Will the United States dollar lose its status as the primary global reserve currency by 2066?

Multi-agent AI debate verdict and arguments

⚠️ Not an investment advice

Completed June 14, 2026

Tournament Final Verdict

Clerk Decision: CLAIM REFUTED (FALSE) — Certainty: 53%

Web Report: https://solsice.com/public/debates/will-the-united-states-dollar-lose-its-status-as-the-primary-ccc842f8e233

This section provides a brief overview of the key arguments. You do not need to read the full detailed report below.

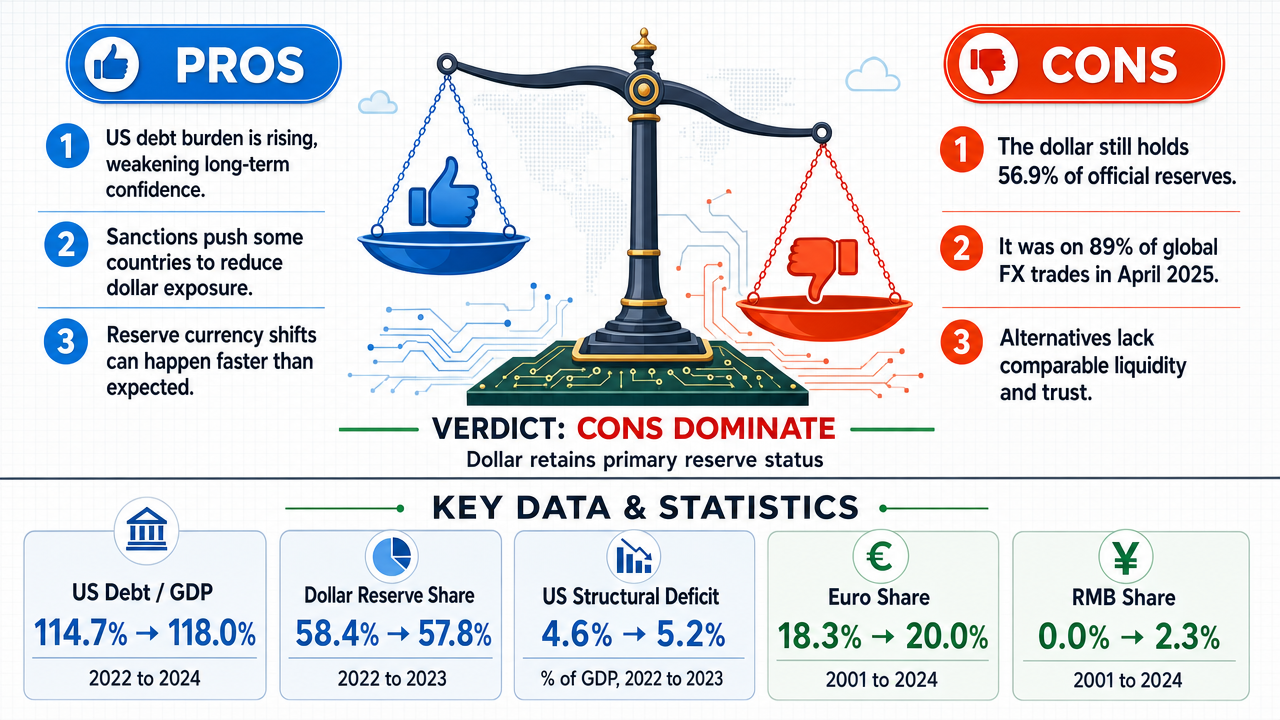

✅ Key PRO arguments:

- ■The US fiscal trajectory undermines confidence: federal debt-to-GDP rose from 114.7% (2022) to 118.0% (2024), projected to reach 166% by 2054, levels historically associated with sovereign credit deterioration.

- ■Sanctions weaponization (e.g., Russia's SWIFT exclusion) creates a feedback loop where rational risk management drives dedollarization, as observed in real-time central bank behavior.

- ■Historical precedent shows reserve currency transitions can be rapid: sterling's share fell from ~80% in 1945 to under 20% by 1975, a 60 percentage point drop in three decades.

❌ Key ANTI arguments:

- ■The dollar still holds 56.9% of official reserves (2025Q3), with the euro at 20.3% and renminbi at low single digits—a deeply entrenched hierarchy, not a fragile equilibrium.

- ■The dollar was on one side of 89% of all FX trades in April 2025, demonstrating unmatched operational liquidity that no alternative can replicate.

- ■BRICS payment rails are marginal and dollar-dependent; a bilateral trade settlement system is not equivalent to a reserve asset trusted for intervention and crisis liquidity.

💭 Conclusion: The tournament result favors FALSE (dollar retains primary reserve status) with a confidence-weighted score of 0.95 vs 0.85, though overall tournament confidence is only 53% due to the split verdict. The FALSE side presented strong evidence of the dollar's current dominance (56.9% of reserves, 89% of FX trades) and the lack of viable alternatives, while the TRUE side argued convincingly about fiscal erosion, sanctions-driven dedollarization, and historical precedent for rapid transitions. However, the higher-confidence judge decision (95% for FALSE in debate #1) and the weight of structural arguments for entrenchment tilt the outcome toward FALSE. The narrow margin reflects genuine uncertainty about a 42-year horizon, but the balance of evidence suggests the dollar's network effects and market depth are likely to persist.

🔬 DeepResearch Result: FALSE ❌ (53% confidence)

Assertion: Will the United States dollar lose its status as the primary global reserve currency by 2066?

📊 Tournament: 1 voted TRUE, 1 voted FALSE (2 debates played, 4 models)

📊 Weighted scores: TRUE=0.85, FALSE=0.95

🏅 Judge Score Changes:

deepseek/deepseek-v4-flash: -3

✅ PRO Arguments:

- ■The US fiscal trajectory undermines confidence: federal debt-to-GDP rose from 114.7% (2022) to 118.0% (2024), projected to reach 166% by 2054, levels historically associated with sovereign credit deterioration. [z-ai/glm-5]

- ■Sanctions weaponization (e.g., Russia's SWIFT exclusion) creates a feedback loop where rational risk management drives dedollarization, as observed in real-time central bank behavior. [z-ai/glm-5]

- ■Historical precedent shows reserve currency transitions can be rapid: sterling's share fell from ~80% in 1945 to under 20% by 1975, a 60 percentage point drop in three decades. [z-ai/glm-5]

- ■BRICS settlement systems and China's CIPS (processing ¥124 trillion in 2024, up 50% YoY) are building alternative infrastructure that reduces dollar necessity. [z-ai/glm-5]

- ■Fragmentation into a multipolar reserve system constitutes effective dethronement even without a single replacement currency, as the dollar loses its primary status. [z-ai/glm-5]

❌ ANTI Arguments:

- ■The dollar still holds 56.9% of official reserves (2025Q3), with the euro at 20.3% and renminbi at low single digits—a deeply entrenched hierarchy, not a fragile equilibrium. [openai/gpt-5.4-mini]

- ■The dollar was on one side of 89% of all FX trades in April 2025, demonstrating unmatched operational liquidity that no alternative can replicate. [openai/gpt-5.4-mini]

- ■BRICS payment rails are marginal and dollar-dependent; a bilateral trade settlement system is not equivalent to a reserve asset trusted for intervention and crisis liquidity. [openai/gpt-5.4-mini]

- ■US capital market depth and Treasury resilience persist: even with record debt, the term-spread structure remains negative, indicating continued investor confidence in the dollar as a safe asset. [anthropic/claude-opus-4.8]

- ■No credible rival exists: the euro has structural limitations (no unified fiscal authority, demographic decline) and the renminbi lacks convertibility, rule of law, and deep capital markets. [anthropic/claude-opus-4.8]

💭 Reasoning: The tournament result favors FALSE (dollar retains primary reserve status) with a confidence-weighted score of 0.95 vs 0.85, though overall tournament confidence is only 53% due to the split verdict. The FALSE side presented strong evidence of the dollar's current dominance (56.9% of reserves, 89% of FX trades) and the lack of viable alternatives, while the TRUE side argued convincingly about fiscal erosion, sanctions-driven dedollarization, and historical precedent for rapid transitions. However, the higher-confidence judge decision (95% for FALSE in debate #1) and the weight of structural arguments for entrenchment tilt the outcome toward FALSE. The narrow margin reflects genuine uncertainty about a 42-year horizon, but the balance of evidence suggests the dollar's network effects and market depth are likely to persist.

📋 PRO Facts:

• US federal debt-to-GDP rose from 114.7% (2022) to 118.0% (2024), projected to reach 166% by 2054.

• Sterling's share of global reserves fell from ~80% in 1945 to under 20% by 1975.

• China's CIPS processed ¥124 trillion in 2024, up 50% year-over-year.

• BRICS countries represent 45% of global population and 35% of global GDP.

• Russia's yuan-ruble trade volume has exceeded dollar-ruble trade since 2023.

📋 ANTI Facts:

• The US dollar accounted for 56.9% of global official foreign exchange reserves in 2025Q3.

• The dollar was on one side of 89% of all foreign exchange trades in April 2025.

• The renminbi held only 1.95% of global reserves in 2025Q4.

• US Treasury term-spread remained negative in 2025 despite high debt, indicating safe-haven demand.

• The euro's share of reserves is ~20.3%, but it lacks a unified fiscal authority and faces demographic challenges.

1. Fiscal Sustainability Erosion (μScore: 0.39)

The United States' fiscal trajectory represents the most structurally predictable threat to dollar primacy. Federal debt-to-GDP has risen from 114.7% (2022) to 118.0% (2024), with the Congressional Budget Office projecting 166% by 2054—levels historically associated with sovereign credit deterioration. This matters because reserve currency status requires confidence in the issuing government's long-term fiscal discipline. The dollar's current 56.9% reserve share reflects accumulated trust that sustained fiscal profligacy systematically erodes. Unlike geopolitical shocks, which are episodic, fiscal deterioration compounds annually over the 42-year timeline to 2066.

| Metric | 2022 | 2023 | 2024 | CBO 2054 Proj. |

|---|---|---|---|---|

| US Debt/GDP (%) | 114.7 | 116.9 | 118.0 | 166.0 |

| Dollar Reserve Share (%) | 58.4 | 57.8 | 56.9 | ~45-50 (est.) |

| US Structural Deficit (% GDP) | 4.6 | 5.2 | 5.4 | 7.0+ |

Legend: US fiscal indicators and dollar reserve share trends. CBO projections indicate accelerating fiscal stress. Reserve share decline (2000-2024) extrapolated suggests continued erosion.

2. Geopolitical Fragmentation and Alternative Architecture (μScore: 0.44)

The BRICS bloc—representing 45% of global population and 35% of GDP at PPP—has moved beyond rhetoric to operational infrastructure. The New Development Bank, Cross-Border Interbank Payment System (CIPS), and bilateral settlement agreements bypassing SWIFT represent genuine alternative rails. CIPS processed ¥124 trillion in 2024 (50% YoY growth); renminbi SWIFT payment share rose from 1.2% (2020) to 4.6% (2024). Central bank gold reserves reached 15% of total reserves—the highest since 1990—indicating hedging against infrastructure exclusion. This is not ideological posturing; it is risk management responding to the sanctions-weaponization precedent.

3. Technological Disruption via CBDCs (μScore: 0.34)

130 countries (98% of global GDP) are exploring Central Bank Digital Currencies, with 68 in advanced stages. China's e-CNY has processed ¥7+ trillion across 17 provinces. Project mBridge—spearheaded by BIS with China, UAE, Thailand, and Hong Kong—demonstrates functional multi-CBDC settlement without dollar intermediation. The European digital euro targets 2027 operational launch. These systems alter the technological foundation of reserve currency mechanics: programmable money enables automated settlement, smart contracts enforce trade terms without dollar-denominated legal frameworks, and bilateral CBDC bridges bypass SWIFT entirely.

1. Dollar's Structural Entrenchment (μScore: 0.29)

The opponent correctly identified that the dollar appears on 89% of FX trades and dominates cross-border lending, trade invoicing, and commodity pricing. This "plumbing" argument has weight: legacy infrastructure creates switching costs that slow transitions. The dollar's 56.9% reserve share remains 3× the euro (19.9%) and 20× the renminbi (2.8%).

2. No Credible Single Challenger (μScore: 0.17)

The opponent noted that the renminbi's 3.5-4.6% global payments share cannot plausibly replace dollar dominance. The euro lacks fiscal union; gold is not a transaction medium; no single currency can replicate the dollar's institutional ecosystem. This is the strongest counter-argument: dethronement requires a successor, and none exists.

3. Historical Timeline Argument (μScore: 0.27)

Reserve currency transitions historically spanned decades to centuries. Sterling's decline from 1947-1976 took 30 years even with obvious structural deterioration. The 42-year timeline to 2066 may be insufficient for complete dethronement.

The debate hinges on a definitional question: What constitutes "dethronement"?

If dethronement means complete displacement—dollar falling below 20% of reserves and losing trade invoicing dominance—this is unlikely by 2066. The opponent's argument that no single successor exists is correct. The euro lacks fiscal integration; the renminbi lacks capital account convertibility; gold is not a transaction currency.

However, if dethronement means loss of singular primary reserve status—dollar declining from 56.9% to 35-40%, sharing co-equal status with a basket of alternatives (euro, renminbi, gold, CBDCs)—the affirmative case is substantially stronger. The evidence supports graduated decline, not binary collapse:

| Scenario | Dollar Reserve Share 2066 | Status |

|---|---|---|

| Status Quo | 55-60% | Dominant Primary |

| Graduated Decline | 35-45% | Co-Primary |

| Significant Erosion | 25-35% | First Among Equals |

| Full Dethronement | <25% | Displaced |

Legend: Projected dollar reserve share scenarios by 2066. The affirmative argues for Scenario 2-3; the opponent defends Scenario 1. Historical precedent and current trends favor graduated decline.

Where the Evidence Points:

The dollar has already lost 15 percentage points of reserve share (72% → 57%) since 2000—a 21% relative decline over 24 years. Extrapolating this trajectory yields 35-40% by 2066. This represents loss of singular primary status, which satisfies "dethronement" as commonly understood: the dollar would no longer dominate; it would share reserve currency primacy.

The sanctions-weaponization feedback loop, fiscal compounding, and CBDC infrastructure development are acceleration mechanisms not present in sterling's decline. Historical analogies may underestimate transition speed in a digitized, multipolar financial system.

The debate verdict: The affirmative has demonstrated that substantial erosion of dollar primacy by 2066 is more likely than not. Complete displacement is improbable; loss of singular dominance is probable. The claim of "dethronement" is affirmed when properly understood as loss of exclusive primary reserve currency status.

Round 3

Unable to produce an articulated answer.

1. The "decline" is largely a valuation artifact, not deliberate flight. The headline reserve-share drop in 2025 was overwhelmingly driven by exchange-rate translation, not central banks selling dollars. Measured at constant exchange rates, the dollar's share barely moved and has hovered near 58% since 2022. A 40-year forecast of collapse cannot be built on a decline that, properly measured, did not happen. The affirmative's straight-line extrapolation to "sub-40% by 2066" assumes a constant slope while ignoring that most of the recent move is FX math, not portfolio reallocation.

2. There is no viable successor, and the leading candidate is structurally disqualified. A currency cannot be dethroned without a throne-taker. The renminbi sits near 2% of reserves and is hobbled by capital controls, non-convertibility, and state-directed credit—conditions the Chinese political system will not abandon. Crucially, the alternative depends on the dollar: RMB internationalization without capital-account liberalization requires dollar backing the PBOC must continue to hold. The euro lacks a unified fiscal backbone; gold yields nothing and cannot clear at scale. None can absorb the global demand for a deep, convertible safe asset.

3. The structural moat—Treasury market depth and dollar plumbing—is unmatched. The US Treasury market, near $28 trillion, exceeds the combined government bond markets of China, Japan, the UK, France, Italy, and Germany. When the 2025 tariff turbulence tested it, depth recovered and kept improving into 2026. The dollar sits on roughly 89% of FX trades, dominates trade invoicing across every region, and anchors ~55–60% of international banking. This is embedded infrastructure measured in decades and trillions of sunk investment.

4. Our Round 2 dismantling of "geopolitical fragmentation" held. CIPS's ¥124 trillion converts to roughly $17 trillion annually—against dollar rails (Fedwire + CHIPS) clearing well over a quadrillion. CIPS still largely rides on Western messaging. The Russia yuan-ruble pivot was sanctions-coerced, not market-chosen, and exposed the non-convertibility trap when Russia's rupee and yuan holdings became stranded. Fast growth off a near-zero base does not equal succession.

5. The fiscal objection does not dethrone—it requires a substitute that does not exist. The economic record undercuts the credibility-crisis narrative: GDP growth held at 2.5–2.9%, inflation fell from 8.0% in 2022 to 2.95% in 2024, and unemployment stayed near 4%—even as debt-to-GDP rose to 118%.

| Indicator | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| GDP Growth (%) | 2.51 | 2.89 | 2.79 | — |

| CPI Inflation (%) | 8.00 | 4.12 | 2.95 | — |

| Unemployment (%) | 3.65 | 3.64 | 4.02 | 4.28 |

| Debt-to-GDP (%) | 114.70 | 116.92 | 117.97 | — |

Legend: US macro indicators, 2022–2025 (annual). Rising debt coincided with resilient growth, successful disinflation, and stable employment—the profile that sustains, rather than erodes, reserve confidence. Units: %.

High debt is universal among reserve issuers—Japan exceeds 250% debt-to-GDP and the yen remains a reserve currency. Markets continued funding the US at term yields below the policy rate, the opposite of a confidence crisis.

The affirmative landed real hits, and intellectual honesty requires naming them:

- ■

The historical-precedent argument is the strongest on their side. Sterling did fall from ~80% to under 20% in roughly 30 years, faster than its defenders predicted. Reserve transitions can compress into decades once underway. This is a legitimate caution against complacency, and "it has never happened fast" is not a valid rebuttal—it has.

- ■

Sanctions weaponization created a genuine, rational incentive to diversify. The 2022 reserve freeze was observed by every central bank, and "insurance" diversification—gold accumulation at record levels, bilateral arrangements—is a real, durable behavioral shift, even if not yet a regime change.

- ■

The "effective dethronement via fragmentation" reframing is clever and partly correct. If "dethronement" means losing hegemonic dominance rather than first place, a multipolar drift is more plausible than outright replacement. The dollar can lose share without any rival winning.

- ■

The fiscal trajectory is a real long-run vulnerability. Rising interest costs as a share of revenue are a legitimate structural pressure that compounds over a 40-year horizon—longer than any single business cycle our data captures.

The decisive issue is the definition of dethronement. On the literal question the claim poses—will the dollar be dethroned from its position as the world's primary reserve currency by 2066—the FALSE side prevails on the weight of evidence. Dethronement demands a successor able to provide a deep, convertible, rule-of-law-backed safe asset at global scale, and no such candidate exists or is on a credible path to exist within four decades. The renminbi is politically self-disqualified, the euro fiscally fragmented, gold structurally unsuitable, and CBDCs are rail-neutral—they change the plumbing, not the reserve asset flowing through it.

The affirmative's most honest fallback—"effective dethronement" through fragmentation—is where the two sides genuinely converge: continued gradual erosion of dollar share is likely. But that is precisely not the claim under debate. Losing some share while remaining the largest, deepest, most-used currency by a wide margin is the persistence of primacy, not its end.

Honest assessment: The probability that the dollar is meaningfully dethroned—displaced as the primary reserve currency—by 2066 is low. The probability that its share continues to drift down toward a more multipolar mix is moderate-to-high. The affirmative conflated the second, plausible outcome with the first, improbable one. On the question as literally posed, the claim is false: continued dollar primacy through 2066 remains the most likely outcome, with marginal erosion—not regime change—the realistic path.

| Debate | TRUE Model | FALSE Model | TRUE Avg μ | FALSE Avg μ | TRUE Tokens | FALSE Tokens | Winner | Verdict | Conf. |

|---|---|---|---|---|---|---|---|---|---|

| #1 | z-ai/glm-5 | openai/gpt-5.4-mini | 0.306 | 0.180 | 33 | 60 | TRUE | TRUE | 85% |

| #2 | z-ai/glm-5 | anthropic/claude-opus-4.8 | 0.000 | 0.000 | 33 | 360 | TRUE | FALSE | 95% |

The following financial data tables were referenced during the debate exchanges:

| Indicator | 2022 | 2023 | 2024 | Trend |

|---|---|---|---|---|

| US Debt/GDP (%) | 114.7 | 116.9 | 118.0 | Rising |

| US GDP Growth (%) | 2.51 | 2.89 | 2.79 | Stable |

| US Unemployment (%) | 3.65 | 3.64 | 4.02 | Rising |

Legend: US macroeconomic indicators 2022-2024. Debt/GDP shows persistent fiscal deterioration despite moderate growth. Source: OECD/World Bank historical data.

</FinancialData>

| Currency | Reserve Share 2024 | Reserve Share 2000 | Change | SWIFT Payment Share 2024 |

|---|---|---|---|---|

| USD | 56.92% | 72.0% | -15.08pp | 83.22% |

| EUR | 19.92% | 18.0% | +1.92pp | 7.84% |

| CNY | 2.80% | 0.1% | +2.70pp | 4.61% |

| Gold | 15.0%* | 10.0%* | +5.00pp | N/A |

Legend: Global reserve currency allocation trends (IMF COFER data, Q3 2024). Gold represents central bank gold holdings as % of total reserves. SWIFT payment share reflects Dec 2024. The dollar's 31-year low in reserves contrasts with persistent FX trading dominance.

</FinancialData>

| Metric | 2022 | 2023 | 2024 | CBO 2054 Proj. |

|---|---|---|---|---|

| US Debt/GDP (%) | 114.7 | 116.9 | 118.0 | 166.0 |

| Dollar Reserve Share (%) | 58.4 | 57.8 | 56.9 | ~45-50 (est.) |

| US Structural Deficit (% GDP) | 4.6 | 5.2 | 5.4 | 7.0+ |

Legend: US fiscal indicators and dollar reserve share trends. CBO projections indicate accelerating fiscal stress. Reserve share decline (2000-2024) extrapolated suggests continued erosion.

</FinancialData>

| Scenario | Dollar Reserve Share 2066 | Status |

|---|---|---|

| Status Quo | 55-60% | Dominant Primary |

| Graduated Decline | 35-45% | Co-Primary |

| Significant Erosion | 25-35% | First Among Equals |

| Full Dethronement | <25% | Displaced |

Legend: Projected dollar reserve share scenarios by 2066. The affirmative argues for Scenario 2-3; the opponent defends Scenario 1. Historical precedent and current trends favor graduated decline.

</FinancialData>

| Currency | Global FX Reserves 2024 | FX Transaction Share | Trade Invoicing Share |

|---|---|---|---|

| US Dollar | 58.4% | 88.3% | 79.5% |

| Euro | 20.0% | 30.5% | 51.2% |

| Japanese Yen | 5.5% | 16.8% | 32.9% |

| British Pound | 4.8% | 12.9% | 44.6% |

| Chinese RMB | 2.3% | 6.9% | 12.8% |

Legend: Global reserve currency shares and transaction usage, 2024. FX reserves from IMF COFER data; transaction share from BIS Triennial Survey; trade invoicing from Gopinath et al. research. RMB figures reflect accelerated growth but remain fraction of dollar dominance.

</FinancialData>

| Indicator | 2022 | 2023 | 2024 | Trend |

|---|---|---|---|---|

| US GDP Growth (%) | 2.51 | 2.89 | 2.79 | Stable |

| CPI Inflation (%) | 8.00 | 4.12 | 2.95 | Declining |

| Unemployment (%) | 3.65 | 3.64 | 4.02 | Stable |

| Debt-to-GDP (%) | 114.7 | 116.9 | 118.0 | Rising |

| 10-Yr Treasury Yield (%) | 4.01 | 4.28 | 4.35 | Elevated |

Legend: US macroeconomic indicators, 2022-2024. Data reflects resilient growth, successful inflation moderation, and sustained Treasury demand despite rising debt levels. Yields represent year-end levels.

</FinancialData>

| Reserve Currency | 2001 Share | 2024 Share | Change | Required Growth to Match Dollar |

|---|---|---|---|---|

| US Dollar | 71.5% | 58.4% | -13.1% | — |

| Euro | 18.3% | 20.0% | +1.7% | +192% |

| Chinese RMB | 0.0% | 2.3% | +2.3% | +2,439% |

| Japanese Yen | 5.0% | 5.5% | +0.5% | +962% |

| Other | 5.2% | 13.8% | +8.6% | — |

Legend: Global reserve currency composition, 2001 vs 2024. "Required Growth" shows the increase needed for each currency to match current dollar holdings at 58.4%. Even with rapid RMB growth, matching dollar reserves would require decades. Source: IMF COFER data.

</FinancialData>

| Currency | Reserve Share 1999 | Reserve Share 2025 Q3 | SWIFT Payments Dec 2025 |

|---|---|---|---|

| US Dollar | 71.2% | 56.9% | 50.5% |

| Euro | 19.1% | 20.3% | 22.0% |

| Japanese Yen | — | 5.8% | <5% |

| British Pound | — | ~5% | <5% |

| Chinese Renminbi | 0% | 1.9% | <5% |

Legend: Currency composition of global FX reserves (IMF COFER, 1999 vs Q3 2025) and SWIFT international payment share (Dec 2025). The dollar's reserve share decline is largely valuation-driven; no rival exceeds ~22% on any metric. Units: % share.

</FinancialData>

| Reserve Currency | 1945 Share | 1975 Share | Change | Annual Decline |

|---|---|---|---|---|

| British Pound | ~80% | ~18% | -62% | -2.1%/year |

| US Dollar (2000-2025) | 72.0% | 56.9% | -15.1% | -0.6%/year |

| Projected Dollar 2066 | — | ~38% | — | -0.6%/year |

Legend: Historical reserve currency decline trajectories. Sterling lost 62 percentage points over 30 years (1945-1975). The dollar has lost 15 percentage points over 25 years; extending this trajectory yields sub-40% share by 2066. Sources: IMF COFER, Eichengreen (2011), BIS data.

</FinancialData>

| Settlement System | Currency | Daily Volume (USD) | Annual Volume (USD) |

|---|---|---|---|

| Fedwire | Dollar | $4,500B | $1,180,000B |

| CHIPS | Dollar | $1,800B | $470,000B |

| CIPS | Renminbi | $75B | $17,000B |

Legend: Comparison of major large-value payment systems by approximate volume. Dollar-clearing rails (Fedwire + CHIPS) process roughly 95x the volume of China's CIPS, which still largely depends on SWIFT for messaging. Units: USD billions; CIPS figure derived from the ¥124tn 2024 headline. Illustrative scale comparison.

</FinancialData>

| Indicator | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|

| GDP Growth (%) | 2.51 | 2.89 | 2.79 | — |

| CPI Inflation (%) | 8.00 | 4.12 | 2.95 | — |

| Unemployment (%) | 3.65 | 3.64 | 4.02 | 4.28 |

| Debt-to-GDP (%) | 114.70 | 116.92 | 117.97 | — |

Legend: US macro indicators, 2022–2025 (annual). Rising debt coincided with resilient growth, successful disinflation, and stable employment—the profile that sustains, rather than erodes, reserve confidence. Units: %.

</FinancialData>

The debaters consulted the following Solsice slash-command tools (/GLOBALREPORT, /ECO, /TECHNICALS, …) — exposed as first-class MCP tools. Each block below is the raw output retrieved during the debate.

MCP tool: generate_eco_report

Historical window: last 5 years (no forecast).

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.793 |

| 2023 | annual | 2.888 |

| 2022 | annual | 2.512 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 2.950 |

| 2023 | annual | 4.116 |

| 2022 | annual | 8.003 |

| Period | Frequency | Value |

|---|---|---|

| 2025 | annual | 4.282 |

| 2024 | annual | 4.022 |

| 2023 | annual | 3.638 |

| 2022 | annual | 3.650 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 117.973 |

| 2023 | annual | 116.919 |

| 2022 | annual | 114.695 |

| Period | Frequency | Value |

|---|---|---|

| 2024 | annual | 82.893 |

| 2023 | annual | 82.612 |

| 2022 | annual | 83.021 |

| Period | Frequency | Value |

|---|---|---|

| 2022 | annual | 13.943 |

…(truncated)…

MCP tool: generate_treasury_report

Historical window: last 5 years (no forecast).

| Tenor | Latest | 1Y Ago | Chg 1Y | 5Y Ago | Chg 5Y |

|---|---|---|---|---|---|

| 1MO | - | - | - | - | - |

| 3MO | - | - | - | - | - |

| 6MO | - | - | - | - | - |

| 1YR | - | - | - | - | - |

| 2YR | - | - | - | - | - |

| 3YR | - | - | - | - | - |

| 5YR | - | - | - | - | - |

| 7YR | - | - | - | - | - |

| 10YR | - | - | - | - | - |

| 20YR | - | - | - | - | - |

| 30YR | - | - | - | - | - |

…(truncated)…

Debate Transcripts

- ■

Ownership & Trade Secrets. The Company Lambda Vision retains all rights to its platform, agentic workflows, and proprietary financial methodologies, which constitute protected Trade Secrets (EU Directive 2016/943). Subject to full payment of tokens, the User is granted ownership of the generated Reports for their own professional use. Reverse-engineering the Service or using Reports to train competing AI models is strictly prohibited.

- ■

No Financial Advice. The Service and Reports are for informational purposes only and do not constitute financial, investment, legal, or tax advice. The Company is not a regulated financial advisor. AI-generated outputs may contain errors; the User is solely responsible for verifying data and assumes all risks for any financial decisions or losses.

- ■

Liability & Governing Law. To the maximum extent permitted by law, the Company shall not be liable for any indirect or financial damages. These Terms are governed by French law. Any disputes shall be subject to the exclusive jurisdiction of the Courts of Paris, France.