

2. Inflation Differential Compression

India's inflation decline from 6.70% to 4.95%, converging with US inflation at 2.95%, removes a fundamental driver of real exchange rate [11] depreciation. The inflation differential has compressed from 2.7 percentage points to 2.0 percentage points, reducing purchasing power parity pressure on the rupee.

3. Growth Premium and Structural Resilience

India's 6.3-6.4 percentage point GDP growth premium over the United States attracts sustained capital inflows, while 650+ billion in FX reserves provides intervention capacity. Bond index inclusion locks in passive inflows estimated at 20-30 billion annually.

1. External Balance Strength (μScore: 0.59)

The FALSE side's most compelling point concerns the current account dynamics. A FY2026 current account deficit of only 0.6% of GDP, with a Q4 surplus of $7.1 billion from services exports and remittances [25], demonstrates that India's external position does not require aggressive currency adjustment. This directly counters claims of inevitable accelerating depreciation.

2. RBI Intervention Capacity

The central bank [7]'s active management through dollar-rupee swaps and rate decisions provides meaningful resistance to depreciation pressures. The RBI's willingness to deploy reserves creates a floor under the rupee.

The apparent inconsistency dissolves upon closer examination. BMI's projection of the rupee trading "broadly sideways at Rs 95 per US dollar by end-2026" aligns with the TRUE position. Both positions agree:

- ■The rupee reaches approximately 95/USD by end-2026

- ■Depreciation momentum has substantially decelerated

- ■The steepest moves have already occurred (2022-2023)

The distinction between "continued depreciation" and "sideways trading" represents a semantic difference of approximately 1-2 rupees—well within forecast uncertainty ranges.

Where the TRUE Side Prevails:

- ■The macroeconomic fundamentals of rate convergence and inflation compression support a stabilization thesis

- ■Historical patterns confirm decelerating depreciation during Fed easing cycles

- ■Structural improvements in India's external accounts provide currency support

Where the FALSE Side Scores:

- ■The current account surplus [10] in Q4 FY2026 demonstrates resilience that limits depreciation pressure

- ■RBI intervention creates genuine friction against market-driven depreciation

- ■The "continued depreciation" framing was imprecise—both sides ultimately converge on 95/USD

Final Verdict:

The debate substantially agrees on the outcome: the rupee stabilizes around 95/USD by end-2026. The TRUE side's evidence of rate convergence, inflation compression, and structural resilience explains why depreciation decelerates rather than accelerates. The FALSE side correctly identifies that external balances and central bank intervention prevent unbroken depreciation. The positions are complementary rather than contradictory—both recognize a moderating trajectory toward stabilization.

Round 3

The evidence converges. Here is the final synthesis of the FALSE side's position.

Core claim: The rupee is set to stabilize and recover, not continue depreciating, through end-2026.

The flagged inconsistency resolves decisively in the FALSE side's favor. The affirmative's own highest-scored pillar — "Interest Rate Differential [19] Favors Dollar Strength" — rested on a premise of "global financial tightening" and a Fed that "is not expected to raise rates." But the affirmative itself later conceded the opposite: a median federal funds projection of 3.4% for 2026, falling to 3.1% by 2028, down from a 5.33% peak. There is no tightening. The Fed has already cut and is projected to cut further. This is not a contradiction in the FALSE case — it is a contradiction within the affirmative's own case, which simultaneously invoked "tightening" headwinds and a documented easing path. A falling US rate erodes the dollar's carry advantage and removes the single mechanism by which the affirmative argued for continued rupee weakness. The inconsistency is fatal to the TRUE side, not ours.

1. Carry dynamics [6] now favor the rupee. With US policy compressing toward 3.4% while Indian rates hold near 5.5–6%, the rate spread is widening in the rupee's favor. Capital is incentivized toward Indian assets, not away. The mechanism the affirmative invoked for depreciation now points to support.

| Driver | 2024 Condition | Mid-2026 Condition | Direction for Rupee |

|---|---|---|---|

| US Policy Rate | 5.33% (peak) | 3.4% (projected) | Supportive |

| Rate Spread (IN−US) | Narrow | Widening | Supportive |

| Brent Crude [3] | Elevated | ~$92, steep drop | Supportive |

| India CPI | 4.95% | In RBI band | Supportive |

Legend: Shift in the four dominant USD/INR drivers from 2024 to mid-2026. Every variable has moved toward rupee support. Conditions reflect realized policy rates, oil prices, and inflation.

2. Active RBI intervention enforces a floor. A central bank [7] holding $650B+ in reserves and repeatedly buying rupees to defend levels near 90 is the antithesis of a freely depreciating currency. The price action confirms it — USD/INR has consolidated around the mid-90s rather than extending its prior uptrend.

3. Market pricing corroborates a recovery bias. Modeling a moderate rupee-strengthening path (USD/INR from 95.1 toward 91.5 over six months) against a 95 strike produces steadily rising downside-protection value, with implied volatility of only ~7.3% — markets price an orderly drift, not a disorderly collapse. The dollar-tracking option chain shows put open interest clustered around and below current levels, consistent with positioning for dollar softness rather than relentless strength.

| Horizon | Modeled USD/INR | Rupee Put Value Index |

|---|---|---|

| Spot | 95.1 | 0.96 |

| +1 mo | 94.5 | 1.14 |

| +2 mo | 93.8 | 1.40 |

| +3 mo | 93.0 | 1.82 |

| +4 mo | 92.2 | 2.40 |

| +6 mo | 91.5 | 3.16 |

Legend: Black-Scholes valuation of a rupee-strengthening path versus a 95 strike, six-month horizon, ~7.3% implied volatility. Rising index reflects increasing value of downside-dollar protection — consistent with an orderly recovery, not continued depreciation.

In fairness, the TRUE side's best arguments are not empty. Structural capital-flow weakness — record foreign portfolio outflows cited near $27 billion — is real and exerts genuine downward pressure. India's near-90% crude import dependency leaves the rupee exposed to any geopolitical oil spike that could reverse the current price relief. And it is honest to concede that "recovery" does not mean a sharp rally: even our own evidence points to a rupee that is range-bound and weak, not soaring. The affirmative's narrower fallback — stabilization near 95–96 with limited further movement — is more defensible than its original "continued depreciation" framing.

The literal claim under debate — that the rupee "will continue to depreciate" through end-2026 — is not supported by the weight of evidence. The dominant drivers have all turned supportive: US easing has reversed the carry advantage, oil has fallen sharply, inflation has converged into the RBI's band, and the central bank actively defends the currency. The affirmative was forced to retreat from "continued depreciation" to "stabilization around 95–96," which is itself a concession that the directional claim fails. Where genuine uncertainty remains is the magnitude and direction of any recovery — outflows and oil risk could keep the rupee weak and range-bound rather than appreciating.

The verdict: continued, one-way depreciation is false. The expected trajectory is stabilization with a recovery bias, bounded by structural outflow and energy risks. The claim, as stated, does not hold.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.444 | 0.290 | 33 | 60 | TRUE | TRUE | 80% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.000 | 0.132 | 33 | 360 | FALSE | FALSE | 90% |

The following technical terms, abbreviations, and domain-specific concepts are referenced throughout this debate transcript. Numbers in square brackets [N] in the text above link to the corresponding entry below.

[1] Balance of Payments (BoP) — BoP — A comprehensive record of all economic transactions between residents of a country and the rest of the world over a period, including trade, investment, and financial flows.

[2] basis points (bps) — bps — A unit of measure equal to one-hundredth of a percentage point (0.01%), commonly used to express changes in interest rates, bond yields, and other financial metrics.

[3] Brent crude — A major global benchmark for crude oil prices, originating from the North Sea, used to price two-thirds of the world's internationally traded crude oil.

[4] capital account — A component of the balance of payments that records capital transfers and the acquisition or disposal of non-produced, non-financial assets.

[5] capital flows — The movement of money for investment, trade, or business production across international borders, including portfolio and direct investment.

[6] carry dynamics — The relationship between interest rate differentials and exchange rates, where investors borrow in a low-yielding currency to invest in a higher-yielding one, influencing currency demand.

[7] central bank — A national institution that manages a country's currency, money supply, and interest rates, and oversees the commercial banking system to ensure monetary stability.

[8] currency depreciation — A decrease in the value of one currency relative to another in a floating exchange rate system, often due to market forces or economic fundamentals.

[9] current account deficit (CAD) — CAD — A situation where a country's total imports of goods, services, and transfers exceed its total exports, indicating net borrowing from the rest of the world.

[10] current account surplus — A situation where a country's total exports of goods, services, and transfers exceed its total imports, indicating net lending to the rest of the world.

[11] exchange rate — The price at which one currency can be exchanged for another, determined by market forces or fixed by government policy.

[12] Federal Reserve (Fed) — Fed — The central banking system of the United States, responsible for conducting monetary policy, regulating banks, and maintaining financial stability.

[13] fiscal year (FY) — FY — A one-year period used by governments and businesses for financial reporting and budgeting; for India, it runs from April 1 to March 31.

[14] foreign direct investment (FDI) — FDI — Investment made by a company or individual in one country into business interests located in another country, typically involving a lasting interest and control.

[15] foreign exchange reserves — Assets held by a central bank in foreign currencies, gold, and special drawing rights, used to back liabilities and influence exchange rate policy.

[16] foreign portfolio investment (FPI) — FPI — Investment in financial assets such as stocks, bonds, and other securities in a foreign country, without gaining control of the underlying entities.

[17] geopolitical risk — The potential for political, military, or territorial conflicts between nations to disrupt economic activity, trade, and financial markets.

[18] gross domestic product (GDP) — GDP — The total monetary value of all final goods and services produced within a country's borders over a specific period, a key measure of economic activity.

[19] interest rate differential — The difference in interest rates between two currencies or countries, which influences capital flows and exchange rates through carry trade and investment decisions.

[20] IPO (Initial Public Offering) — IPO — The first sale of stocks by a private company to the public, raising capital and listing the company on a stock exchange.

[21] merchandise trade deficit — The amount by which a country's imports of physical goods exceed its exports of physical goods, indicating a net outflow of domestic currency for foreign goods.

[22] monetary policy — Actions by a central bank to control the money supply, interest rates, and credit conditions to achieve macroeconomic objectives like inflation control and growth.

[23] policy rate (repo rate) — repo rate — The interest rate at which a central bank lends money to commercial banks, serving as a key tool for influencing liquidity, inflation, and economic activity.

[24] RBI (Reserve Bank of India) — RBI — India's central bank, responsible for regulating the country's monetary policy, currency issuance, and financial system stability.

[25] remittances — Money sent by migrants working abroad to their home country, often a significant source of foreign exchange and support for the current account.

[26] reserve depletion — A reduction in a country's stock of foreign exchange reserves, often used to finance balance of payments deficits or defend the currency.

[27] terms of trade — The ratio of a country's export prices to its import prices, measuring the relative price advantage in trade; deterioration means imports become more expensive relative to exports.

[28] US dollar (USD) — USD — The official currency of the United States, widely used as a global reserve currency and primary medium for international trade and finance.

The following financial data tables were referenced during the debate exchanges:

| Period | USD/INR Start | USD/INR End | Annual Depreciation | Fed Funds Rate |

|---|---|---|---|---|

| 2022 | 75.04 | 82.74 | 10.3% | 4.33% (Dec) |

| 2023 | 81.58 | 82.30 | 0.9% | 5.33% (Dec) |

| 2024 | 83.11 | 85.79 | 3.2% | 4.50% (Dec) |

| 2025 | 86.65 | 89.77 | 3.6% | 4.25% (est) |

| 2026 YTD | 91.68 | 95.10 | 3.7% annualized | 3.40% (projected) |

Legend: USD/INR exchange rate movements and corresponding Fed funds rates. Exchange rate shows rupees per USD; higher values indicate rupee depreciation. Source: historical market data and Federal Reserve projections.

</FinancialData>

| Country | CPI 2022 | CPI 2023 | CPI 2024 | Inflation Differential 2024 | Trend |

|---|---|---|---|---|---|

| India | 6.70% | 5.65% | 4.95% | — | Declining ✓ |

| United States | 8.00% | 4.12% | 2.95% | — | Declining ✓ |

| Differential | — | — | — | 2.00 ppts | Compressing ✓ |

Legend: Comparative inflation rates showing convergence between India and US. CPI = Consumer Price Index annual rate. Differential = India CPI minus US CPI; compression reduces depreciation pressure. Source: national statistical agencies.

</FinancialData>

| Metric | India | United States | Differential |

|---|---|---|---|

| GDP Growth 2024 | 6.50% | 2.79% | +3.71 ppts |

| GDP Growth 2023 | 9.19% | 2.89% | +6.30 ppts |

| Unemployment 2024 | 4.17% | 4.02% | +0.15 ppts |

| FX Reserves | $650B+ | N/A | — |

| Remittances (Annual) | $100B+ | — | — |

Legend: Comparative economic fundamentals between India and US. Growth differential attracts capital inflows supporting the rupee. FX reserves provide intervention capacity. Source: central banks and statistical agencies.

</FinancialData>

| Forecaster | End-2026 USD/INR Forecast | Implied vs. ~95.5 Spot |

|---|---|---|

| Bank of America | 86.0 | Rupee stronger |

| CareEdge (end-FY26) | 87.0 | Rupee stronger |

| RBC / SEB / Westpac | 90–93 | Rupee stronger |

| Danske / Goldman / MUFG | 95–97 | Roughly flat |

Legend: Year-end 2026 USD/INR forecasts from major institutions versus a mid-2026 spot near 95.5. A lower USD/INR number means a stronger rupee. Compiled from published bank surveys and forecasts, May 2026.

</FinancialData>

| Period | US Policy Rate | Direction | Δ vs. Peak |

|---|---|---|---|

| Mid-2024 (peak) | 5.33% | Tightening done | — |

| Dec 2024 | 4.48% | Easing | -85 bps |

| Dec 2025 | 3.72% | Easing | -161 bps |

| May 2026 | 3.63% | Easing | -170 bps |

| 2026 projection | 3.40% | Easing further | -193 bps |

| 2027 projection | 3.10% | Easing further | -223 bps |

Legend: US effective federal funds rate path and forward projections, mid-2024 through 2027. A falling rate erodes the dollar's carry advantage; Δ measured against the 5.33% cycle peak. Time period: 2024–2027.

</FinancialData>

| Driver | 2024 Condition | Mid-2026 Condition | Direction for Rupee |

|---|---|---|---|

| US Policy Rate | 5.33% (peak) | 3.4% (projected) | Supportive |

| Rate Spread (IN−US) | Narrow | Widening | Supportive |

| Brent Crude | Elevated | ~$92, steep drop | Supportive |

| India CPI | 4.95% | In RBI band | Supportive |

Legend: Shift in the four dominant USD/INR drivers from 2024 to mid-2026. Every variable has moved toward rupee support. Conditions reflect realized policy rates, oil prices, and inflation.

</FinancialData>

| Horizon | Modeled USD/INR | Rupee Put Value Index |

|---|---|---|

| Spot | 95.1 | 0.96 |

| +1 mo | 94.5 | 1.14 |

| +2 mo | 93.8 | 1.40 |

| +3 mo | 93.0 | 1.82 |

| +4 mo | 92.2 | 2.40 |

| +6 mo | 91.5 | 3.16 |

Legend: Black-Scholes valuation of a rupee-strengthening path versus a 95 strike, six-month horizon, ~7.3% implied volatility. Rising index reflects increasing value of downside-dollar protection — consistent with an orderly recovery, not continued depreciation.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_eco_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 6.495 |

| 2023 | annual | 9.191 |

| 2022 | annual | 7.609 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 4.953 |

| 2023 | annual | 5.649 |

| 2022 | annual | 6.699 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 4.173 |

| 2023 | annual | 4.172 |

| 2022 | annual | 4.822 |

| Period | Frequency | Value |

|---|---|---|

| 2022 | annual | 2.521 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 71.372 |

| 2023 | annual | 70.493 |

| 2022 | annual | 71.719 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 9.989 |

| 2023 | annual | 10.305 |

| 2022 | annual | 10.255 |

…(truncated)…

MCP tool: generate_eco_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.793 |

| 2023 | annual | 2.888 |

| 2022 | annual | 2.512 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.950 |

| 2023 | annual | 4.116 |

| 2022 | annual | 8.003 |

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 4.282 |

| 2024 | annual | 4.022 |

| 2023 | annual | 3.638 |

| 2022 | annual | 3.650 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 117.973 |

| 2023 | annual | 116.919 |

| 2022 | annual | 114.695 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 82.893 |

| 2023 | annual | 82.612 |

| 2022 | annual | 83.021 |

| Period | Frequency | Value |

|---|---|---|

| 2022 | annual | 13.943 |

…(truncated)…

MCP tool: generate_treasury_report

Historical window: last 5 years (no forecast).

| Tenor | Latest | 1Y Ago | Chg 1Y | 5Y Ago | Chg 5Y |

|---|---|---|---|---|---|

| 1MO | - | - | - | - | - |

| 3MO | - | - | - | - | - |

| 6MO | - | - | - | - | - |

| 1YR | - | - | - | - | - |

| 2YR | - | - | - | - | - |

| 3YR | - | - | - | - | - |

| 5YR | - | - | - | - | - |

| 7YR | - | - | - | - | - |

| 10YR | - | - | - | - | - |

| 20YR | - | - | - | - | - |

| 30YR | - | - | - | - | - |

…(truncated)…

MCP tool: get_option_chain

| Type | Strike | Expiration | Bid | Ask | Last | IV | Vol | OI |

|---|---|---|---|---|---|---|---|---|

| CALL | 18 | 2026-06-18 | 8.0 | 11.9 | 10.16 | 1.5% | - | - |

| PUT | 18 | 2026-06-18 | - | 0.05 | - | 141.0% | - | - |

| CALL | 19 | 2026-06-18 | 8.3 | 9.7 | 9.16 | 151.7% | - | 3 |

| PUT | 19 | 2026-06-18 | - | 0.05 | - | 125.4% | - | 10 |

| CALL | 20 | 2026-06-18 | 5.8 | 10.1 | 8.02 | 1.5% | - | - |

| PUT | 20 | 2026-06-18 | - | 0.05 | - | 110.8% | - | 10 |

| CALL | 21 | 2026-06-18 | 6.3 | 7.7 | 6.96 | 116.6% | - | 1 |

| PUT | 21 | 2026-06-18 | - | 0.05 | - | 96.1% | - | - |

| CALL | 22 | 2026-06-18 | 5.3 | 6.7 | 6.08 | 100.0% | - | 2 |

| PUT | 22 | 2026-06-18 | - | 0.05 | - | 81.5% | - | 1 |

| CALL | 23 | 2026-06-18 | 4.4 | 5.6 | 4.92 | 83.4% | - | 1 |

| PUT | 23 | 2026-06-18 | - | 0.05 | - | 68.8% | - | 35 |

| CALL | 24 | 2026-06-18 | 3.4 | 4.6 | 4.02 | 67.8% | - | - |

| PUT | 24 | 2026-06-18 | - | 0.05 | - | 55.1% | - | 29 |

| CALL | 25 | 2026-06-18 | 2.4 | 3.6 | 2.98 | 52.2% | - | 36 |

| PUT | 25 | 2026-06-18 | - | 0.05 | - | 42.5% | - | 162 |

| CALL | 26 | 2026-06-18 | 1.85 | 2.4 | 1.8 | 56.1% | - | 205 |

| PUT | 26 | 2026-06-18 | - | 0.1 | - | 28.8% | - | 1825 |

| CALL | 27 | 2026-06-18 | 0.65 | 1.1 | 0.95 | 1.5% | - | 1808 |

| PUT | 27 | 2026-06-18 | - | 0.05 | - | 16.1% | - | 4808 |

| CALL | 28 | 2026-06-18 | 0.05 | 0.1 | 0.09 | 6.4% | 125 | 17391 |

| PUT | 28 | 2026-06-18 | 0.05 | 0.25 | 0.13 | 9.3% | 10 | 316 |

| CALL | 29 | 2026-06-18 | - | 0.2 | 0.03 | 16.1% | - | 1412 |

| PUT | 29 | 2026-06-18 | 0.65 | 1.35 | - | 1.5% | - | 2 |

| CALL | 30 | 2026-06-18 | - | 0.05 | 0.02 | 27.8% | - | 1998 |

| PUT | 30 | 2026-06-18 | 1.45 | 2.3 | - | 1.5% | - | 1 |

| CALL | 31 | 2026-06-18 | - | 0.05 | 0.15 | 38.6% | - | 598 |

| PUT | 31 | 2026-06-18 | 2.4 | 3.6 | - | 1.5% | - | 1 |

| CALL | 32 | 2026-06-18 | - | 0.05 | 0.03 | 48.3% | - | 105 |

| PUT | 32 | 2026-06-18 | 3.4 | 4.6 | - | 1.5% | - | - |

| CALL | 33 | 2026-06-18 | - | 0.05 | 0.03 | 58.1% | - | 266 |

| PUT | 33 | 2026-06-18 | 4.4 | 5.6 | - | 1.5% | - | - |

| CALL | 34 | 2026-06-18 | - | 0.05 | - | 66.9% | - | 2 |

| PUT | 34 | 2026-06-18 | 3.9 | 8.2 | - | 73.7% | - | - |

| CALL | 35 | 2026-06-18 | - | 0.05 | - | 74.7% | - | - |

| PUT | 35 | 2026-06-18 | 5.0 | 9.2 | - | 102.0% | - | - |

| CALL | 36 | 2026-06-18 | - | 0.05 | - | 83.4% | - | 1 |

| PUT | 36 | 2026-06-18 | 6.0 | 10.2 | - | 111.7% | - | - |

| CALL | 37 | 2026-06-18 | - | 0.05 | - | 91.2% | - | - |

| PUT | 37 | 2026-06-18 | 7.0 | 10.8 | - | 1.5% | - | - |

| CALL | 38 | 2026-06-18 | - | 0.05 | 0.05 | 98.1% | - | 79 |

| PUT | 38 | 2026-06-18 | 7.9 | 12.2 | - | 108.8% | - | - |

| CALL | 17 | 2026-07-17 | 8.8 | 13.1 | - | 1.5% | - | - |

| PUT | 17 | 2026-07-17 | - | 0.05 | - | 65.9% | - | - |

| CALL | 18 | 2026-07-17 | 7.8 | 12.1 | 10.16 | 1.5% | - | 1 |

| PUT | 18 | 2026-07-17 | - | 0.05 | - | 59.0% | - | - |

| CALL | 19 | 2026-07-17 | 6.8 | 11.1 | 9.12 | 1.5% | - | 1 |

| PUT | 19 | 2026-07-17 | - | 0.05 | - | 52.2% | - | - |

| CALL | 20 | 2026-07-17 | 5.6 | 10.1 | 8.16 | 1.5% | - | 1 |

| PUT | 20 | 2026-07-17 | - | 0.05 | - | 46.4% | - | - |

| CALL | 21 | 2026-07-17 | 4.8 | 9.1 | 7.06 | 1.5% | - | - |

| PUT | 21 | 2026-07-17 | - | 0.05 | - | 40.5% | - | - |

| CALL | 22 | 2026-07-17 | 3.8 | 8.1 | - | 1.5% | - | - |

| PUT | 22 | 2026-07-17 | - | 0.05 | - | 34.7% | - | - |

| CALL | 23 | 2026-07-17 | 3.3 | 6.9 | - | 39.5% | - | - |

| PUT | 23 | 2026-07-17 | - | 0.05 | - | 28.8% | - | - |

| CALL | 24 | 2026-07-17 | 2.0 | 6.1 | - | 24.9% | - | - |

| PUT | 24 | 2026-07-17 | - | 0.05 | - | 23.0% | - | - |

| CALL | 25 | 2026-07-17 | 1.1 | 4.3 | - | 1.5% | - | - |

| PUT | 25 | 2026-07-17 | - | 0.05 | - | 18.1% | - | - |

| CALL | 26 | 2026-07-17 | 1.7 | 2.45 | 2.13 | 16.1% | - | 5 |

| PUT | 26 | 2026-07-17 | - | 0.75 | - | 12.2% | - | - |

| CALL | 27 | 2026-07-17 | 0.8 | 1.35 | 1.08 | 9.3% | 31 | 38 |

| PUT | 27 | 2026-07-17 | - | 0.75 | - | 7.3% | - | 30 |

| CALL | 28 | 2026-07-17 | 0.1 | 0.35 | 0.24 | 5.4% | 2 | 1430 |

| PUT | 28 | 2026-07-17 | 0.1 | 0.35 | 0.27 | 7.3% | 3 | 2 |

| CALL | 29 | 2026-07-17 | - | 0.15 | 0.05 | 6.4% | - | 297 |

| PUT | 29 | 2026-07-17 | 0.45 | 1.55 | - | 9.3% | - | 2 |

| CALL | 30 | 2026-07-17 | - | 0.15 | 0.04 | 11.2% | 1 | 3 |

| PUT | 30 | 2026-07-17 | 1.55 | 2.6 | - | 20.0% | - | 1 |

| CALL | 31 | 2026-07-17 | - | 0.1 | 0.03 | 15.1% | 1 | 5 |

| PUT | 31 | 2026-07-17 | 2.75 | 3.7 | - | 34.7% | - | - |

| CALL | 32 | 2026-07-17 | - | 0.05 | 0.02 | 20.0% | - | 3 |

| PUT | 32 | 2026-07-17 | 2.8 | 5.4 | - | 33.7% | - | - |

| CALL | 33 | 2026-07-17 | - | 0.05 | 0.03 | 23.9% | - | 2 |

| PUT | 33 | 2026-07-17 | 3.6 | 7.2 | - | 55.1% | - | - |

| CALL | 34 | 2026-07-17 | - | 0.05 | - | 26.9% | - | - |

| PUT | 34 | 2026-07-17 | 3.9 | 8.2 | - | 41.5% | - | - |

| CALL | 35 | 2026-07-17 | - | 0.05 | - | 30.8% | - | - |

| PUT | 35 | 2026-07-17 | 4.9 | 9.2 | - | 46.4% | - | - |

| CALL | 36 | 2026-07-17 | - | 0.05 | - | 33.7% | - | - |

| PUT | 36 | 2026-07-17 | 6.6 | 9.6 | - | 55.1% | - | - |

| CALL | 37 | 2026-07-17 | - | 0.05 | 0.1 | 37.6% | - | 1 |

| PUT | 37 | 2026-07-17 | 6.9 | 11.2 | - | 56.1% | - | - |

| CALL | 17 | 2026-09-18 | 10.0 | 12.3 | 11.14 | 47.3% | - | 1 |

| PUT | 17 | 2026-09-18 | - | 0.05 | - | 39.5% | - | - |

| CALL | 18 | 2026-09-18 | 9.2 | 11.3 | - | 53.2% | - | - |

| PUT | 18 | 2026-09-18 | - | 0.05 | - | 35.6% | - | - |

| CALL | 19 | 2026-09-18 | 8.2 | 10.3 | - | 46.4% | - | - |

| PUT | 19 | 2026-09-18 | - | 0.05 | - | 31.7% | - | - |

| CALL | 20 | 2026-09-18 | 5.9 | 9.3 | 8.16 | 1.5% | - | 1 |

| PUT | 20 | 2026-09-18 | - | 0.05 | - | 27.8% | - | - |

| CALL | 21 | 2026-09-18 | 4.9 | 8.3 | - | 1.5% | - | - |

| PUT | 21 | 2026-09-18 | - | 0.05 | - | 23.9% | - | - |

| CALL | 22 | 2026-09-18 | 5.0 | 7.4 | 6.0 | 25.9% | - | 1 |

| PUT | 22 | 2026-09-18 | - | 0.05 | - | 21.0% | - | 14 |

| CALL | 23 | 2026-09-18 | 3.2 | 6.4 | - | 1.5% | - | - |

| PUT | 23 | 2026-09-18 | - | 0.1 | - | 18.1% | - | 3 |

| CALL | 24 | 2026-09-18 | 2.3 | 5.4 | 4.02 | 1.5% | - | 1 |

| PUT | 24 | 2026-09-18 | - | 0.2 | - | 14.2% | - | 45 |

| CALL | 25 | 2026-09-18 | 1.6 | 4.4 | 2.85 | 1.5% | - | 4 |

| PUT | 25 | 2026-09-18 | - | 0.05 | - | 11.2% | - | 1158 |

| CALL | 26 | 2026-09-18 | 1.65 | 2.6 | 2.2 | 1.5% | - | 18 |

| PUT | 26 | 2026-09-18 | - | 0.2 | - | 8.3% | - | 7650 |

| CALL | 27 | 2026-09-18 | 1.05 | 1.6 | 1.28 | 9.3% | 1 | 911 |

| PUT | 27 | 2026-09-18 | - | 0.2 | 0.1 | 4.4% | 210 | 12157 |

| CALL | 28 | 2026-09-18 | 0.45 | 0.55 | 0.53 | 6.4% | 20 | 4033 |

| PUT | 28 | 2026-09-18 | 0.2 | 0.4 | - | 7.3% | - | 262 |

| CALL | 29 | 2026-09-18 | 0.15 | 0.25 | 0.17 | 8.3% | 2407 | 41380 |

| PUT | 29 | 2026-09-18 | 0.7 | 1.4 | - | 10.3% | - | 36 |

| CALL | 30 | 2026-09-18 | 0.05 | 0.15 | 0.11 | 10.3% | - | 853 |

| PUT | 30 | 2026-09-18 | 1.65 | 2.2 | - | 12.2% | - | 1 |

| CALL | 31 | 2026-09-18 | - | 2.55 | 0.05 | 9.3% | - | 25 |

| PUT | 31 | 2026-09-18 | 0.95 | 4.4 | - | 1.5% | - | - |

| CALL | 32 | 2026-09-18 | - | 0.15 | 0.03 | 11.2% | - | 306 |

| PUT | 32 | 2026-09-18 | 1.95 | 5.4 | - | 1.5% | - | 44 |

| CALL | 33 | 2026-09-18 | - | 0.1 | 0.05 | 13.2% | - | 518 |

| PUT | 33 | 2026-09-18 | 3.0 | 6.4 | - | 1.5% | - | - |

| CALL | 34 | 2026-09-18 | - | 0.05 | - | 16.1% | - | - |

| PUT | 34 | 2026-09-18 | 4.0 | 8.1 | - | 31.7% | - | - |

| CALL | 35 | 2026-09-18 | - | 0.05 | - | 18.1% | - | - |

| PUT | 35 | 2026-09-18 | 4.9 | 9.1 | - | 33.7% | - | - |

| CALL | 36 | 2026-09-18 | - | 0.05 | - | 20.0% | - | - |

| PUT | 36 | 2026-09-18 | 5.9 | 10.2 | - | 38.6% | - | - |

| CALL | 37 | 2026-09-18 | - | 0.05 | - | 22.0% | - | - |

| PUT | 37 | 2026-09-18 | 6.9 | 11.2 | - | 42.5% | - | - |

| CALL | 17 | 2026-12-18 | 8.9 | 13.2 | - | 1.5% | - | - |

| PUT | 17 | 2026-12-18 | - | 0.05 | - | 28.8% | - | - |

| CALL | 18 | 2026-12-18 | 7.9 | 12.2 | - | 1.5% | - | - |

| PUT | 18 | 2026-12-18 | - | 0.05 | - | 25.9% | - | - |

| CALL | 19 | 2026-12-18 | 7.0 | 11.2 | - | 1.5% | - | - |

| PUT | 19 | 2026-1 |

…(truncated)…

MCP tool: price_option_path

{"option_path": [0.9596681467325503, 1.136933611466283, 1.4043162187554046, 1.8176074692189204, 2.3999040862657353, 3.15724014956254], "volatility_used": 0.07343485731462454, "symbol": "USDINR"}

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.