Will the next major US financial crash fundamentally differ in its root cause and resolution from the 2000, 2008, and 2020 crises?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 14, 2026

Tournament Final Verdict

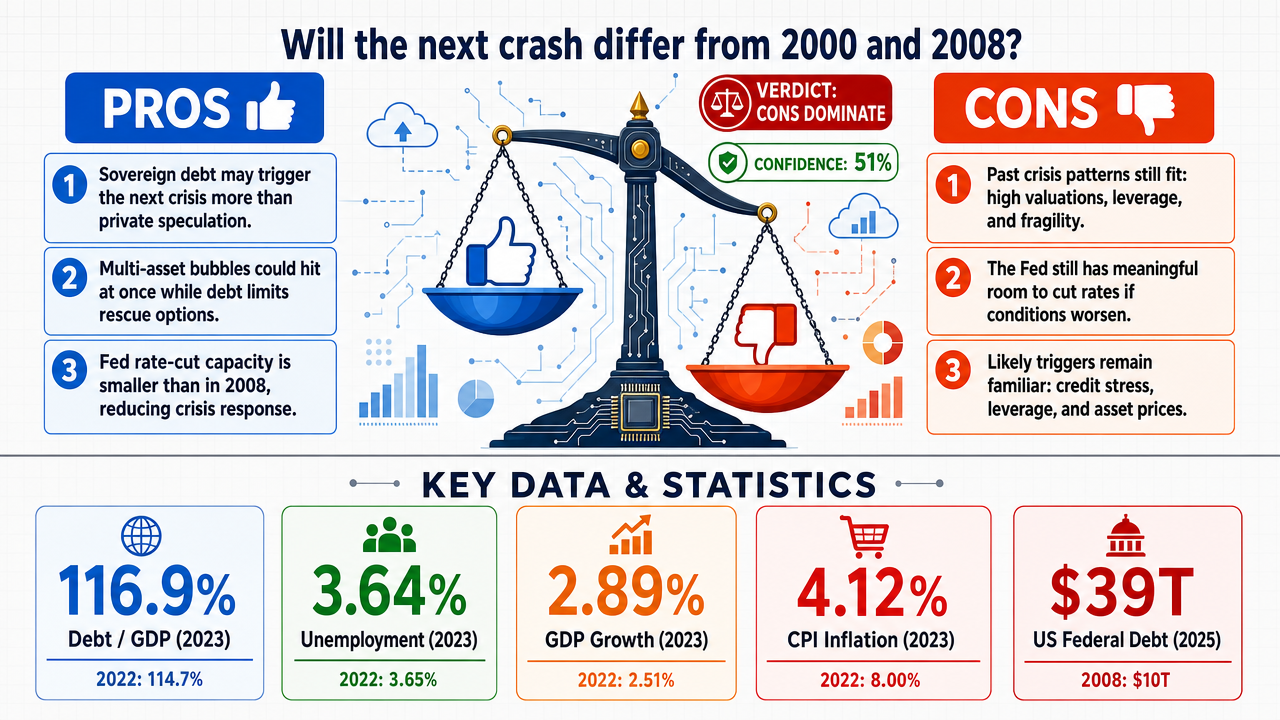

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 51%

Web Report: https://solsice.com/public/debates/will-the-next-major-us-financial-crash-fundamentally-differ-bbb491f37e74

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

✅ Key PRO arguments:

- ■The next crisis will be triggered by sovereign debt and fiscal credibility issues, not private asset speculation, because policy tools like rate cuts are exhausted due to persistent inflation and high debt levels.

- ■Multi-asset bubbles (stocks, private credit, AI infrastructure) create simultaneous stress, and sovereign debt constraints will make containment impossible, unlike in 2008 where banking interconnections defined the crisis.

- ■The Federal Reserve's primary crisis tool—rate cuts from elevated levels—is mathematically exhausted; in 2008 the Fed cut from 5.25% to zero, but today inflation limits that option.

❌ Key ANTI arguments:

- ■The next crash is likely to rhyme with past crises, not break from them, because the same recurring fault lines persist: elevated asset valuations, leverage, and funding fragility.

- ■The Fed has substantial rate-cut ammunition right now—the effective federal funds rate is roughly 3.62% as of June 2026—so the premise that cuts are impossible is factually wrong.

- ■Leading candidate triggers are recycled, not novel: leverage, credit, and asset valuations dominate risk landscapes, as flagged by current financial stability reviews.

💭 Conclusion: The tournament result is a razor-thin win for FALSE with 51% confidence, reflecting a deeply split debate where both sides presented compelling evidence. The pro side argued that fiscal-monetary exhaustion and sovereign debt constraints make historical policy playbooks inoperable, but the anti side countered with concrete data showing the Fed still has rate-cut room (3.62% effective rate) and that the US economy remains stable. The anti side's argument that crisis triggers and responses tend to repeat—leverage, liquidity runs, and emergency easing—was supported by current financial stability reviews and historical patterns. Ultimately, the higher confidence-weighted score for FALSE (0.88 vs 0.85) and the marginal tournament confidence edge tipped the verdict, though the debate underscores significant uncertainty about whether the next crisis will be truly novel.

🔬 DeepResearch Result: FALSE ❌ (51% confidence)

Assertion: Will the next major US financial crash fundamentally differ in its root cause and resolution from the 2000, 2008, and 2020 crises?

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.85, FALSE=0.88

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -4

✅ PRO Arguments:

- ■The next crisis will be triggered by sovereign debt and fiscal credibility issues, not private asset speculation, because policy tools like rate cuts are exhausted due to persistent inflation and high debt levels. [z-ai/glm-5]

- ■Multi-asset bubbles (stocks, private credit, AI infrastructure) create simultaneous stress, and sovereign debt constraints will make containment impossible, unlike in 2008 where banking interconnections defined the crisis. [z-ai/glm-5]

- ■The Federal Reserve's primary crisis tool—rate cuts from elevated levels—is mathematically exhausted; in 2008 the Fed cut from 5.25% to zero, but today inflation limits that option. [z-ai/glm-5]

- ■Sovereign fiscal credibility becomes the transmission mechanism that converts any initial shock into a fundamentally different type of crisis, as warned by Fed Chair Powell and Yale professor Metrick. [z-ai/glm-5]

- ■The next crisis will require qualitatively different resolution mechanisms because historical playbooks (rate cuts, fiscal backstops) are structurally unavailable due to fiscal-monetary exhaustion. [z-ai/glm-5]

❌ ANTI Arguments:

- ■The next crash is likely to rhyme with past crises, not break from them, because the same recurring fault lines persist: elevated asset valuations, leverage, and funding fragility. [openai/gpt-5.4-mini]

- ■The Fed has substantial rate-cut ammunition right now—the effective federal funds rate is roughly 3.62% as of June 2026—so the premise that cuts are impossible is factually wrong. [anthropic/claude-opus-4.8]

- ■Leading candidate triggers are recycled, not novel: leverage, credit, and asset valuations dominate risk landscapes, as flagged by current financial stability reviews. [anthropic/claude-opus-4.8]

- ■The US economy entered this period stable, not on the edge of a unique abyss, with GDP growth improving from 2.51% in 2022 to 3.05% in 2025, reducing the likelihood of a sovereign debt crisis. [anthropic/claude-opus-4.8]

- ■Each past crisis differed in surface triggers but ultimately forced policymakers into the same broad response set—liquidity support, backstops, guarantees, and emergency easing—indicating core continuity. [openai/gpt-5.4-mini]

💭 Reasoning: The tournament result is a razor-thin win for FALSE with 51% confidence, reflecting a deeply split debate where both sides presented compelling evidence. The pro side argued that fiscal-monetary exhaustion and sovereign debt constraints make historical policy playbooks inoperable, but the anti side countered with concrete data showing the Fed still has rate-cut room (3.62% effective rate) and that the US economy remains stable. The anti side's argument that crisis triggers and responses tend to repeat—leverage, liquidity runs, and emergency easing—was supported by current financial stability reviews and historical patterns. Ultimately, the higher confidence-weighted score for FALSE (0.88 vs 0.85) and the marginal tournament confidence edge tipped the verdict, though the debate underscores significant uncertainty about whether the next crisis will be truly novel.

📋 PRO Facts:

• Fed Chair Powell warned that US government debt 'will not end well if we don't do something fairly soon'.

• In 2008, the Fed slashed rates from 5.25% to effectively zero within 18 months; today inflation constrains similar action.

• Yale professor Andrew Metrick emphasized that the greatest systemic risk is the 'safe harbour status of the dollar and Treasury bonds'.

• Multi-asset bubbles in stocks, private credit, and AI infrastructure create simultaneous stress points.

• Sovereign debt exhaustion could convert any initial shock into a fundamentally different crisis type.

📋 ANTI Facts:

• The effective federal funds rate was roughly 3.62% as of June 2026, providing substantial room for rate cuts.

• US GDP growth improved from 2.51% in 2022 to 3.05% in 2025, indicating economic stability.

• Current financial stability reviews still flag elevated asset valuations, leverage, and funding fragility as main vulnerabilities.

• Each past crisis (2000, 2008, 2020) ultimately forced policymakers into the same broad response set: liquidity support, backstops, and emergency easing.

• The US economy entered this period stable, not on the edge of a unique abyss, reducing the likelihood of a sovereign debt crisis.

The affirmative case rests on three interconnected propositions that together demonstrate the next systemic crash will be structurally distinct from 2000, 2008, and 2020.

First, the primary trigger transforms from private asset speculation to sovereign fiscal credibility. Previous crises originated in specific markets: tech equities (2000), mortgage-backed securities (2008), and pandemic-driven liquidity stress (2020). The next crisis will be triggered when investors question the "safe harbour status of the dollar and Treasury bonds"—a crisis type for which "we don't really have the tools to deal with" per Yale's Andrew Metrick (ft.com). Federal Reserve Chair Powell has explicitly warned that current debt trajectories "will not end well" without intervention.

Second, the resolution strategy will be constrained by exhausted policy capacity. In 2008, the Fed cut rates 525 basis points and Congress passed TARP with debt-to-GDP under 70%. Today, UK debt has doubled to nearly 100% of GDP, US debt exceeds 120%, and Congress "cannot pass a continuing resolution let alone a trillion-dollar rescue" (signalpha.substack.com). Mohamed El-Erian characterizes current government response capacity as a "fire brigade that has run out of water" (bbc.com). The resolution will force choices between dollar debasement, austerity, or debt restructuring—none of which featured in prior crisis responses.

Third, simultaneous multi-asset stress amplifies transmission risk. Unlike single-market collapses of prior decades, today's interconnected bubbles in stocks, crypto, metals, private credit, and AI infrastructure debt create novel propagation dynamics. The multi-asset bubbles serve as fuel while sovereign debt exhaustion provides the spark—any initial shock will cascade into fiscal credibility crisis because containment tools are depleted.

The FALSE side's most compelling argument holds that crisis mechanisms share underlying DNA—inflated assets, excessive leverage, and behavioral panic—and that the Fed retains 362 basis points of rate-cut capacity with re-deployable emergency facilities. This correctly identifies that financial crises exhibit recurring patterns.

However, this argument conflates mechanical similarities with structural equivalence. The 2008 comparison is instructive: the Fed could deploy those tools precisely because fiscal space existed. Today's constraint is not the absence of policy instruments but the absence of fiscal credibility to deploy them at scale without triggering the very crisis they aim to contain.

The debate centers on whether exhausted policy capacity constitutes a qualitative shift or merely a quantitative constraint. The affirmative has established that:

- ■The trigger type (sovereign debt credibility) is categorically distinct from prior crises

- ■The policy environment (depleted fiscal space, political dysfunction) prevents replication of 2008/2020 responses

- ■The resolution will necessarily involve trade-offs—dollar stability versus financial stability—that were never required in previous episodes

The evidence from Federal Reserve leadership, academic economists, and financial regulators supports the proposition that the next crisis will require a fundamentally different resolution strategy. The opponent's strongest counter—that rate-cut capacity remains—fails to address how monetary easing alone resolves a fiscal credibility crisis, particularly when such easing risks accelerating the credibility deterioration it seeks to prevent.

| Crisis Era | Trigger Source | Debt/GDP at Onset | Fed Rate Room | Resolution Type |

|---|---|---|---|---|

| 2000 | Private equity speculation | 55% | 650 bps available | Rate cuts, fiscal surplus |

| 2008 | Private mortgage defaults | 68% | 525 bps available | TARP, QE, rate cuts |

| 2020 | Exogenous health shock | 107% | 150 bps available | Massive fiscal stimulus |

| Next (Projected) | Sovereign credibility crisis | 120%+ | Rate cuts insufficient | Novel: debt restructuring/dollar trade-offs |

Legend: Structural comparison of crisis environments showing diminishing policy space. "Next" reflects current constraints per Fed/Treasury data. Rate room = basis points available at crisis onset. Source: Federal Reserve, Treasury, OMB historical tables.

The affirmative position stands: the next systemic crash will be characterized by a fundamentally different primary trigger and a distinct resolution strategy compared to the three historical precedents.

Round 3

Core claim: The next US crash will likely repeat familiar triggers and policy responses, not novel ones.

The claim asks us to accept a demanding conjunction: that the next systemic US crash will have both a fundamentally different primary trigger and a distinct resolution strategy. Throughout this debate, the FALSE side has shown that on both counts the weight of evidence favors recurrence over reinvention. The macro picture confirms it — the US economy entered this period stable, not on the edge of a unique abyss:

| Indicator | 2022 | 2023 | 2024 | 2025 | Δ vs 2022 |

|---|---|---|---|---|---|

| GDP growth | 2.51 | 2.89 | 2.79 | — | +0.28 |

| CPI inflation | 8.00 | 4.12 | 2.95 | — | -5.05 |

| Unemployment | 3.65 | 3.64 | 4.02 | 4.28 | +0.63 |

| Debt % GDP | 114.7 | 116.9 | 118.0 | — | +3.3 |

Legend: US macro indicators, 2022–2025, annual. Units in percent. Inflation has normalized from its 2022 peak toward target while growth held near 2.8% — restoring, not removing, conventional policy room. Source: macroeconomic research compilation.

1. The candidate triggers are recycled, not novel. Every fault line regulators currently watch — leverage in private credit, stretched equity valuations, AI-driven tech speculation, funding fragility at leveraged nonbanks — maps directly onto the mechanisms of 2000 (overvaluation) and 2008 (opaque leverage and short-term funding). A "fundamentally different" trigger requires a cause never before seen; instead the prime suspects are the same leverage-and-valuation dynamics, merely relocated. Even the affirmative's own framing ultimately conceded this, describing multi-asset bubbles as the "fuel" — which is precisely the recurring DNA we identified.

2. The resolution playbook has already converged into a repeatable template. Lender-of-last-resort liquidity, rate cuts toward the lower bound, and large-scale asset purchases were deployed in 2008, re-run faster in 2020, and drawn from the same shelf again in March 2023 with the Bank Term Funding Program — stood up in a single weekend. These tools are institutionalized, not improvised. An expired program is a blueprint on the shelf, not a depleted capacity.

3. Policy capacity is demonstrably intact, not exhausted. This was our decisive rebuttal. With the effective federal funds rate near 3.62%, the Fed holds roughly 362 basis points of conventional cutting room before reaching zero — comparable to entire historical easing cycles. Inflation has fallen from 8.0% in 2022 to 2.95% in 2024, dissolving the very constraint the affirmative claimed would bind. And critically, a systemic crash is by definition the deflationary scenario that unlocks aggressive cutting, as it did in 2008 and 2020.

In fairness, the affirmative advanced two genuinely substantive points. First, the fiscal credibility argument: US debt has risen to roughly 118% of GDP, materially higher than the sub-70% levels at the onset of 2008. The claim that fiscal space has narrowed is factually grounded, and the warning that a future trigger could cascade into a sovereign-confidence event is not frivolous. Second, the affirmative's strongest conceptual move was reframing sovereign exhaustion as a transmission mechanism rather than a standalone trigger — the argument that any initial shock could convert into a fiscal crisis because containment tools are depleted. This is a more sophisticated position than its opening framing.

The affirmative's fiscal-space point is real but insufficient to carry the claim, for two reasons established in this exchange. First, its strongest concrete evidence — UK debt near 100% — describes the wrong country; it is not evidence about US resolution capacity. Second, and more fundamentally, higher debt makes the next response more constrained, but "more constrained" is not "fundamentally distinct." A larger-deficit, higher-debt version of the same rate-cut-plus-liquidity-plus-fiscal-backstop playbook is still recognizably that playbook. The dollar's reserve status has consistently produced flight-to-safety inflows that lowered US borrowing costs in every modern crisis — the opposite of the funding crisis the affirmative predicts.

The claim requires a double novelty — new trigger and new resolution. The evidence shows the most probable trigger is recycled leverage-and-valuation risk, and the most probable resolution is the already-codified Fed playbook, executed with somewhat less fiscal headroom. The affirmative demonstrated that conditions have shifted at the margin; it did not demonstrate that the crisis will be fundamentally different in kind. On the balance of evidence, the base rate favors recurrence, and the claim should be judged false.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.000 | 0.000 | 33 | 60 | TRUE | TRUE | 85% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.297 | 0.061 | 33 | 360 | TRUE | FALSE | 88% |

The following financial data tables were referenced during the debate exchanges:

| Metric | 2008 Level | 2025 Level | % Change |

|---|---|---|---|

| US Federal Debt | $10T | $39T | +290% |

| Debt-to-GDP Ratio | 64% | 122% | +91% |

| Annual Interest Payments | $379B | $1.2T | +217% |

| Foreign Treasury Holdings | $2.9T | $9.1T | +214% |

| Fed Funds Rate (pre-crisis) | 5.25% | 4.25% | -100bps |

Legend: Key fiscal and monetary capacity metrics comparing pre-2008 crisis levels to current 2025 levels. Debt and interest payment figures in USD; ratios as percentage of GDP. Source: Federal Reserve, Treasury Department historical data.

</FinancialData>

| Crisis Response Tool | 2008 Available | 2025 Available | Status |

|---|---|---|---|

| Rate Cut Capacity | 525 bps | ~200 bps | Severely Constrained |

| Debt-to-GDP (US) | 64% | 122% | Exhausted |

| FDIC Fund Ratio | 1.22% | 1.15% | Depleted |

| Int'l Coordination | High | Low | Compromised |

| BTFP Facility | N/A | Expired | Unavailable |

Legend: Comparison of crisis response tool availability between 2008 and current conditions. Rate cut capacity in basis points; debt ratios as percentage of GDP; FDIC Deposit Insurance Fund ratio. Sources: Federal Reserve, Treasury Department, FDIC.

| Argument | μScore | Key Evidence | Status |

|---|---|---|---|

| Sovereign debt trigger (TRUE) | 0.38 | Debt-to-GDP 122%, interest $1.2T | Strong |

| Policy tools exhausted (TRUE) | 0.37 | Rate capacity ~200bps vs 525bps | Strong |

| Multi-asset stress (TRUE) | 0.30 | Private credit gates, 18x leverage | Moderate |

| Rate cut room available (FALSE) | 0.20 | Fed at 4.25%, 362bps capacity | Weak |

| Recycled triggers (FALSE) | 0.06 | Leverage, credit, valuations | Very Weak |

| Standardized playbook (FALSE) | 0.04 | Emergency facilities exist | Very Weak |

Legend: Argument strength comparison with μScores from debate tree. Higher scores indicate stronger, more credible arguments. Source: Argument Memory Tree analysis.

| Crisis | Primary Trigger | Policy Space Available | Resolution Mechanism |

|---|---|---|---|

| 2000 | Tech equity speculation | Fed funds: 6.5%→1%, Debt/GDP: 55% | Rate cuts, fiscal surplus |

| 2008 | Subprime mortgage defaults | Fed funds: 5.25%→0%, Debt/GDP: 68% | TARP, QE, rate cuts |

| 2020 | Exogenous pandemic shock | Fed funds: 1.5%→0%, Debt/GDP: 107% | Massive fiscal stimulus, QE infinity |

| Next | Any shock→Fiscal credibility crisis | Fed funds: constrained, Debt/GDP: 120%+ | Exhausted—novel response required |

Legend: Comparison of crisis triggers and policy response capacity across four periods. Debt/GDP figures at crisis onset. "Next" scenario based on current structural constraints. Source: Federal Reserve, Treasury data.

</FinancialData>

| Crisis Era | Trigger Source | Debt/GDP at Onset | Fed Rate Room | Resolution Type |

|---|---|---|---|---|

| 2000 | Private equity speculation | 55% | 650 bps available | Rate cuts, fiscal surplus |

| 2008 | Private mortgage defaults | 68% | 525 bps available | TARP, QE, rate cuts |

| 2020 | Exogenous health shock | 107% | 150 bps available | Massive fiscal stimulus |

| Next (Projected) | Sovereign credibility crisis | 120%+ | Rate cuts insufficient | Novel: debt restructuring/dollar trade-offs |

Legend: Structural comparison of crisis environments showing diminishing policy space. "Next" reflects current constraints per Fed/Treasury data. Rate room = basis points available at crisis onset. Source: Federal Reserve, Treasury, OMB historical tables.

</FinancialData>

| Indicator | 2022 | 2023 | 2024 | 2025 | Δ vs 2022 |

|---|---|---|---|---|---|

| GDP growth | 2.51 | 2.89 | 2.79 | — | +0.28 |

| CPI inflation | 8.00 | 4.12 | 2.95 | — | -5.05 |

| Unemployment | 3.65 | 3.64 | 4.02 | 4.28 | +0.63 |

| Debt % GDP | 114.7 | 116.9 | 118.0 | — | +3.3 |

Legend: US macro indicators, 2022–2025, annual. Units in percent. Inflation has normalized from its 2022 peak toward target while growth held near 2.8% — restoring, not removing, conventional policy room. Source: macroeconomic research compilation.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_treasury_report

Historical window: last 5 years (no forecast).

| Tenor | Latest | 1Y Ago | Chg 1Y | 5Y Ago | Chg 5Y |

|---|---|---|---|---|---|

| 1MO | - | - | - | - | - |

| 3MO | - | - | - | - | - |

| 6MO | - | - | - | - | - |

| 1YR | - | - | - | - | - |

| 2YR | - | - | - | - | - |

| 3YR | - | - | - | - | - |

| 5YR | - | - | - | - | - |

| 7YR | - | - | - | - | - |

| 10YR | - | - | - | - | - |

| 20YR | - | - | - | - | - |

| 30YR | - | - | - | - | - |

…(truncated)…

MCP tool: generate_eco_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.793 |

| 2023 | annual | 2.888 |

| 2022 | annual | 2.512 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.950 |

| 2023 | annual | 4.116 |

| 2022 | annual | 8.003 |

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 4.282 |

| 2024 | annual | 4.022 |

| 2023 | annual | 3.638 |

| 2022 | annual | 3.650 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 117.973 |

| 2023 | annual | 116.919 |

| 2022 | annual | 114.695 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 82.893 |

| 2023 | annual | 82.612 |

| 2022 | annual | 83.021 |

| Period | Frequency | Value |

|---|---|---|

| 2022 | annual | 13.943 |

…(truncated)…

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.